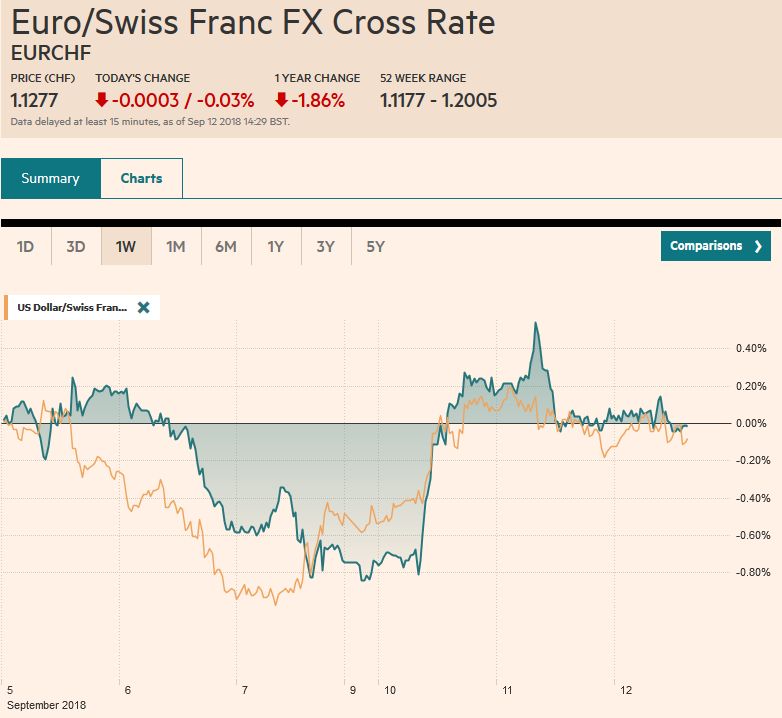

Swiss Franc The Euro has fallen by 0.03% at 1.1277 EUR/CHF and USD/CHF, September 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates The dollar has been confined to about 10 pips on either side of JPY111.55. There are .13 bln of options struck between JPY111.50 and JPY111.65 that expire today. Dollar support extends to JPY111.20-JPY111.30. It has not traded above JPY112.00 since August 1. The euro has chopped between .1570 and almost .1610, staying within yesterday’s ranges. Sterling also remains within yesterday’s range. While a date in November for a special UK-EU summit to sign an agreement is bandied about, the other side of the problem, the cabinet, and

Topics:

Marc Chandler considers the following as important: 4) FX Trends, CAD, EUR, Eurozone Industrial Production, Featured, FX Daily, GBP, JPY, newsletter, SPY, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.03% at 1.1277 |

EUR/CHF and USD/CHF, September 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe dollar has been confined to about 10 pips on either side of JPY111.55. There are $1.13 bln of options struck between JPY111.50 and JPY111.65 that expire today. Dollar support extends to JPY111.20-JPY111.30. It has not traded above JPY112.00 since August 1. The euro has chopped between $1.1570 and almost $1.1610, staying within yesterday’s ranges. Sterling also remains within yesterday’s range. While a date in November for a special UK-EU summit to sign an agreement is bandied about, the other side of the problem, the cabinet, and Parliament are digging in for a fight. There is talk of a leadership challenge. The Bank of England meets tomorrow, and a unanimous decision on rates is widely expected after last month’s hike. The market does not anticipate another rate hike until after Brexit at the end of March 2019. |

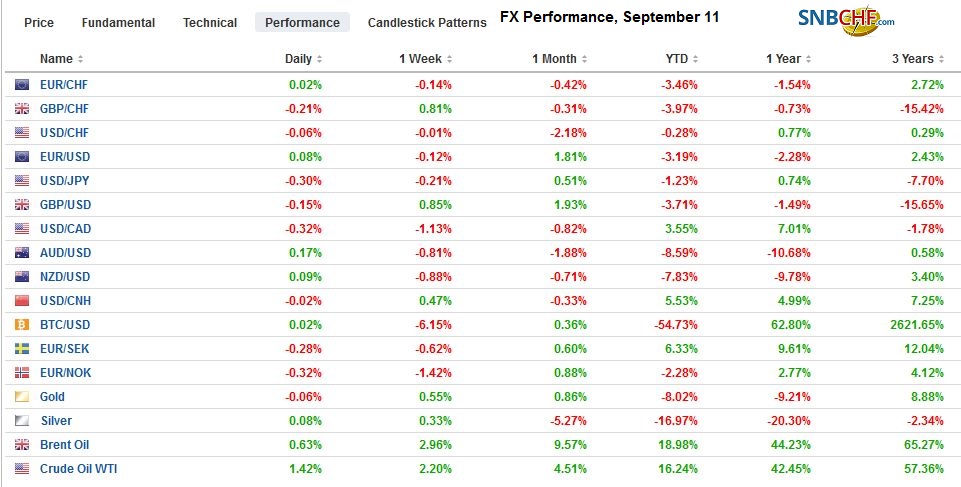

FX Performance, September 12 - Click to enlarge |

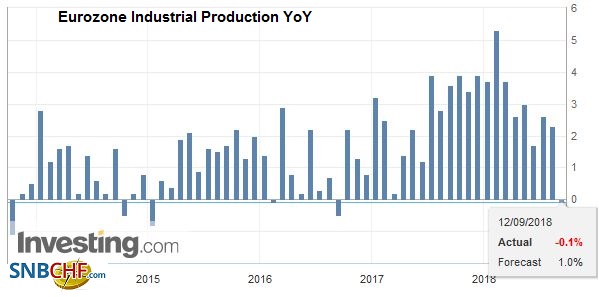

EurozoneEurostat confirmed that EMU industrial output fell for a second consecutive month in July. The 0.8% decline was larger than expected and is the third decline of such a magnitude in four months and weighed on the euro. German and Spanish industrial output had surprised on the downside last week, and Italy matched suit today with a report showing a 1.8% contraction, much larger than expected, and bringing the year-over-year rate to -1.3% (workday adjusted). It is the largest decline since January 2015. |

Eurozone Industrial Production YoY, Oct 2013 - Sep 2018(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

We had anticipated that the ECB staff would shave its growth forecasts, which are announced tomorrow. In June, the staff forecast 2.1% growth this year slipping to 1.7% next year. France took the jump on the ECB by revising its growth down to 1.7% this year and next from 2.0% and 1.9% respectively. The poor economic data and softer forecasts come at a difficult time for Europe as next year’s budgets are prepared.

Slower growth translates into larger deficit as a percent of GDP. France revised its deficit projection to 2.6% this year from 2.3% and next year 2.8% of GDP rather than 2.4%. Although the Italian government has been making more investor-friendly comments, which have been rewarded by bond market investors, the room to maneuver is limited. Moreover, the decline in the sovereign yield and premium over Germany may be having a diminishing impact on bank shares, which are off 1.4% at pixel time while the benchmark yield is about two basis points lower.

Meanwhile, the EC’s confrontation with Hungary may come to a head today. It is threatening sanctions over what is seen as a crisis of democracy. A 2/3 majority is needed to approve sanctions under Article 7. If the EU cannot muster the support, it may embolden others and what has been dubbed the rise of ‘illiberal democracies.”

In Asia, stocks remained under pressure. The MSCI Asia Pacific Index fell 0.2% to extend the losing streak for a 10th consecutive session, the longest run since 2002. The contrast is stark. The Topix and Shanghai Composite, as well as the leading markets in Europe, like the DAX, CAC, FTSE-Milan, and the FTSE 250 are all below the 50-and 200-day moving averages. The US S&P 500 posted a bullish outside up day yesterday and is within two percent of the record high seen in late August. European shares are firmer today, rising 0.2% near midday. The latest fund tracker reports showed European equity funds saw the first inflow in nearly six months. The S&P 500 is up 8% year-to-date coming into today’s session, while the Dow Jones Stoxx 600 is down 3.3%.

The Canadian dollar is holding on to the bulk of yesterday’s gains, with the last surge sparked by reports that it is willing to make a concession on dairy, a sector not included in the current NAFTA. White House economic adviser Kudlow suggested that this was a major stumbling block. However, many had anticipated Canada to make this move as it had already signaled its intention and had done the same thing to strike a deal with the EU. Other more serious hurdles seem to remain. These include anti-dumping panels, a sunset clause, intellectual property rights and patents for pharma, and protection for what Canada calls cultural industries.

Of course, NAFTA is not the only consideration for the Canadian dollar. The Bank of Canada widely expected to hike rates next month. The OIS market appears to be discounting a bit more than an 85% chance of rate increase. US dollar support is seen in the CAD1.3000-CAD1.3020 area.

South Korea reported an unexpected jump in August unemployment (4.2% from 3.8%), and this makes it more difficult for the central bank to hike interest rates. It may have to resort to macroprudential measures if it wants to curb surging property prices. India reports CPI and industrial production. Both are expected to have eased. The dollar initially rose to new record highs against the rupee before recovering on the back of reports suggesting new measures will be announced to support the currency early next week (following a planned economic review this weekend.

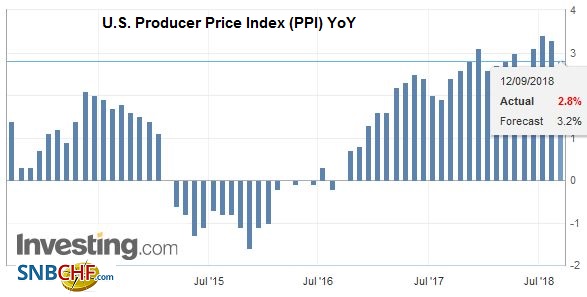

United StatesThe US session features the August PPI and the Fed’s Beige Book ahead of the meeting on September 26. Governor Brainard speaks a little after midday in Detroit, and Fed President Bullard speaks in Chicago shortly after the stock market opens. A rate hike is as done of a deal as these things get. The EIA oil inventory figures will also receive attention after the API estimated an 8.63 mln barrel draw. Analysts had expected a 2.7 mln barrel build. The $9-$10 a barrel spread between WTI and Brent has helped US step up its oil exports, while the EIA shaved US output projections. |

U.S. Producer Price Index (PPI) YoY, Oct 2013 - Sep 20181(see more posts on U.S. Producer Price Index, ) Source: investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$CAD,$EUR,$JPY,Eurozone Industrial Production,Featured,FX Daily,newsletter,SPY