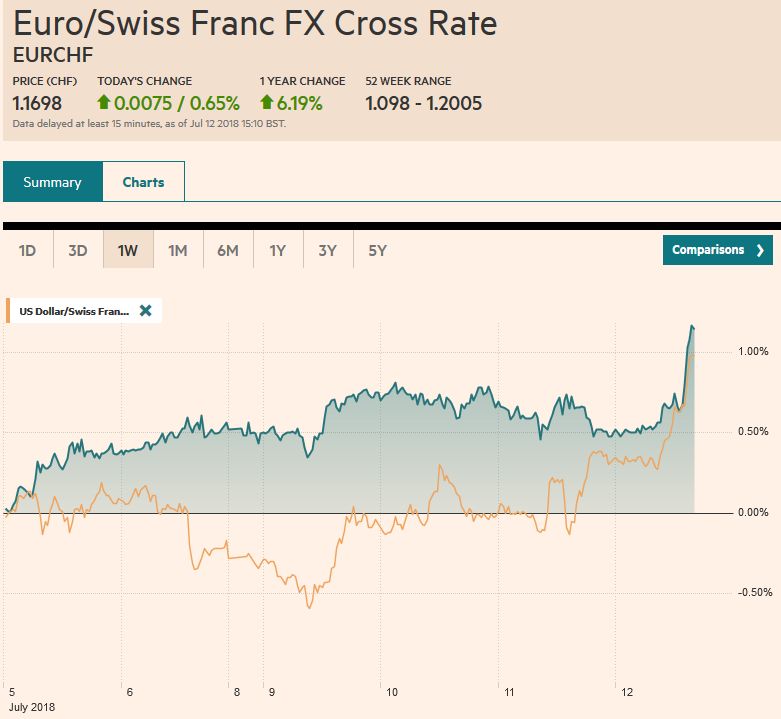

Swiss Franc The Euro has risen by 0.65% to 1.1698 CHF. EUR/CHF and USD/CHF, July 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates The dollar has broken out against the Japanese yen. Despite the global equity drop and decline in US yields, which often underpin the yen, the yen fell to its lowest level since early January yesterday and is continuing to sell-off today. The dollar closed above JPY112 yesterday and is near JPY112.50 today. The high for the year was set on January 8 near JPY113.40. The JPY112.00 option for about 0 mln that expires today looked safe until yesterday. The Swedish krona is rivaling the yen on the downside today after a softer than expected

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, CAD, EUR, EUR/CHF, Featured, FX Daily, GBP, newsletter, Oil, SEK, U.S. Consumer Price index, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.65% to 1.1698 CHF. |

EUR/CHF and USD/CHF, July 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe dollar has broken out against the Japanese yen. Despite the global equity drop and decline in US yields, which often underpin the yen, the yen fell to its lowest level since early January yesterday and is continuing to sell-off today. The dollar closed above JPY112 yesterday and is near JPY112.50 today. The high for the year was set on January 8 near JPY113.40. The JPY112.00 option for about $610 mln that expires today looked safe until yesterday. The Swedish krona is rivaling the yen on the downside today after a softer than expected CPI (0.2% instead of 0.3%) and dovish minutes from the Riksbank meeting earlier this month. Although the central bank has pointed to the likelihood of a hike later this year, the comments from the individual members make it clear this is not a done deal. While the euro is holding above yesterday’s low near $1.1665, it has not been able to recover much and so far today is the first session since last Tuesday that it has not been above the $1.17 level. There are two maturing option strikes that are in play. One is at $1.1675 (~785 mln euros) and the other is at $1.1690 (~570 mln euros). The only data of note was the aggregate industrial production figure for May. Despite disappointing French data earlier this week (-0.2 vs. expectations for +0.7), industrial output jumped 1.3% in the EMU, the strongest since November. Sterling extended yesterday’s losses marginally and dipped briefly below $1.32. It is trapped in a narrow range and has not been above $1.3230 yet today. An option for about GBP400 mln at $1.3225 expires today. Brexit issues are simmering below the surface, and the loss in the World Cup weighs on moods. Rees-Mogg has proposed four amendments that would essentially gut Prime Minister May’s plan and the prospects for passing is the subject of today’s debates. |

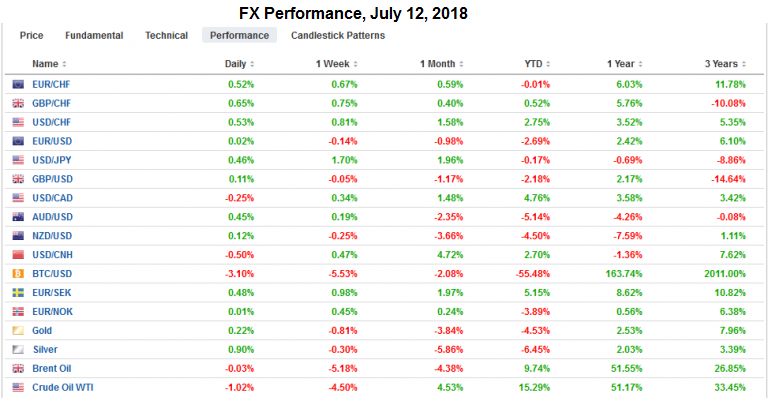

FX Performance, July 12 - Click to enlarge |

The US dollar rallied yesterday as the escalating trade tensions between the world’s top two economies choked off the animal spirits and a marked down in equities and risk assets. It remains firm today even as risk has come back. Equities are mostly higher today and bonds lower. Emerging market currencies, from Turkey to South Africa are firmer, as is the Chinese yuan. The news stream itself is light and some are using suggestions that US and China trade talks will likely resume shortly as a justification for today’s move.

There would, of course, be trade talks, but the clock is ticking ahead of the implementation of tariffs on the next $16 bln of goods. The public comment period on the $200 bln of goods that face an additional 10% levy runs until the end of August. As the list of goods is examined, it is clear that there is more than meets the eye. As Bloomberg reporter Murtaugh points out, on that list was liquified natural gas from China, which the US does not import. Some items in the first round of $34 bln are not even traded, like China putting a tariff on piped natural gas from the US.

Trump’s strident tone at the NATO summit may not be surprising, but some observers are detecting a further deterioration in US relations with Europe. Scenarios of the US disengagement from Europe include withdrawal of troop, sanctions on the Nord Stream 2 consortium, and tariffs on autos. The US investigation of auto imports on national security ground is expected to be finished by the end of next month.

The MSCI Asia Pacific Index eked out a minor gain of less than 0.1% after yesterday’s 1% drop. However, the magnitude of the gain should not obscure the breadth. All the markets were higher, with 2%+ gains in China and a 1.2% gain in Japan’s Nikkei. Foreign investors were small buyers of Korea (~$44 mln) bringing this week’s purchases to $132 mln, which is sufficient to turn the flows on the month positive.

European shares are higher, with the Dow Jones Stoxx 600 up about a third of a percent through late morning turnover. All the sectors are higher except for real estate, which is nursing a small loss. The energy sector and financials are barely positive. Yesterday’s drop (~1.25%) snapped a six-day advance and retraced 50% of it in one day. It would not be surprising to see it recover to new highs in the coming days.

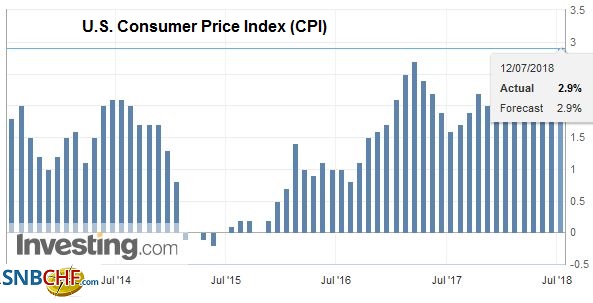

United StatesAttention in the North American session turns toward the US June CPI. The consensus is for a 0.2% increase in both the core and headline figures. After yesterday’s PPI and the firmness in the consumer goods component, we suspect the risk is on the upside. An upside surprise could weigh on the US 10-year note and push the yield toward the upper end of its three-week range which comes in just below 2.90%. After Tuesday’s poor reception to the three-year note sale, yesterday’s 10-year auction went considerably better. Today the US auctions $14 bln 30-year bonds. The dollar may rise with a firm CPI and the Dollar Index is flirting with the 61.8% retracement (~94.85) of the decline since late June. That would likely generate over-extended intraday technical signals before it can reach that late June high near 95.50. |

U.S. Consumer Price Index (CPI) YoY, Jul 2013 - Jul 2018(see more posts on U.S. CPI, ) Source: investing.com - Click to enlarge |

The Bank of Canada hiked rates as widely expected, and even though the Canadian dollar gave back its initial gains, it was not the Governor Poloz was dovish. The central bank revised up its forecast for US growth and given the elasticities and knock-on effects, one can estimate Canada’s exports to the US. Despite the tariffs, counter-tariffs and other trade tensions, Poloz expects export growth. Canada’s housing market has stabilized, and the terms of trade have improved. The tariff impact was judged to be modest. The Canadian dollar, however, is dragged lower by the general strength of the US dollar and the a

Oil prices are stabilizing after yesterday’s plunge, the largest in a couple of years. Brent was off nearly 7% on heavy volume, while WTI fell 5%. Reports suggest there were strong demand for September $80 calls. The slide in prices came despite the large drop in US crude inventory (12.6 mln barrel decline last week, the most since 2016). The drawdown was twice what the industry survey showed. Several considerations were at work. Libyan shipments were resuming. The trade tensions gave rise to demand concerns. The strong dollar did not do oil any favors, even if the correlation has weakened. More Iranian oil may come to market if the US grants some waivers. There was also speculation that the Trump will press Putin to boost Russia’s oil output, and that the Saudis would increase their oil sales to the US.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$CAD,$CNY,$EUR,EUR/CHF,Featured,FX Daily,newsletter,OIL,SEK,U.S. Consumer Price Index,USD/CHF