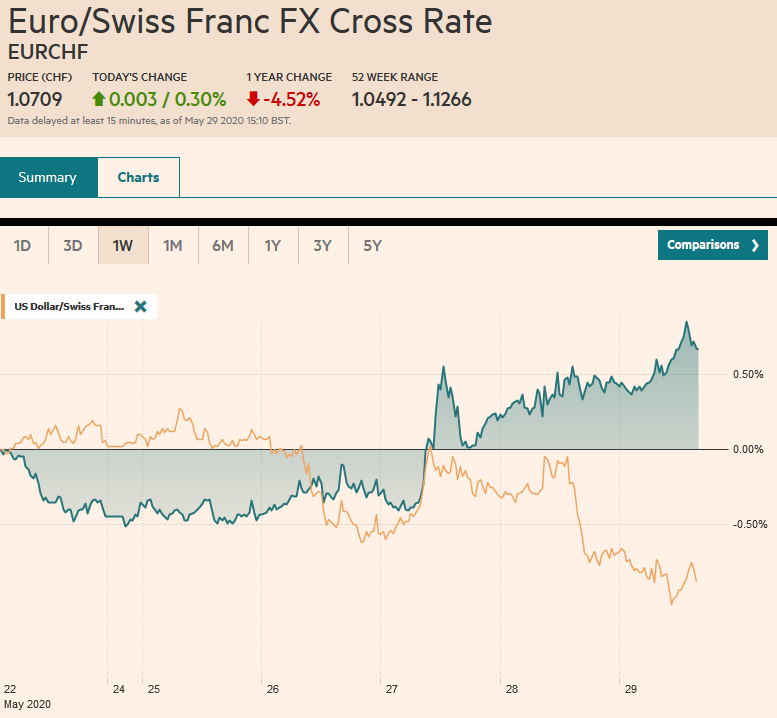

Swiss Franc The Euro has risen by 0.30% to 1.0709 EUR/CHF and USD/CHF, May 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The announcement that President Trump will hold a press conference on China later today rattled investors yesterday after they had earlier shrugged off the escalation of tension between the US and China to take the S&P 500 up to its highest level in nearly three months. The S&P 500 reversed and settled on its lows, and this carried over into today’s activity, which also may be reflecting month-end adjustments. Equity markets in the Asia Pacific region were mixed, with Japan, Hong Kong, Australia, and Taiwan seeing selling pressure. Still, the Nikkei finished the week with more than

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, cnh, Currency Movement, ECB, Featured, Hong Kong, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.30% to 1.0709 |

EUR/CHF and USD/CHF, May 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The announcement that President Trump will hold a press conference on China later today rattled investors yesterday after they had earlier shrugged off the escalation of tension between the US and China to take the S&P 500 up to its highest level in nearly three months. The S&P 500 reversed and settled on its lows, and this carried over into today’s activity, which also may be reflecting month-end adjustments. Equity markets in the Asia Pacific region were mixed, with Japan, Hong Kong, Australia, and Taiwan seeing selling pressure. Still, the Nikkei finished the week with more than a 7% gain, and Australia’s rose 4.7%. The Dow Jones Stoxx 600 is snapping a four-day advance today, led by energy, consumer discretionary, and finance sectors. With a 1.25% loss near midday, the benchmark is still up nearly 3.2% on the week. US stocks are trading lower, and the S&P 500 is up 2.5% for the holiday-shortened week coming into today. The US dollar is softer against most of the major currencies, and the euro rose to almost $1.1140, its best level since the end of March. Emerging market currencies are mixed, while the JP Morgan Emerging Market Currency Index gained a little more than 1% this week after a 2.4% gain last week. Gold is consolidating near $1725. It settled last week near $1734. Oil is a little heavy after a sharp rise in US inventories. The July WTI futures contract is near $32.50 after closing last week around $33.25. |

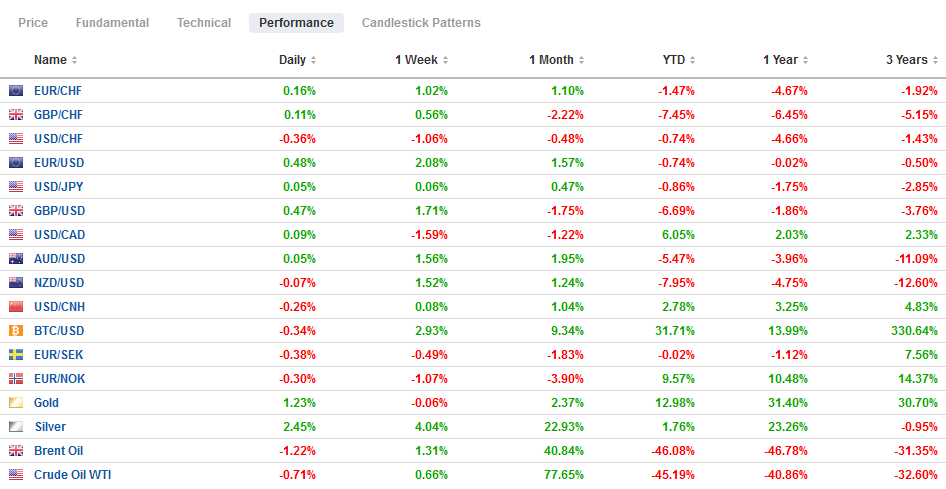

FX Performance, May 29 - Click to enlarge |

Asia Pacific

Honk Kong dollar forward points eased a little but remain elevated. The three-month forward points are a bit below 170 points, down from 213 at the end of last week. It was near 65 points in the middle of the month. The 12-month forward points are near 645. It was quoted near 768 a week ago, and 221 two weeks ago. The Hong Kong stock market eked out a minor gain on the week (-0.15%).

The PBOC set the dollar’s reference rate at CNY7.1316. The bank models implied about CNY7.1324. There was some intra-week volatility, but the dollar is finishing the week little changed. It is near CNY7.14 now and CNY7.1365 a week ago. The offshore yuan shows a bit more pressure. The dollar is trading a little above CNH7.16, and a week ago, the dollar settled near CNH7.1485.

Japanese April industrial output and retail sales were weaker than expected, tumbling 9.1% and 9.6% on the month, respectively. The jobless rate edged up to 2.5% from 2.4%, and the job-to-applicant ratio eased from 1.39 to 1.32. On the other hand, as has been seen elsewhere, consumer confidence ticked up in May, rising to 24 from 21.6. Tokyo’s core CPI returned positive in May, rising 0.2% year-over-year after a 0.1% decline in April and excluding fresh food and energy, it rose to 0.5% from 0.2%.

The dollar fell to a two-week low near JPY107.10 in late Asian turnover and has not been able to resurface much above JPY107.30 in the European morning. The greenback is off about 0.4% for the week against the yen, its first decline in two weeks. For the month, the dollar is virtually unchanged after falling in the first four months of the year. The Australian dollar remains firm today, but it continues to trade within the range set on Tuesday (~$0.6540-$0.6675). It has risen seven of the past eight weeks, including this week’s roughly 1.75% advance (~$0.6655). There is an option for about A$665 mln struck at $0.6650 that expires today.

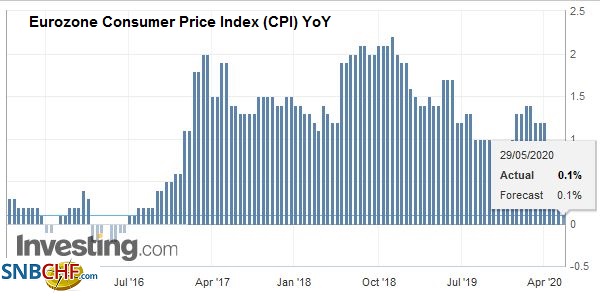

EuropeThe preliminary estimate of May CPI showed a 0.1% rise year-over-year, a four-year low. It is down from 0.4% in April but was spot on expectations. The core rate was a bit stickier and was unchanged at 0.9%. There are no policy implications for next week’s ECB meeting. The new staff forecasts are likely to echo Lagarde’s comments this week, suggesting downward revisions to the base case. Given the pace of ECB purchases, it appears to be on track to deploy the 750 bln euro Pandemic Emergency Purchase Plan by late Q3. It is widely expected to be expanded by at least 500 bln euros and extended well into next year. The ECB is also likely to indicate readiness to buy new EU bonds if the new proposal is approved (European heads of state and the European Parliament). Meanwhile, the April money supply and lending figures suggest that many banks will likely qualify for the maximum minus 100 bp TLTRO loans in next month’s operation. |

Eurozone Consumer Price Index (CPI) YoY, May 2020(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

| At the start of next week, the UK government may seek to put more onus on businesses to pick up more of the tab for furloughed workers starting in August. Employers may pick up a greater share of wages, insurance, and benefits. Meanwhile, trade talks with the EU are not showing much progress, and there may be some brinkmanship ahead of next month’s EU summit. |

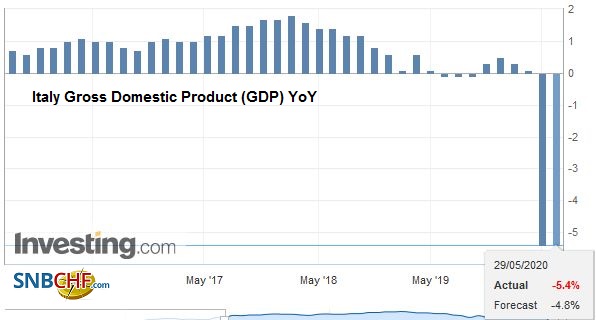

Italy Gross Domestic Product (GDP) YoY, Q1 2020(see more posts on italy-gross-domestic-product, ) Source: investing.com - Click to enlarge |

Near $1.1140, the euro has risen a little more than 2% this week, its best weekly performance in two months. We see the ECB efforts to reanimate its transmission mechanism, which is, in part, to encourage carry-trades (buying of peripheral instruments) as a critical force. The EU fiscal support is clearly needed, but as Merkel herself has noted, it might not be agreed at next month’s summit. Meanwhile, note that the German government is coalescing around a recovery package that could be worth 50-100 bln euros. The euro is above the April highs, and the next target is the late March high near $1.1165. Sterling’s 1% gain this week (~$1.23) is among the weakest performances by the majors this week. This month it fell roughly 2.3%, the most by a major currency. The range for the week was set in the first couple of sessions (~$1.2165-$1.2365). There is an option for about GBP465 mln at $1.23 that expires today and another for almost GBP260 mln at $1.2355.

America

Yesterday’s flurry of US data did not offer much in fresh insight. Data surprise models pick-up that durable goods orders in April were not as weak as expected. Still, the difference between the actual drop of 17.2% and the 19% decline that economists projected in the Bloomberg survey is of little consequence. The same can be said for the minor tweak in Q1 GDP from a contraction of 4.8% at an annualized clip to 5.0% is virtually meaningless. Weekly initial jobless claims are noisy, and this continues to be true even though the numbers are much higher. Difficulty adjusting for California, which reports data every other week, and Florida, where the application process seems to be overwhelmed, seems to account for the bulk of the unexpected decline in continuing claims. Growth here in Q2 looks to be contracting by around 9-10% on a quarter-over-quarter basis.

Foreign central banks continued to replenish their Treasury holdings that were liquidated in March and the first half of April. During those six weeks, foreign officials liquidated $155 bln of their Treasuries from the custodial accounts kept at the Federal Reserve. They bought a little more than $5.2 bln in the week ending Wednesday to bring the seven-week shopping spree to almost $80 bln.

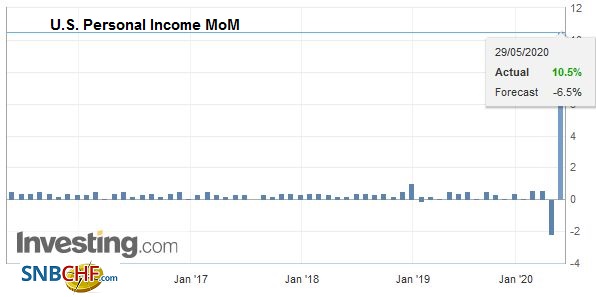

| Today’s US data highlights include the April trade balance and personal income and consumption reports. The income and consumption data will receive the most attention. Income is likely to continue to hold up better than consumption. The government is replacing income through transfer payments. In March, income fell 2%, and consumption slid 7.5%. In April, income is expected to have fallen by 6% and consumption by 12%+. The consequential rise in the saving rate seems largely involuntary, but the household liquidity preference may have also increased during the emergency. The economic shock is deflationary, and even if inflation risks are out there, they are not materializing now. On the contrary, disinflationary forces are still strengthening. The PCE deflator, which the Fed targets at 2%, is expected to fall to around 0.5% from 1.3%. The core measure that is often talked about is projected to decline toward 1.1% from 1.7%. In addition to Trump’s press conference, Fed Chair Powell participates in a virtual discussion (11 am ET). |

U.S. Personal Income MoM, April 2020(see more posts on U.S. Personal Income, ) Source: investing.com - Click to enlarge |

Canada reports March monthly and Q1 GDP. The median forecast in the Bloomberg survey shows a March contraction of around 8.5% after a flat reading in February. This would translate to a 3.7% year-over-year decline in output. It would mean that the economy shrank by about 10% in Q1 at an annualized pace following a 0.3% annualized expansion in Q4 19.

After falling Tuesday, the US dollar has remained pinned to its lows against the Canadian dollar. It has found support near CAD1.3725 but has not been able to reach much beyond CAD1.3820. The greenback is hovering near CAD1.3750 late in the European morning. The momentum indicators are stretched, but marginal new near-term US dollar losses are still possible. The US dollar is also trading with a heavier bias against the Mexican peso, and if the losses are sustained, it would be the ninth losing session of the past 10. With this month’s loss (~8.4%), the dollar will end a three-month rally that saw it rise by around 28%.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, May 28: Escalating Tensions, Calm Markets

FX Daily, May 28: Escalating Tensions, Calm Markets

Overview: The US Secretary of State’s announcement that the autonomy of Hong Kong could no longer be affirmed did not derail the rally in US equities. However, the threat of an executive order against social media companies may be discouraging follow-through buying, leaving US equities little changed ahead of the open. In contrast, Asia Pacific and European equities are mostly higher.

FX Daily, May 26: Fear is Still on Holiday

FX Daily, May 26: Fear is Still on Holiday

Overview: The heightened tensions between the US and China sapped risk-appetites before the weekend, but appear to be missing in action today. Equity markets have rebounded strongly. Nearly all the equity markets in the Asia Pacific region rose (India was a laggard) led by an almost 3% rally in Australia, which was seen as particularly vulnerable to the Sino-American fissure.

FX Daily, May 27: China and Hong Kong Pressures are Having Limited Knock-on Effects

FX Daily, May 27: China and Hong Kong Pressures are Having Limited Knock-on Effects

Overview: The S&P 500 gapped higher yesterday, above the recent ceiling and above the 200-day moving average for the first time since early March. The momentum faltered, and it finished below the opening level and near session lows. The spill-over into today’s activity has been minor. The heightened tensions weighed on China and Hong Kong markets, but Japan, South Korea, Taiwan, and Indian equity markets rose.

FX Daily, May 22: US-China Escalation Sinks Hong Kong and Hits Risk Appetites

FX Daily, May 22: US-China Escalation Sinks Hong Kong and Hits Risk Appetites

Overview: The US has ratcheted up pressure on China on several fronts and has sapped risk appetites ahead of the weekend. Equity markets are lower across the world. Even in India, where the central bank unexpectedly cut the repo rate 40 bp, shares fell 0.7%. It was Hong Kong’s 5.5% that led the region lower. Europe’s Dow Jones Stoxx 600 is off around 1% in late morning turnover to pare this week’s gain to about 2.5%.

FX Daily, March 19: ECB’s Bazooka Support Bonds but not the Euro

FX Daily, March 19: ECB’s Bazooka Support Bonds but not the Euro

Overview: It is not just that the dollar soared while stocks and bonds continued to plunge. The dollar’s strength is, in effect, a powerful short-covering rally. It was used to fund a great part of the global circuit of capital. The circuit of capital is in reverse now, and the funding currency is being bought back. The dollar’s strength is a function of the sell-off of other assets.

FX Daily, March 20: Markets Ending the Week on Better Note

FX Daily, March 20: Markets Ending the Week on Better Note

Overview: Dramatic price action continues but in the other direction. Stocks and bonds have rallied strongly, and the US dollar is snapping a strong advance with a sharp and broad setback. The immediate trigger is hard to identify. Some accounts linking it to fears that the California shutdown will be repeated throughout the country, deepening the coming downturn.

FX Daily, April 28: Oil’s Slides before Steadying, while Easing of Lockdowns Support Risk-Taking

FX Daily, April 28: Oil’s Slides before Steadying, while Easing of Lockdowns Support Risk-Taking

Overview: Equities are building on yesterday’s gains. The MSCI Asia Pacific Index rose 2% yesterday and edged higher today. Shanghai and Austalia stand out as exceptions. In Europe, the Dow Jones Stoxx 600 is extending yesterday’s 1.8% gain to reach its best level since March 11. Today would be the fourth advance in the past five sessions. US shares are firmer.

FX Daily, May 6: The Euro is Knocked Back Further

FX Daily, May 6: The Euro is Knocked Back Further

Overview: The late sell-off in US stocks yesterday has not prevented gains in Asia and Europe. Most of the equity markets, including the re-opening of China, gain more than 1%. Australia was a notable exception, falling about 0.4%, and Taiwan was virtually flat. European bourses opened higher but made little headway before some profit-taking set in, while US shares are trading higher.

Tags: #USD,$CNY,cnh,Currency Movement,ECB,Featured,Hong Kong,newsletter