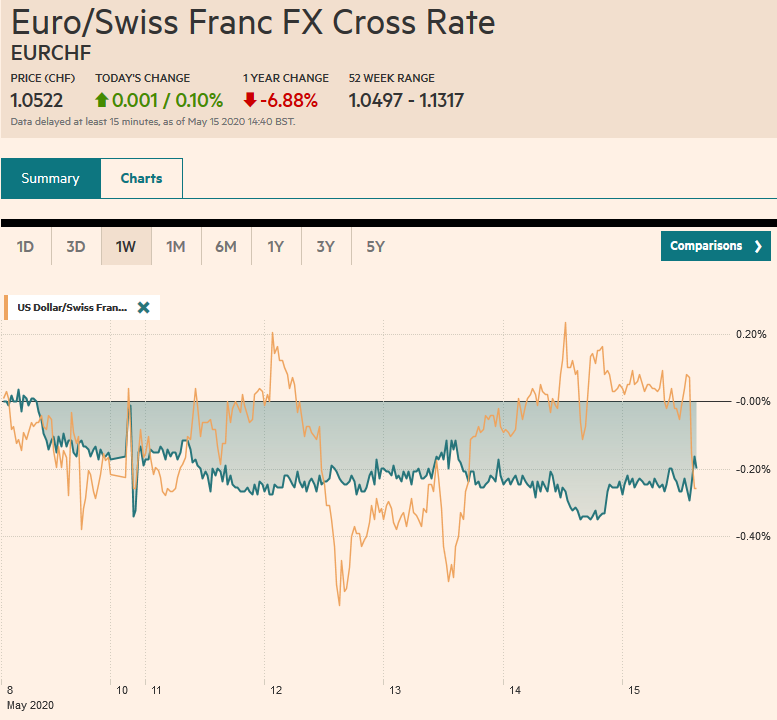

Swiss Franc The Euro has risen by 0.10% to 1.0522 EUR/CHF and USD/CHF, May 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The S&P 500 staged an impressive recovery yesterday, a sell-off that took it to its lowest level since April 21, to close more than 1% higher on the day, helped set the tone in the Far East and Europe today. Gains in most Asia Pacific markets, but Hong Kong, Shanghai, and India, trimmed this week’s losses. Australia’s 1.4% rally today managed to turn ASX positive for the week, extending leg up for a third consecutive week. The Dow Jones Stoxx 600 is up around 1% to pare this week’s loss to about 3.2%. US stocks are firm and look poised to extend yesterday’s recovery. Benchmark 10-year

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, China Fixed Asset Investment, China Industrial Production, China Retail Sales, Currency Movement, EUR/CHF, Eurozone Gross Domestic Product QoQ, Eurozone Trade Balance, Featured, FX Daily, Germany, Germany Gross Domestic Product, manufacturing, newsletter, U.S. Capacity Utilization Rate, U.S. Industrial Production, U.S. Retail Sales, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.10% to 1.0522 |

EUR/CHF and USD/CHF, May 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The S&P 500 staged an impressive recovery yesterday, a sell-off that took it to its lowest level since April 21, to close more than 1% higher on the day, helped set the tone in the Far East and Europe today. Gains in most Asia Pacific markets, but Hong Kong, Shanghai, and India, trimmed this week’s losses. Australia’s 1.4% rally today managed to turn ASX positive for the week, extending leg up for a third consecutive week. The Dow Jones Stoxx 600 is up around 1% to pare this week’s loss to about 3.2%. US stocks are firm and look poised to extend yesterday’s recovery. Benchmark 10-year yields are a little softer in most of Europe, and at 61 bp, the US 10-year Treasury yield is off nine basis points this week, the most among the G7 countries. The dollar is narrowly mixed, and for the week, only the Norwegian krone of the majors is higher on the week. Among emerging markets currencies today, Eastern and Central Europe are outperforming Asia Pacific. For the week, the Turkish lira is the strongest currency, advancing nearly 2.5% to snap a four-week slide. The JP Morgan Emerging Market Currency Index is off almost 0.5% for the week, its first decline in three weeks. Gold is approaching the mid-April high around $1747.50 for a nearly two percent gain on the week. July WTI edged to $29, its highest level since April 20 before consolidating. This is the third weekly gain, during which time the price of WTI has risen by nearly a third. |

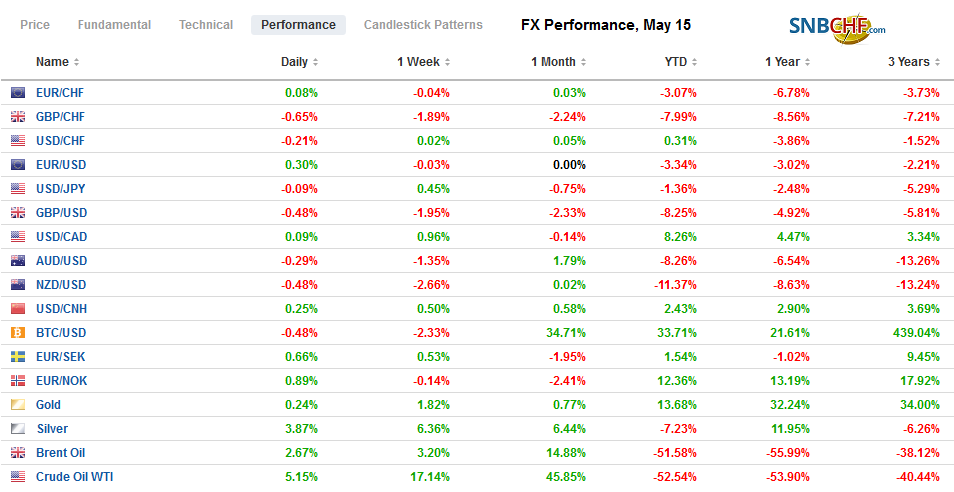

FX Performance, May 15 - Click to enlarge |

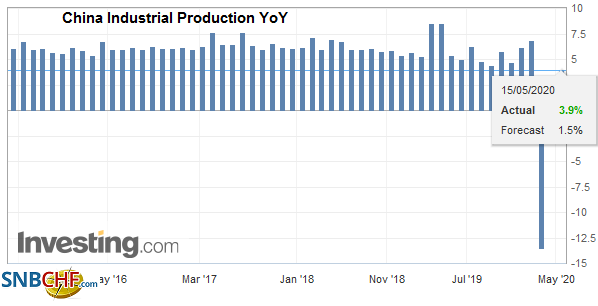

Asia PacificChina’s April data shows a recovery is taking hold, though consumption is lagging behind output. Retail sales fell 7.5% year-over-year in April, which was worse than expected, but better than the 15.8% decline in March. Industrial production rose 3.9% from a year ago after contracted 1.1% in March. |

China Industrial Production YoY, April 2020(see more posts on China Industrial Production, ) Source: investing.com - Click to enlarge |

| It was more than twice the gain median forecasts projected in the Bloomberg survey. Fixed investment was off 10.3% in April from a year ago, following a little more than a 16% slide in March. Surveyed joblessness rose to 6% from 5.9%. After next week’s National People’s Congress session, additional monetary and fiscal stimulus is expected. |

China Retail Sales YoY, April 2020(see more posts on China Retail Sales, ) Source: investing.com - Click to enlarge |

| Early Monday in Tokyo, Japan will report Q1 GDP. Economists expect a little more than a 1% contraction for the quarter and a 4.5% annualized rate. In Q4 19, the world’s third-largest economy shrank by 1.8% (-7.1% annualized). The current quarter will be the third consecutive decline in output, and a contraction of more than 5% (21.5% annualized) is expected. 2 |

China Fixed Asset Investment YoY, April 2020(see more posts on China Fixed Asset Investment, ) Source: investing.com - Click to enlarge |

The dollar has remained in the range set on Monday (~JPY106.40-JPY107.75). It has spent most of the recent session a tighter JPY106.80-JPY107.20. There are $2.4 bln in options expiring today struck at JPY107.00. The Australian dollar remains resilient. Yesterday, it did fall below the 20-day moving average but recovered to settle above it (~$0.6435). It has not closed below it since early April. Resistance is being encountered in the $0.6475 area. The dollar has edged higher for the third session against the Chinese yuan and is fraying the CNY7.10 level, the upper end of its month-long range. On the week, it is up about 0.4%.

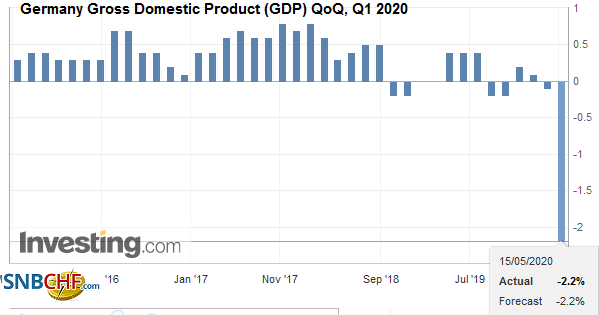

EuropeGerman Q1 GDP was spot on expectations with a 2.2% quarter-over-quarter decline. The surprise came as Q4 19 was revised to show a small contraction (-0.1%), underscoring the economic weakness as a pre-existing condition before the virus outbreak. It has freed itself from the self-imposed debt constraints, and its fiscal efforts are estimated to be around 7.5% of GDP, though this includes loan guarantees as well as spending commitments. |

Germany Gross Domestic Product (GDP) QoQ, Q1 2020(see more posts on Germany Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| It does support the idea of a “K” bottom, whereby some countries, with the fiscal space, can emerge stronger, and perhaps earlier than others. The flash PMIs next week are expected to show some improvement sequentially. |

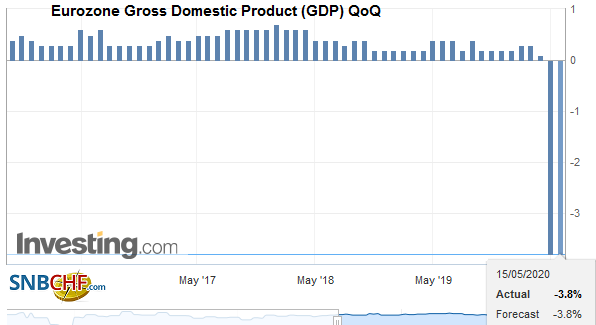

Eurozone Gross Domestic Product (GDP) QoQ, Q1 2020(see more posts on Eurozone Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| The latest round of UK-EU trade talks ends today. Little progress has been reported. The EU has rejected London’s proposal to place testing and certification activities for autos, chemicals, and pharmaceuticals in the UK. Disputes over fisheries and judiciary have not been resolved. There are rising frustrations on both sides. There will be another round of talks before the senior politicians meet again. Prime Minister Johnson has threatened to walk away from the negotiations if progress is not made by mid-year. It is difficult to see an alternative to a disruptive outcome. Separately, the UK is in trade talks with the US and Japan. |

Eurozone Trade Balance, March 2020(see more posts on Eurozone Trade Balance, ) Source: investing.com - Click to enlarge |

The euro is in a little more than a quarter of cent range today below $1.0820. There are nearly 570 mln euro options at $1.08 that is set to expire today. It finished last week around $1.0840. The high for the week was just shy of $1.09, and the low was set yesterday near $1.0775. Sterling matched its lowest level since March yesterday, near $1.2165. It recovered to $1.2240 today, where it was greeted with fresh sales. A close above $1.2250 would help stabilize the tone, but there is an option there that expires today for around GBP255 bln that may help prevent it.

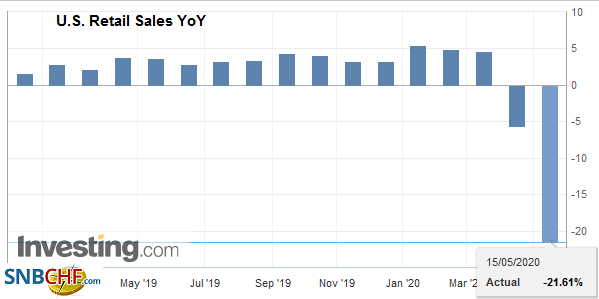

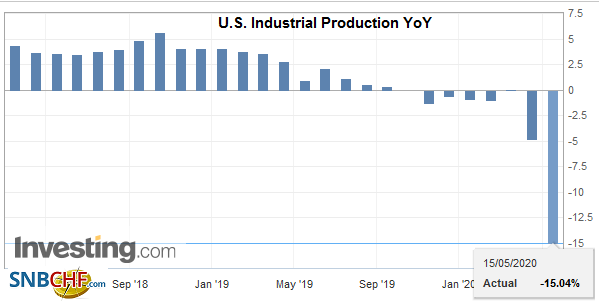

AmericaThe US reports April retail sales and industrial production figures today. Significant declines are widely anticipated. The median forecasts in the Bloomberg survey have fallen in recent days, and both are now expected to fall 12%. It seems unreasonable to expect that investors respond much to the news, leading to seeming anomalies with the equity markets. |

U.S. Retail Sales YoY, April 2020(see more posts on U.S. Retail Sales, ) Source: investing.com - Click to enlarge |

| More importantly, outside of the weekly jobless claims, where yesterday’s report has been distorted by a data entry error (~270k more initial claims) and a distortion caused by California’s every two-week filing rather than weekly as other states, the first indicator for May is due. It is the Empire State manufacturing survey. It may provide the first confirmation that the economy is bottoming. It is expected to rise to -60 from the record low of -78. During the worst of the Great Financial Crisis, it fell to -34.3. |

U.S. Industrial Production YoY, April 2020(see more posts on U.S. Industrial Production, ) Source: investing.com - Click to enlarge |

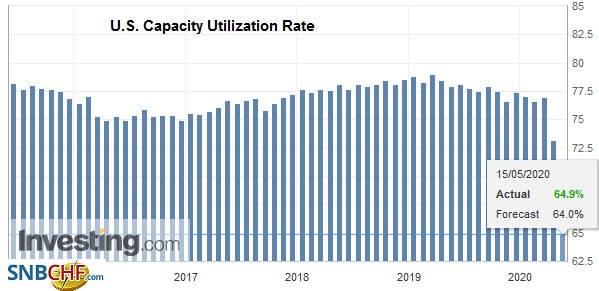

| There have been many claims about the US lack of manufacturing. This is simply not true. The US is the world’s second-largest manufacturer behind China. Before last year’s slump, it was at record levels. Many times, observers confuse employment in the sector with output. Employment has been in a secular downtrend, but this is a function of rising productivity. Others bemoan that is accounts for a shrinking share of GDP. That is true, but that reflects the growth of the output in services. The US imports about 15% of GDP, meaning the other 85% is produced domestically. With US government assistance, Taiwan Semiconductor announced it will build a $12 bln facility in Arizona that will employ 1600 people is a talking point today as it touches many issues, including re-on-shoring, and building to get inside the threatened US protectionist walls. |

U.S. Capacity Utilization Rate, April 2020(see more posts on U.S. Capacity Utilization Rate, ) Source: investing.com - Click to enlarge |

The Federal Reserve purchased a little more than $300 mln of corporate ETFs on the first day of the facility’s operation. It was a component of the increase (of almost $213 bln) in the Fed’s balance sheet to $6.93 trillion. Separately, the Fed reported that foreign central banks added about $21.2 bln to their Treasury holdings for which it provides custody services. It is the fifth week in a row that the central banks are replenishing their holdings of Treasuries that were liquidated in the March and early April mayhem. During a five-week stretch, they sold about $154 bln in Treasuries.

The US dollar is little changed against the Canadian dollar (~CAD1.4065) as the North American session is about to begin. There is a relatively large option (~$775 mln) at CAD1.4085 that expires today. Risk appetites (S&P 500 proxy) may be the key to how the Canadian dollar finishes the week. The pullback in equities this week is helping the greenback snap a two-week decline against the Loonie. In the broad picture, the US dollar is consolidating in a narrowing range around CAD1.40. The Mexican peso showed little reaction to the widely anticipated central bank’s decision to cut rates by 50 bp for the third time. At 5.50%, its target rate is still high in both nominal and real terms. The greenback is trading with a heavier bias against the peso for the third session. However, it settled last week near MXN23.65, and it is finding support now ahead of MXN23.70. It has also been broadly consolidating for the past month around MXN24.00.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, February 14: Investors Continue to Look Past the Coronavirus

FX Daily, February 14: Investors Continue to Look Past the Coronavirus

Overview: The capital markets are heading into the weekend, still trying to look past the coronavirus despite the new cases in Hubei. Tokyo was a notable exception in the Asia Pacific region, as the other major equity markets, like in Hong Kong, China, Taiwan, South Korea, and Australia, advanced. The MSCI Asia Pacific Index rose for the second week.

FX Daily, April 15: Dollar Rises as Equities Slump

FX Daily, April 15: Dollar Rises as Equities Slump

Overview: The recovery in equities stalled, and the risk-off mood has helped lift the US dollar, which had been trending lower. Taiwan and Malaysia were notable exceptions in the Asia Pacific regions to the heavier equity tone. The Nikkei gave back almost 0.5% after surging more than 3% on Tuesday. Europe’s Dow Jones Stoxx 600 is ending a five-day rally.

FX Daily, November 18: Sterling Shines in Subdued Start to the New Week

FX Daily, November 18: Sterling Shines in Subdued Start to the New Week

Overview: Equities in Europe and the US look to extend their six-week rally, while the MSCI Asia Pacific Index gets back on the winning way after stumbling last week. Despite the escalation of the conflict in Hong Kong, the Hang Seng rose 1.35% to lead the region and recoup a chunk of last week’s 4.8% slump. The Dow Jones Stoxx 600 puts the European benchmark within spitting distance of the four-year high set recently.

FX Daily, November 25: Hong Kong, China, and UK Election Hopes Fan Modest Risk-Taking

FX Daily, November 25: Hong Kong, China, and UK Election Hopes Fan Modest Risk-Taking

Overview: The combination of the victory of the pro-democracy movement in Hong Kong and an apparent concession by China on intellectual property rights is helping bolster risk appetites to start the week. Equities are higher. Hong Kong’s Hang Seng led Asia Pacific equities with a 1.5% gain, the second biggest this month. Korea and India’s bourses also gained more than 1%.

FX Daily, December 16: China Data Surprises to the Upside while Europe’s Manufacturing PMI Disappoints

FX Daily, December 16: China Data Surprises to the Upside while Europe’s Manufacturing PMI Disappoints

Overview: Despite better than expected Chinese data, and last week’s investor-friendly developments, Asia Pacific equities were mixed. Australia led the advancing bourses with a 1.6% gain, its largest for the year despite the government revising down growth and wages. China, Taiwan, and Indian markets also moved higher.

FX Daily, January 17: China and the UK Surprise in Opposite Directions

FX Daily, January 17: China and the UK Surprise in Opposite Directions

Overview: Helped by new record highs in the US, global stocks are moving higher today. Nearly all the markets in the Asia Pacific region advanced and the seventh consecutive weekly rally is the longest in a couple of years. Europe’s Dow Jones Stoxx 600 is at new record highs and appears set to take a four-day streak into next week. US shares are trading firmly.

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

Overview: The ring of containment of Covid-19 has grown from China. The new frontline is Japan, South Korea, Italy, and Iran. A lockdown of around 50k people near Milan and Austria blocking trains from Italy is scaring investors. Asian markets fell, but South Korea bore the brunt with a nearly 4% decline. The national holiday in Japan spared local equities.

FX Daily, March 17: Even Turn Around Tuesday is Flat

FX Daily, March 17: Even Turn Around Tuesday is Flat

Overview: While the markets are not as disorderly as they have been, the tone is fragile, and the animal spirits have been crushed. Australian stocks fell more than 10% last week and dropped another 9.7% yesterday before rebounding by almost 6% today to be one of the few Asia Pacific equity markets to rise. The Nikkei eked out a small gain, but the broader Topix rose 2.6%.

Tags: #USD,Brexit,China Fixed Asset Investment,China Industrial Production,China Retail Sales,Currency Movement,EUR/CHF,Eurozone Gross Domestic Product QoQ,Eurozone Trade Balance,Featured,FX Daily,Germany,Germany Gross Domestic Product,manufacturing,newsletter,U.S. Capacity Utilization Rate,U.S. Industrial Production,U.S. Retail Sales,USD/CHF