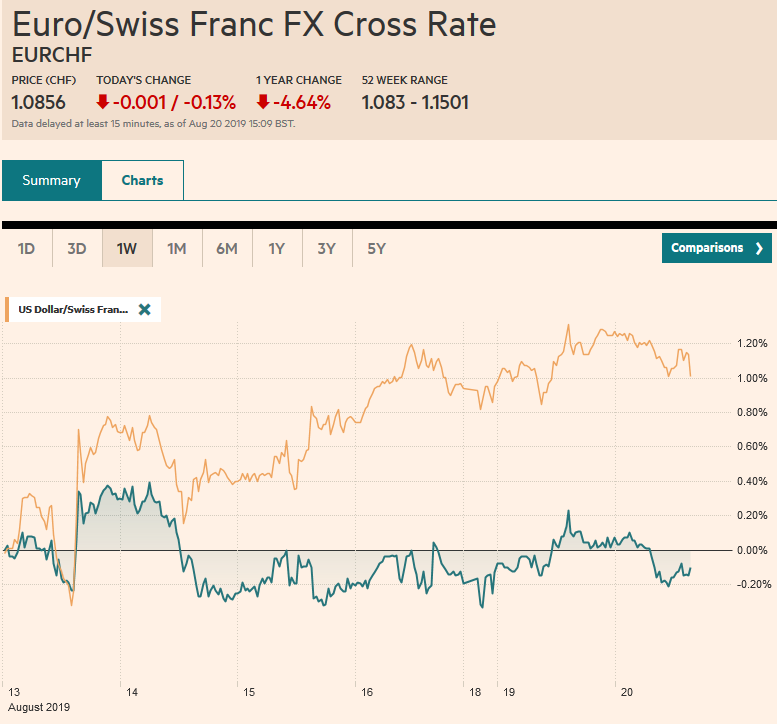

Swiss Franc The Euro has risen by 0.13% to 1.0856 EUR/CHF and USD/CHF, August 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Global equities and bonds are firmer in quiet turnover, and the dollar is narrowing mixed in narrow ranges. The big events of the week, the eurozone flash PMI and Powell’s speech at Jackson Hole still lie ahead. The MSCI Asia Pacific Index rose for the third consecutive session, led by Korea and Australia’s 1%+ gains. Europe’s Dow Jones Stoxx 600 is firm and testing two-week highs. US equities are also trying to extend yesterday’s gain. The rise in US yields yesterday dragged most of Asia Pacific higher, but the US 10-year slipped back from the test on 1.60%, and European yields are

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Currency Movements, EUR/CHF, Featured, FX Daily, Germany Producer Price Index, newsletter, SPX, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.13% to 1.0856 |

EUR/CHF and USD/CHF, August 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Global equities and bonds are firmer in quiet turnover, and the dollar is narrowing mixed in narrow ranges. The big events of the week, the eurozone flash PMI and Powell’s speech at Jackson Hole still lie ahead. The MSCI Asia Pacific Index rose for the third consecutive session, led by Korea and Australia’s 1%+ gains. Europe’s Dow Jones Stoxx 600 is firm and testing two-week highs. US equities are also trying to extend yesterday’s gain. The rise in US yields yesterday dragged most of Asia Pacific higher, but the US 10-year slipped back from the test on 1.60%, and European yields are two-three basis points lower. The dollar’s three-day advance against the yen has stalled near JPY106.70. The euro continues to trade heavily and has been unable to resurface above $1.11. Sterling is the weakest of the majors, off about 0.3% (a little below $1.21). New rules in Turkey that tie bank reserves requirements to lending may free up TRY5.4 bln (~$960 mln), which is thought likely to flow offshore, taking the lira off another 1% and taking the dollar to its best level in more than three weeks. After pushing below $1500 yesterday, gold has rebounded, while oil edges higher for the third consecutive session. |

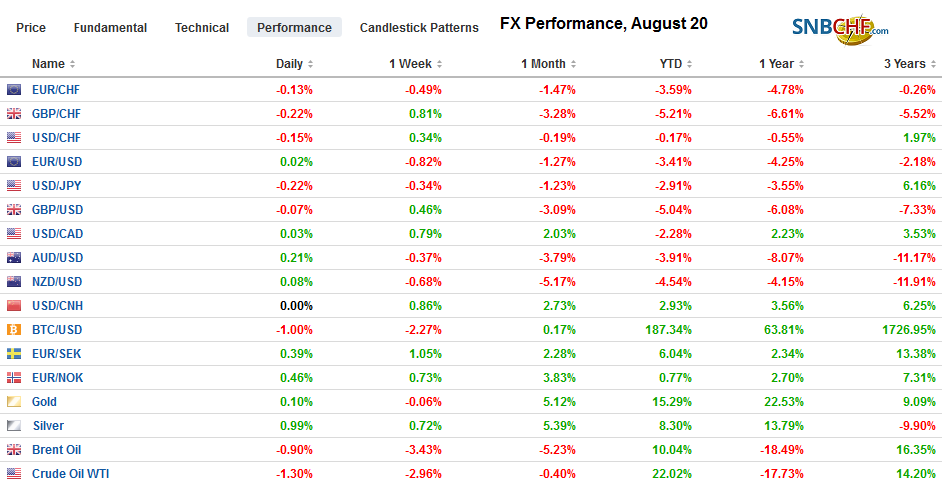

FX Performance, August 20 - Click to enlarge |

Asia Pacific

The PBOC set the dollar’s reference rate in line with the private sector models (CNY7.0454). However, pressure on the yuan remains. Spot is near CNY7.0640, and the dollar peaked on August 12 near CNY7.07. The spread between the onshore (CNY) and offshore (CNH) has narrowed. The dollar peaked against the offshore yuan on August 6 at CNH7.14. The rate reform China announced over the weekend generated a smaller decline in rates than many observers expected. The new way the Loan Prime Rate is set changed, but it produced a six basis point decline to 4.25% from 4.31%.

Japan’s 20-year bond sales saw a slightly better reception than expected, helping yields ease a touch today. Separately, Japan’s Security Dealers Association reported today that foreign investors bought the most ultra-long Japanese bonds (20-years+) in three years last month. Foreign investors bought JPY485 bln (~$4.5 bln) of JGBs that originally had maturities of 20 years or longer. Foreign investors still prefer shorter-term paper and bought JPY2.1 trillion of two-five year government bonds.

The minutes from the Reserve Bank of Australia’s recent meeting were more balanced than many expected. Although the central bank says it is prepared to ease again if necessary, the tone was more optimistic. It noted more favorable economic backdrop with tax cuts, infrastructure spending, the past easing, and the softer Australian dollar. Australian stocks rallied, with the benchmark gaining 1.2%, the most in two months.

The dollar is snapping a three-day advance against the yen that was unable to overcome the JPY107 hurdle. There are about $1.2 bln in expiring options today struck at JPY106.90 and JPY107.00. A more relevant option may be the $550 mln at JPY06.30. European activity has seen the dollar pushed lower. The Australian dollar is firm, but it is not going anyplace quickly. It stalled in front of $0.6800, which it has not traded above since the middle of last week. Even then, it needs to punch through $0.6820 to be noteworthy.

Europe

UK Prime Minister Johnson has more drama around it, but his position, at the end of the day, is not much different than his predecessor. They both recognize the importance of avoiding a hard Irish border, but neither like the backstop and seek “alternative arrangements” without really proposing a concrete workable alternative. Johnson’s combative tone was supposed to send a message to the EC that is serious about leaving if needed without an agreement. However, this appears to have won over exactly no one. Sterling has remained pinned in the $1.20-$1.22 trough since the start for the month. It appears that EC officials are bracing the no-deal exit in a little more than two months.

| Germany will sell 2 bln euro of 30-year zero-coupon bonds. It borrows money for 30-years and has not debt servicing costs associated. Next week, it will sell 5 bln euros of two-year bonds also with a zero-coupon. This suggests Germany can loosen its purse strings and maintain the “black zero” of its fiscal policy. Again, the main deterrent of a more stimulative fiscal plan is not the means but the political will. The Bundesbank warned yesterday that the economy may be contracting here in Q3. It would be the second consecutive quarterly decline and the third in four quarters. |

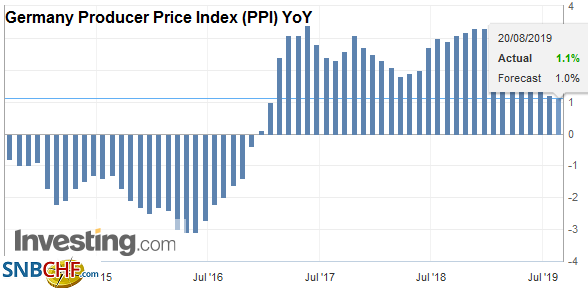

Germany Producer Price Index (PPI) YoY, July 2019(see more posts on Germany Producer Price Index, ) Source: investing.com - Click to enlarge |

As the North American market prepares to open, word from Italy is still awaited. Prime Minister Conte will address the Senate. That may lead to a vote of confidence or his resignation. It is not clear if elections can be avoided or held in sufficient time to allow the 2020 budget to be delivered to the EU on schedule. The point is the political situation is in flux, and it may still take a few days to sort it out. Italian bonds, as one would suspect, are under-performing.

The euro is narrow range below $1.11. It is holding above last week’s low (~$1.1065). Initial resistance is seen near $1.1090 and then $1.1115. The euro is lower for the fifth consecutive session, which is the longest losing streak in three months. Sterling was turned back yesterday after approaching its 20-day moving average (~$1.2190). It has not traded above this moving average in nearly two months. There may be some support near $1.2050, but the $1.20 level is more significant. The selling pressure eased in as the London morning progressed. Resistance in North America is seen in the $1.2120-$1.2140 area. There GBP650 mln in options struck at $1.2160 and $1.2175 that expire today but do not appear in play.

America

The market responded to Huawei’s reprieve in a similar though more subdued way that it responded to last week’s news that the next round of US tariffs would be split. Investors want to read it as a sign of some sort of olive branch to China. It is not. It is not about China. It is about the US. The split in the tariffs was another example of affirmation through negation. After months of claiming that Chinese producers pay for the tariff, last week’s actions implicitly acknowledged that it is American that pay for it. Similarly, the extension of Huawei’s reprieve is limited to where it serves US interests, and that is maintaining the rural networks. Commerce Secretary Ross said that those communities will have an extra 90-days to “wean themselves” off Huawei. At the same time, the US placed another nearly four dozen Huawei units on its blacklist, bringing it to over 100.

The S&P 500 gapped higher yesterday following the gap higher last Friday. The gaps are part of a bullish pattern that could project back to record highs. If last week’s gap (breakaway) marked the end of the correction, yesterday’s maybe a measuring gap, which would project toward 2980. A convincing move above 2850 would confirm the double bottom (~2822) and push through the (61.8%) retracement of the leg down from the July 26 all-time high. The minimum measuring objective of the double bottom projects toward 3080.

Boston Fed President Rosengren, one of two dissents from last month’s decision to cut rates, remains a skeptic. He sees H2 growth around 2% and is not unduly troubled by the brief inversion of the 2-10 yield curve. The market is pricing in a greater chance that the Fed cuts 50 bp next month than standing pat. That is the backdrop for Powell’s Jackson Hole speech at the end of the week. Separately, the White House has denied that it is looking to cut payroll taxes but did acknowledge it was looking at lowering individual income taxes. Such a proposal could put the Democrats in an awkward position. Support the President or vote against household tax cuts.

Fed’s Daly and Quarles speak today in an otherwise light North American calendar. The Canadian dollar remains on the defensive. There is increasing speculation that despite the neutrality of the central bank, the slowing world economy and more Fed cuts in the pipeline will force the Bank of Canada to cut rates this year. The US dollar is knocking around just below the recent highs near CAD1.3345. Support is seen near CAD1.3280. A move above CAD1.3355 would likely signal a move toward the mid-June high around CAD1.3435, and then CAD1.35. The dollar remains firm against the Mexican peso after reaching new highs for the year yesterday (~MXN19.8940). In thin trading so far today, the dollar has held above MXN19.80. The next important target is MXN20.00.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Currency Movements,EUR/CHF,Featured,FX Daily,Germany Producer Price Index,newsletter,SPX,USD/CHF