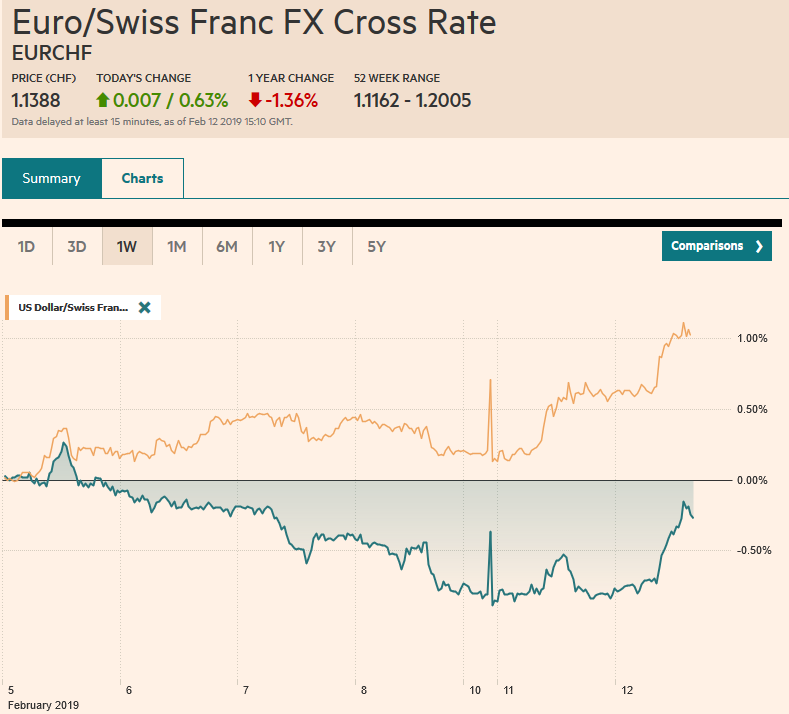

Swiss Franc The Euro has risen by 0.63% at 1.1388 EUR/CHF and USD/CHF, February 12(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The Dollar Index’s eight-day advance is in jeopardy. Although the greenback recorded new highs against some major currencies, the momentum appears to be stalling. The news stream is constructive as a compromise seems to have been reached to avoid another US government shutdown, and there is some optimism that the US and China will strike a deal even if not by March 1. Equities are moving higher. The MSCI Asia Pacific Index ended a four-day downdraft as the region’s largest markets rose. The Dow Jones Stoxx 600 gapped slightly

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CAD, EUR, EUR/CHF and USD/CHF, Featured, GBP, MXN, newsletter, SEK, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.63% at 1.1388 |

EUR/CHF and USD/CHF, February 12(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The Dollar Index’s eight-day advance is in jeopardy. Although the greenback recorded new highs against some major currencies, the momentum appears to be stalling. The news stream is constructive as a compromise seems to have been reached to avoid another US government shutdown, and there is some optimism that the US and China will strike a deal even if not by March 1. Equities are moving higher. The MSCI Asia Pacific Index ended a four-day downdraft as the region’s largest markets rose. The Dow Jones Stoxx 600 gapped slightly higher to extend yesterday’s gains. The 0.5% gain in the European morning was led by health care and consumer discretionary, but all sectors were in the green. The S&P 500 has a gap of its own from last week (~2719.3-2724.1), though the key is the 200-day moving average (~2743). Core bond yields are mostly one-basis points firmer, and core yield led by Italy are a couple basis points lower. Oil prices are more than a dollar a barrel off yesterday’s lows and iron ore prices are pulling back. |

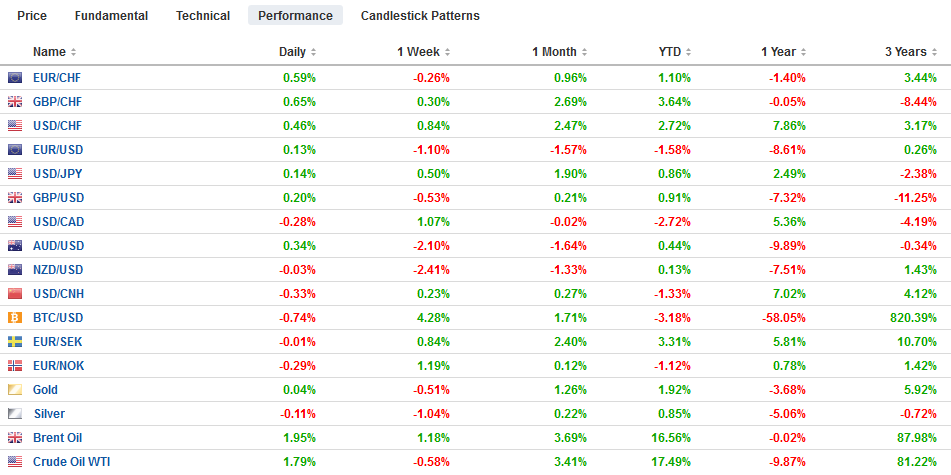

FX Performance, February 12 - Click to enlarge |

Asia Pacific

The Bank of Japan surprised many with its decision earlier today to reduce the amount of 10-25-year government bonds that it buys. It will buy JPY180 bln this month, down from JPY200 bln it has been buying since July. Some are reading more than a technical adjustment into the reduced purchases and maybe a modest rate protest. At the end of last week, yields at the very long-end of the Japanese curve (20-40 years) fell to three-year lows. Japanese yields did rise in response to the BOJ announcement, but none rose more than two basis points. The ten-year yield closed up a single basis point but remains slightly in negative territory.

Australia’s housing sector continues to contract. Home loan approvals tumbled 6.1% in December. Economists in the Bloomberg survey expected a 2% decline after falling nearly 1% in November. Home loan approvals fell for the last four months of 2018 and nine months throughout the year. Although the Reserve Bank of Australia adopted a neutral bias, the market is increasingly favoring a rate cut toward the end of the year.

One of the important developments that attract portfolio capital into China is the inclusion of its markets into global benchmarks. This is true for fixed income as well as equities. MSCI announced today that as of the end of the month, it will include a dozen more Chinese companies into its main benchmarks.

The dollar set new highs for 2019 against the yen near JPY110.65. There is a retracement target by JPY110.85 that may cap it. Above there lies the 200-day moving average (~JPY111.30) and the late December 2018 highs (~JPY111.40). Initial support today is seen near JPY110.30. The Australian dollar made a fractional new low but has firmed from about $0.7055 to almost $0.7080, where the five-day moving average is found. It has not closed above this average since February 1. A close above $0.7100 would give credence to views that a near-term low is in place. The dollar had traded briefly through CNY6.70 before the Lunar holiday but rebounded to almost CNY6.80 before finding new offers. Look for consolidation.

Europe

Brexit remains front and center. May is expected to seek Parliament support for an extension to the end of the month. Although she was careful not to formally rule out Labour’s demand to remain in a customs union, her spokespeople have made it clear, this is not under consideration. There are other reports today that suggest May could offer to resign in the summer to help force a deal now and to keep her rivals off-balanced. Yesterday’s news of a 0.4% contraction in December, with a fourth consecutive quarterly decline in investment, casts a cloud over the economic outlook. Moreover, Nissan and Airbus decisions are not included in the data.

Spain’s parliament debates the minority government’s budget today and is scheduled to vote on it tomorrow. The trial of the Catalan separatists for 2017 actions begins this week. The government needs support for its budget, or the government will fall. Threats to call elections for mid-April were denied, but the situation is moving toward a climax, even though Spanish assets show nothing amiss. Italian polls over the weekend showed center-right is gaining support. The League, Brothers of Italy, and Berlusconi’s Forza Italia are together polling around 45%. There continues to be speculation that the growing distance between the League and the Five Star Movement, especially with later now outstripping the senior coalition partner. League leader Salvini wants to be Prime Minister. He seems to sense it is within reach.

Sweden’s Riksbank meets tomorrow. It delivered its first hike at the end of last year. The economic data makes a tightening sequence difficult to envision. The repo rate will most likely remain at -0.25%. The euro appreciated 3.8% against the krona since the end of last year, and that move seems to be over. The euro peaked near SEK10.515 at the end of last week. Our initial target is SEK10.36-SEK10.40.

The euro dipped below $1.1260 before stabilizing. It has yet to resurface above $1.13, making it so far the first day since mid-November that it has not been above there. Selling pressure on sterling eased to near $1.2835, but the enthusiasm is not there to take it up much. It probably requires a move above $1.2880-$1.2900 to squeeze the late shorts.

America

It appears that a second government shutdown may be averted. A compromise deal was struck in principle. It does provide $1.375 bln for fencing along the border. Although the first shutdown was blamed primarily on Republicans, polling suggested this might not be the case of a second shutdown. If the agreement does work the next issue is the debt ceiling, which comes into force early next month. There are numerous ways Treasury can buy time to postpone the day of reckoning, but it is not without bounds.

Mid-level preparations for the high-level trade talks in China late this week continue. The Trump Administration continues to sound hopeful an agreement with be reached. Reports suggest that the crafting of the statement has begun. The current tariff freeze may be extended into March to allow time for Trump and Xi to meet. Even if some progress on reducing the bilateral imbalance is achieved, no one really thinks it will provide any closure for the super-power rivalry.

The economic data calendar is lacking market moving releases today. US JOLTS report rarely moves the market. Nor does Canada or Mexico have important data today. Fed Chair Powell speaks as do two of the more hawkish regional presidents (George and Mester) but a consensus backing a pause has clearly emerged.

The US dollar hit a ceiling in recent days against the Canadian dollar around CAD1.3315-CAD1.3325. A break of CAD1.3230-CAD1.3250 would suggest a near-term high is in place. The dollar jumped higher against the Mexican peso yesterday. Poor data (larger than expected drop in industrial output) and concerns about AMLO’s stance on the pipelines spooked investors. The dollar may find support near where it previously encountered resistance (MXN19.20-MXN19.25).

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,EUR/CHF and USD/CHF,Featured,MXN,newsletter,SEK