Spring is around the corner in the Northern Hemisphere, and with it, a sense of a Goldilocks moment. Growth is sufficiently strong to see employment grow and absorb the economic slack. In the US, the participation rate of the key 25-54 aged demographic group has risen and now stands at 89.3%, the highest since 2010. Europe enjoys the broadest economic expansion in more than a decade, and while Japanese growth has not been stellar, the expansion is the longest in 30 years and given it shrinking population, continues to do well on a per capita basis. Meanwhile, and importantly, price pressures have been less than expected despite the explosion of central bank balance sheets. This allows the central banks to

Topics:

Marc Chandler considers the following as important: EUR, Featured, FX Trends, JPY, newsletter, SPY, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Spring is around the corner in the Northern Hemisphere, and with it, a sense of a Goldilocks moment. Growth is sufficiently strong to see employment grow and absorb the economic slack. In the US, the participation rate of the key 25-54 aged demographic group has risen and now stands at 89.3%, the highest since 2010. Europe enjoys the broadest economic expansion in more than a decade, and while Japanese growth has not been stellar, the expansion is the longest in 30 years and given it shrinking population, continues to do well on a per capita basis.

Meanwhile, and importantly, price pressures have been less than expected despite the explosion of central bank balance sheets. This allows the central banks to either raise rates gradually (Federal Reserve, Bank of England, and the Bank of Canada) or continue to pursue an aggressive monetary course (ECB, Bank of Japan, Swiss National Bank).

It has been a common refrain among central bankers in different stages of the monetary cycle to assure investors that they are data-dependent. The monetary playbook was being written on the fly since the Great Financial Crisis, but it was not a pure ad hocery exercise. However, the major central banks seem to be on a well-defined course over the next several months, rendering the data, barring a significant surprise, superfluous.

Here is what we know: The Bank of Japan will continue its combination of Qualitative and Quantitative Easing and Yield Curve Control until inflation is nearer to its target, which officials currently project to be in the fiscal year beginning April 2019. The ECB is going to buy 30 bln euros of assets through September, and most likely reduce its buying further in the fourth quarter. A rate hike, which will begin with the deposit rate at minus 40 bp, will start “sometime” after the net purchases have been completed, which we would pencil in for mid-2019.

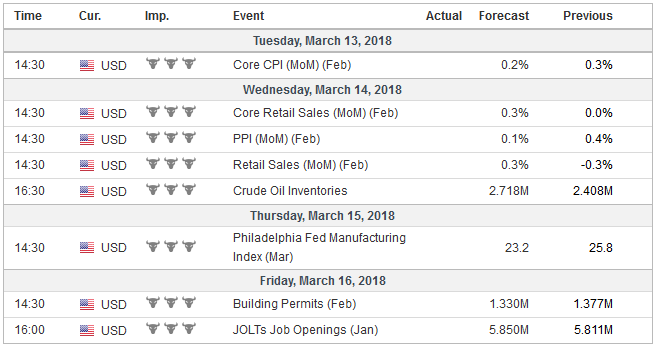

United StatesThe Federal Reserve is more confident that the US economy is on track toward achieving its dual mandate. In recent weeks, the market expectations have converged with the Fed’s forecasts for three rate hikes this year. The risk of four hikes is greater than two, but tactically, such a decision need not be made for several months. Throughout the cycle, the market has not been as aggressive as the Fed’s forecasts, which suggests that talk that the Fed is somehow behind the curve is exaggerated. Fed Chief Powell offered the imagery that captures what appears to be the consensus at the central bank. What were headwinds have become tailwinds. The dollar is not appreciating, and global growth is the best in at least a decade. Oil prices have risen. Fiscal policy is stimulative. This means that the high-frequency economic data in the coming days may spur reactions to the headlines but are unlikely to alter expectations for Fed policy. This seems likely to be the case despite the fact that the economic reports are top shelf, CPI, retail sales, and industrial output. The composition of US growth is changing from last quarter. Industrial output surged in Q4 17, spurred by the recovery from the devastating storms, and appears to be slowing considerably at the start of the year. The consumer is also a little less buoyant. A 0.3% rise in February retail sales would simply offset the 0.3% decline in January, leaving a flat performance. The components that feed into GDP may hold in a bit better, but together January-February may average near trend of 0.2%. Both the Atlanta and New York Fed’s GDP tracking models have eased in recent weeks and now stand at 2.5% and 2.8% respectively. Consumer price pressure is stable. January’s outsized 0.5% monthly increase will not be repeated. Economists look for a 0.2% increase in February, which would lift the headline pace 2.2% from 2.1%. Due to the base effect, a 0.2% rise in the core rate will keep the year-over-year rate steady at 1.8%. |

Economic Events: United States, Week March 12 - Click to enlarge |

EurozoneJapan and Europe have a light economic calendar. Europe features industrial production. Soft PMI data and the unexpected decline in German industrial output, for the second consecutive month (-0.1% after a -0.5% in January, the median expectation was for a 0.6% increase) point to a soft report. Real sector data are expected to confirm the survey data that warns the economy lost some momentum since the start of the year. The seems to contrast with the ECB staff that raised this year’s growth forecast by a tenth of a percent to 2.4%. Leave aside the false impression of precision, there seemed to be a reluctance to recognize the loss of momentum and the tightening of financial conditions. Market rates have risen. Equities have weakened (and are underperforming). The euro has appreciated. Financial conditions are less supportive. |

Economic Events: Eurozone, Week March 12 - Click to enlarge |

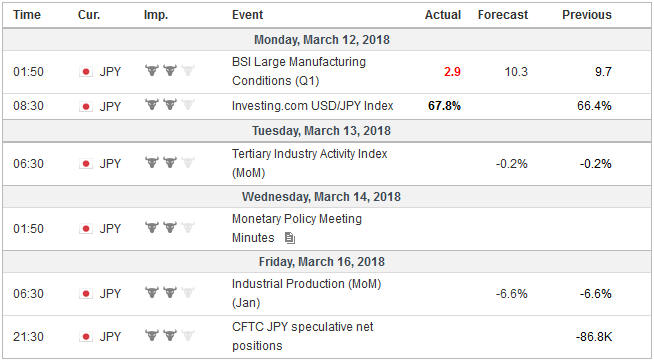

JapanJapan’s weekly portfolio flows reported by the MOF may draw more attention than usual. It is not unusual for Japanese investors to repatriate some of their overseas investments around the turn of the fiscal year. However, what should not be lost in the seasonality were the comments by the head of the Government Pension Investment Fund (GPIF) suggesting that the recent price action has made US bonds more attractive. Recall that previously the cost of hedging was prohibitive. More interesting than the largest weekly bond sales by Japanese investors in several years, foreign investors stepped up their purchases of Japanese bonds. The JPY1.27 trillion Japanese bonds they bought was the most in six months. Since the bonds are obviously not sought because of their high yields (Japan’s yield curve is negative out through eight years), it is interesting to contemplate the motivation. Is it an expression of a bullish yen view? Is it about moving toward benchmarks? Does it have to do with the funding side? Next week’s data may not shed light on the motivation but will show whether it was a one-off. |

Economic Events: Japan, Week March 12 - Click to enlarge |

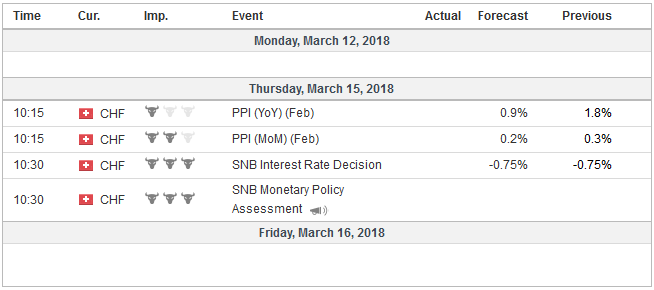

Switzerland |

Economic Events: Switzerland, Week March 12 - Click to enlarge |

The prospects of a trade war have increased given the US tariffs on steel and aluminum. However, at the last minute, President Trump shifted and opened the door to exemptions, including for Canada and Mexico. Australia experiences a bilateral trade deficit with the US cooperates in military matters, and may also be in line to be granted dispensation.

However, the fear of a trade war seems to be much greater than when Obama put tariffs on tires, and Bush slapped a 30% tariff on steel (with many exemptions). However, outside of some symbolic moves, the most likely course of action based on precedent and game theory, would suggest avoiding a tit-for-tat trade war, which would do more to weaken the multilateral trade order than the US tariffs. Instead, challenging the US action at the WTO strengthens the rule of law and is strategically and tactically the most likely course.

The prospect of a summit between North Korea and the United States saw Japanese and Korean stocks rally at the end of the week. On the one hand, the prospects of talks may be a sign of a de-escalation of tensions, which understandably supports risk-on strategies. On the other hand, while the talks are a positive step, this likely simply marks a new phase.

North Korea has a chit, its intercontinental ballistic missile capability that draws the US attention. The development of this power was done purposefully and not simply to denuclearize the peninsula. After all, the US nuclear capability is so much larger than what is in South Korea. The bottom-line if there is a peace dividend to be found in Korea, there is much work to be done before it can be collected.

The concern about higher interest rates and a trade war did not prevent the US stock market to gap higher before the weekend. The NASDAQ closed at new record highs, completely recouping last month’s brief but sharp slump. The S&P 500 also gapped higher, and it is testing the late February high, which is the main technical obstacle in the way of the record.

The US markets have led the equity recovery since the February swoon. In fact, last week, Europe’s Dow Jones Stoxx 600 took out those February lows before recovering. It needs to rise another 2% before it challenges the post-swoon peak, which itself was only half of the earlier decline.

Japanese equities recouped half of the decline seen the middle of February, and both the Nikkei and Topix made a marginal new low last week. However, the recovery was less inspiring, in part the market was closed while the US rallied and dragged up European bourses. This suggests some scope for catch-up, and aided perhaps by the yen’s decline through a 20-day moving average, though limited by frequently seasonal repatriation.

Tags: #USD,$EUR,$JPY,Featured,newsletter,SPY