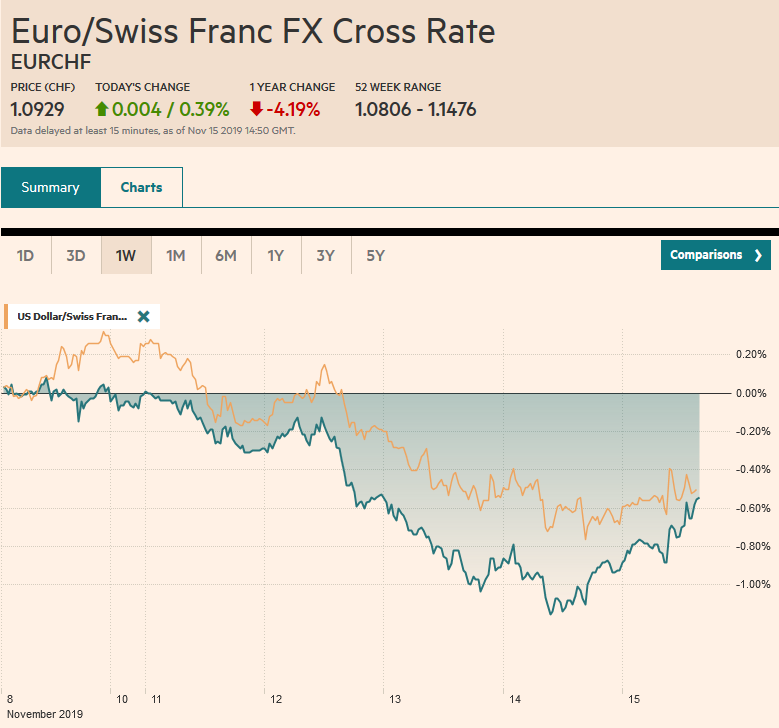

Swiss Franc The Euro has risen by 0.39% to 1.0929 EUR/CHF and USD/CHF, November 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Comments by US presidential adviser Kudlow playing up the prospects of a trade agreement between the US and China, with other reports suggesting a key call be held today, is helping to underpin sentiment into the weekend. The MSCI Asia Pacific Index pared this week’s loss today, with China the only main market not participating, despite the PBOC’s unexpected injection of CNY200 bln of the Medium-Term Lending Facility. The regional benchmark snapped a five-week advance. Europe’s Dow Jones Stoxx 600 is firmer today but practically unchanged on the week. A five-week advance is in

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, Currency Movement, EUR/CHF, Featured, FX Daily, Hong Kong, newsletter, USD, USD/CHF, USMCA

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.39% to 1.0929 |

EUR/CHF and USD/CHF, November 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Comments by US presidential adviser Kudlow playing up the prospects of a trade agreement between the US and China, with other reports suggesting a key call be held today, is helping to underpin sentiment into the weekend. The MSCI Asia Pacific Index pared this week’s loss today, with China the only main market not participating, despite the PBOC’s unexpected injection of CNY200 bln of the Medium-Term Lending Facility. The regional benchmark snapped a five-week advance. Europe’s Dow Jones Stoxx 600 is firmer today but practically unchanged on the week. A five-week advance is in tow, and its performance in the afternoon will determine whether this can be stretched into a sixth week. The same is true for the S&P 500. Benchmark 10-year yields are firmer on the day, but yields are mostly lower on the week. The US and German yields are off about 10 bp this week. Peripheral European bond yields have edged higher. The US dollar enjoys a firmer bias against the major currencies, with yen and Swiss franc the weakest. Turnover is quiet and ranges are small. Gold is giving back yesterday’s gain, and around $1463, it is up about less than $5 this week after losing $55 last week. December WTI is little changed today and has spent the week consolidating within the $56-$58 range. |

FX Performance, November 15 - Click to enlarge |

Asia Pacific

President Xi’s admonishment that “ending violence and restoring order” is the most important goal now adds to the sense that official patience is running thin. Low-intensity demonstrations, even if large, can be coped with, the scale of violence and the closure of schools and businesses means that the situation has become unsustainable. The financial markets are aware of this. The Hang Seng fell 4.8% this week, the most in three months. Since the currency is pegged to the dollar, the more efficient way to bet on tensions is not to sell the currency as it is to play for higher interest rates. This is being reflected in the forward market, where the three-month forward rates jumped to their highest in 20 years yesterday before pulling back today to still-elevated levels. Alibaba’s large IPO also probably contributed to the tightening of money market conditions.

US officials seeming to talk more about the prospects for a trade agreement than Chinese officials and have repeatedly been more optimistic that a deal can be achieved. Kudlow’s claim that only “short strokes” remains may be devilishly deceiving. The toughest elements are frequently the last, and as golfers say, “drive for show and putt for dough,” which also means the “short-strokes” are the most important.

The dollar is recovering from yesterday’s loss against the yen, which saw it down to JPY108.25, its lowest level since November 4. Today’s modest gains, if sustained, would end a five-day downdraft for the dollar, its longest losing streak in six months. A nearly $550 mln option is struck at JPY108.50 that expires today. The Australian dollar is consolidating yesterday’s loss, the largest in four months after the disappointing employment data were reported. The market does not appear to have completed its adjustment, and resistance is now pegged near $0.6800. It began the month over $0.6900. A break of $0.6770 could signal another near-term 1% decline. The dollar resurfaced above CNY7.0 this week and ended a five-week slide against the Chinese yuan, during which time it fell by a little more than 2%.

EuropeThe UK election, which may be as close to a second referendum on leaving the EU as the country may get, is less than a month away. Earlier Brexit Party head Farage had declared it would not run candidates in Tory-led districts. While this seems to bolster the Conservatives, many were hoping that the Brexit Party would not run candidates in Labour-led districts in which the majority voted to leave in the 2016 referendum. The Tories have targetted these districts to try to secure a majority. However, yesterday, Farage indicated the Brexit Party would field candidates there to have a stronger hand to negotiate with the Tories. |

Eurozone Consumer Price Index (CPI) YoY, October 2019(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

| In response to yesterday’s news that the German economy eked out the slightest growth (0.1%) in Q3, Finance Minister Scholz reiterated his claim that no new fiscal stimulus is needed. Nearly everyone outside of Germany wants Europe’s largest economy to provide more stimulus. Germany’s ordoliberalism, which Draghi once said, was part of the ECB’s DNA, rejects the kind of Keynesian demand management fiscal policy except in extreme circumstances. In countless calls for Germany to expand its fiscal policy, few observers even try to address the ordoliberal arguments. |

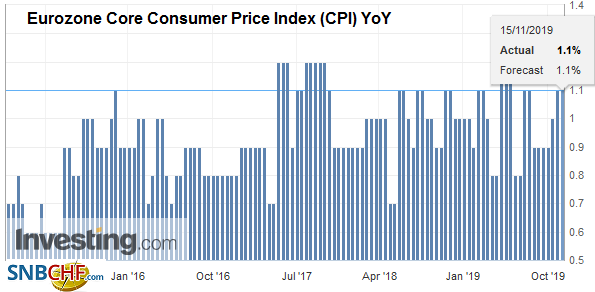

Eurozone Core Consumer Price Index (CPI) YoY, October 2019(see more posts on Eurozone Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

The euro posted a possible key upside reversal yesterday by making new lows for the move (just below $1.0990) and then recovering and closing above the previous session’s high (~$1.1020). The low neared the technical objective of the double top pattern (~$1.1180 in late October and early November). However, there has been no meaning follow-through buying today (~2/100s of a penny). It has been unable to decisively distance itself from the $1.10 level where a 1.2 bln euro option has been struck that expires today. Initial support is seen near $1.1015 today. On the week, the single currency is virtually flat after falling 1.3% the previous week. Near $1.2875, sterling has gained about a cent this week despite mostly disappointing data. The hope that the Tories can secure a majority continues to underpin it. It continues to trade within the range set at the start of the week (~$1.2780-$1.2900).

America

The Federal Reserve announced a series of new and longer repo operations in the coming period to help alleviate the pressure that is already becoming evident for the year-end roll. Some indicative prices for funding for around 125 bp above present rates. That more measures are being undertaken does not refute Powell’s claim that the situation ins under control. The Federal Reserve has the tools to make sure the repo market is calm. Yet is seems reluctant to follow the ECB’s “full allotment at a fixed rate,” which would, in essence, not limit the repo operations to a fixed amount but provide as much as anyone wanted, with the proper collateral. However, the problem is that officials are still trying to work out how much is needed, and unlimited provisions would not necessarily help this process. Many observers still want to call what the Fed is doing as QE, but remember that before the Great Financial Crisis, the Fed often conducted repo operations, and the balance sheet typically grew year-in and year-out. Moreover, we have often emphasized the signaling channel as the primary way QE worked, and that signaling channel is markedly different now.

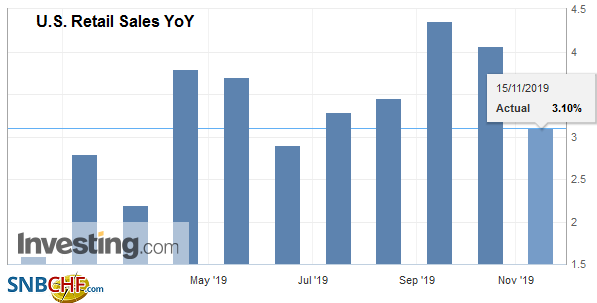

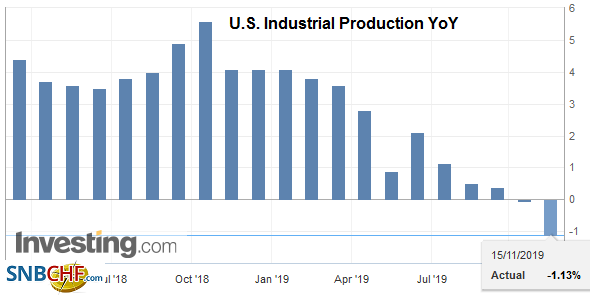

| There are three US economic reports today to note. October retail sales offer the latest read on the consumer, which is the one engine of the US economy that continues to perform well. Retail sales, which account for a little less than half of personal consumption, which is nearly 70% of GDP, fell in September and is expected to have bounced back last month. We suspect the headline will be dampened by poor auto sales. The core reading, whose components are used for GDP calculations, maybe stronger. After a flat reading in September, the median forecast in the Bloomberg survey is for a 0.3% gain. It averaged 0.4% in Q3, 0.6% in Q2, and 1.2% in Q1. The US report October industrial production. It is expected to have fallen by 0.4%, which would be the second consecutive decline. The contraction is led by manufacturing. The Bloomberg survey found a median forecast for a 0.7% decline. It would be the third decline in four months, though skewed by the strike at GM. The Empire State manufacturing survey offers among the first insights into this month’s activity. It is expected to tick up to around 6 from 4. If so, it would be the best since May. However, to put it in perspective, consider that last November it stood at 21.4. |

U.S. Retail Sales YoY, October 2019(see more posts on U.S. Retail Sales, ) Source: investing.com - Click to enlarge |

| After beginning the rate hike cycle with the overnight rate at 3.0% at the end of 2015, the central bank of Mexico raised rates until the end of last year when the overnight rates stood at 8.25%. Yesterday’s 25 bp rate cut was the third cut this year, bringing the target rate to 7.5%. The market favors another one at the December 19 meeting. Inflation (CPI) has fallen from about 6.8% at the end of 2017 to 3.0% in September and October. Barring significant currency volatility or another shock, we suspect the central bank will cut rates another 100 bp next year. |

U.S. Industrial Production YoY, October 2019(see more posts on U.S. Industrial Production, ) Source: investing.com - Click to enlarge |

We had argued that in a counter-intuitive way, the impeachment proceedings in the House of Representatives made a USMCA deal more likely. Speaker Pelosi was not a key driver of the impeachment process, and she has expressed concern about the left-wing of the Democrat Party. We understood this to strategically favor some action that would strengthen the moderates and deflect the criticism of a “do-nothing Congress.” It side agreement to enhance the enforcement of labor rules appears to have been struck a vote is now expected before the holiday recess next month.

The US dollar peaked near CAD1.3270 yesterday and shed its gains at least in part in response to the optimism on the USMCA. It fell to CAD1.3220 in Asia before bouncing back to around CAD1.3250, where a $560 mln option is struck, which expires today. The US dollar fell in one session this week and one session last week against the Canadian dollar. Although the market looks as if it wants to take another shot at the 200-day moving average (~CAD1.3275), the technical indicators are getting stretched, suggesting additional greenback gains may be difficult to sustain. The USMCA news may have helped the Mexican peso recover after the central bank delivered the expected rate cut yesterday, and there has been follow-through buying of the peso today. The dollar peaked mid-week near MXN19.53 and set a lower high yesterday around MXM19.4850. It is trading near a three-day low around its 200-day moving average (~MXN19.2650). Resistance is seen near MXN19.32 now.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brexit,Currency Movement,EUR/CHF,Featured,FX Daily,Hong Kong,newsletter,USD/CHF,USMCA