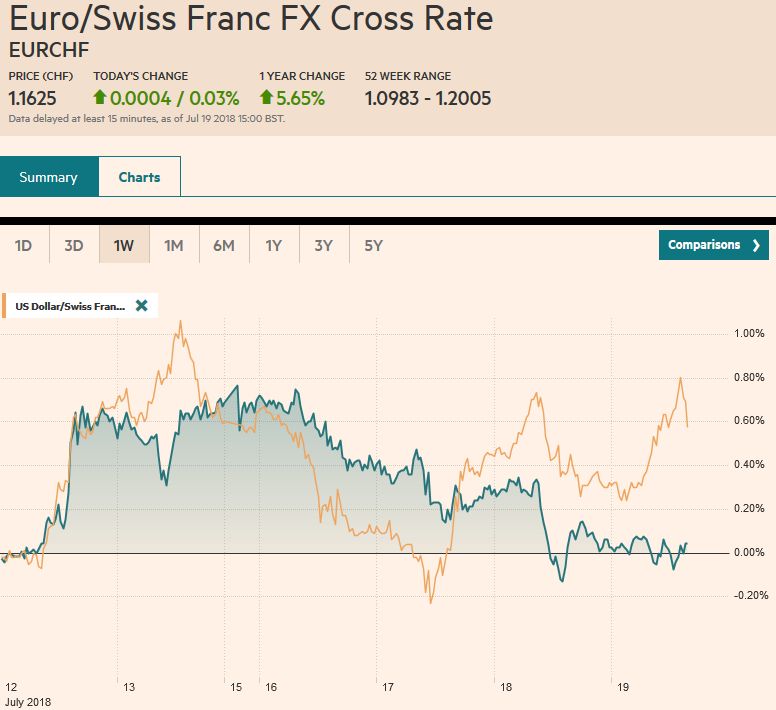

Swiss Franc The Euro has risen by 0.03% to 1.1625 CHF. EUR/CHF and USD/CHF, July 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates The US dollar is extending its recent gains against most of the world’s currencies. We continue to see the most compelling case for the macro driver being the diverging policy mixes. There are also more immediate factors too. The surprisingly poor UK retail sales report, for example, managed to do what the Brexit chaos and softer than expected CPI fail to do. Namely, push sterling below .30 for the first time since last September. Sterling fell about .2985. The battle for .30 continue, and there is a large GBP2 bln option there that is

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CAD, EUR, Featured, GBP, Japan Trade Balance, JPY, newslettersent, U.K. Retail Sales, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Swiss FrancThe Euro has risen by 0.03% to 1.1625 CHF. |

EUR/CHF and USD/CHF, July 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is extending its recent gains against most of the world’s currencies. We continue to see the most compelling case for the macro driver being the diverging policy mixes. There are also more immediate factors too. The surprisingly poor UK retail sales report, for example, managed to do what the Brexit chaos and softer than expected CPI fail to do. Namely, push sterling below $1.30 for the first time since last September. Sterling fell about $1.2985. The battle for $1.30 continue, and there is a large GBP2 bln option there that is expiring today. Technically, the next target is closer to $1.28. In fairness, the risk that the UK leaves the EU at the end of next March (maybe a small extension is possible, according to City AM report) without an agreement, in which case, a return to the flash crash low from October 2016 cannot ben ruled out. The dollar recovered from the earlier softness that saw it test the JPY112.65 area at the start of the Asian session, but as US traders returned, it is near session highs above JPY113.00. There is a $634 mln option struck at JPY113 that will be cut today and an option at JPY113.20 ($700 mln) expires. It is unclear where the top of the dollar’s new range. We suspect it will be near JPY114, but this does not preclude some pushing past it, perhaps even nearer JPY115. The euro has been pushed below $1.16 for the first time in two and a half weeks. It seems to be more a function of dollar strength than euro weakness now. There is an option struck at $1.16 (667 mln euros) that expires today. For two months, the euro has been traversing a roughly $1.15-$1.850 trading range on the wide. |

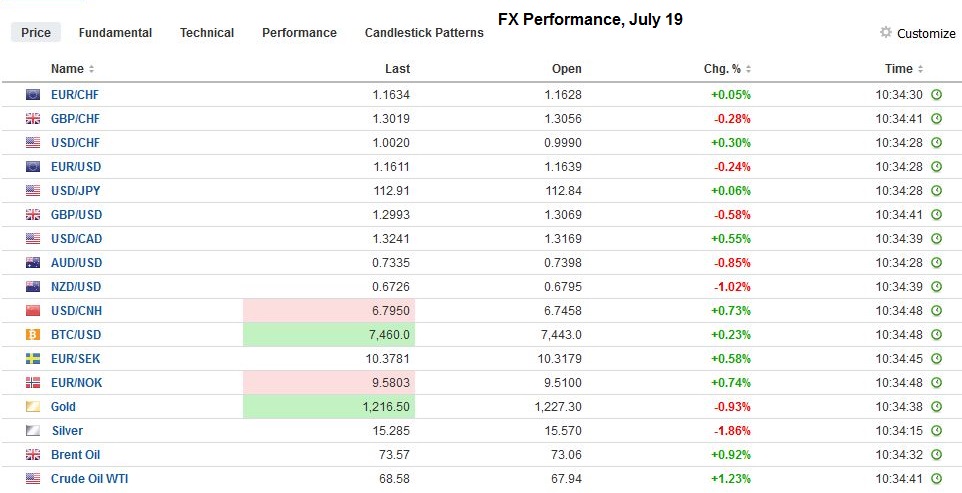

FX Performance, July 19 - Click to enlarge |

United KingdomUK consumers returned in Q2, but the quarter ended on a soft note. Retail sales, excluding gasoline and diesel, fell 0.6%. The market looked for a small gain, perhaps flattered by the World Cup merchandising, after a 1.4% rise in May (revised from 1.3%). But now the thought is that maybe the event kept people from shopping. Foods sales were strong and on a quarterly basis, were the strongest since 2001. While the data disappointed, the outlook for the August 2 BOE meeting is unchanged. The implied yield of the September short-sterling futures contract is half a basis point lower at 82 bp. It is virtually unchanged thus far in July. |

U.K. Retail Sales YoY, Aug 2013 - Jul 2018(see more posts on U.K. Retail Sales, ) Source: investing.com - Click to enlarge |

JapanJapan also reported a larger than expected June trade surplus. After falling into deficit in May, the balance swung back to surplus in June. The June surplus of JPY721.4 bln compares with economists forecasts of closer to JPY530 bln and the May deficit of JPY578 bln. The surplus appears to be the result of weaker imports rather than export strength. Exports grew 6.7% from a year ago (8.1% in May), while import growth slowed to a 2.5% year-over-year pace (from 14.0% in May). Export growth in Japan is slowing. Exports to China and EU rose, while exports to the US slipped (less than 1%) but is the first decline for nearly a year and a half. Imports from the US fell 2.1%. Japan’s records show a small increase in the surplus with the US from a year ago (0.5%). |

Japan Trade Balance, Jul 2013 - Jul 2018(see more posts on Japan Trade Balance, ) Source: investing.com - Click to enlarge |

Even strong data though may not be sufficient to block currencies from weakening in the face of the dollar demand. Australia reported as strong of jobs data as imaginable, and the Australian dollar has been unable to hold on to its initial gains and near $0.7350 is off more than 0.5%. Australia created 50.9k net new jobs in June, three times more than most expected, and of these, 41.2k were full-time jobs. It has created a bit more than 13k jobs in May while it lost almost 20k full-time positions, after the minor revisions. The participation rated jumped to 65.7% from 65.5%, but the unemployment rate was steady at 5.4%.

The yen is the best performing of the majors, only down slightly against the dollar. Two developments could have seen the yen strengthen today. First, the BOJ reduced the quantity of long bonds it was buying. It trimmed the buying in the 10-25-year bucket by JPY10 bln and the 25+ bucket by a similar JPY10 bln. The market barely paid attention. Indeed yields through 20-years softened, and the yield of the 30-year bond edged 2/10 of a basis point higher, still pinned at two-year lows.

The US dollar settled poorly against the Canadian dollar yesterday (possible shooting star candlestick), but it has come roaring back today. A move above CAD1.3265 could signal a new fresh assault on the year’s high seen in late June near CAD1.3385.

China’s yuan fell nearly 0.9% against the US dollar, the most in Asia today, and the second worst performing in the emerging market space after the 1.3% decline in the South African rand. There continues to be speculation that contrary to denials, China has weaponized the yuan. We continue to lean against this view, but recognize that Chinese officials protest against the yuan’s weakness is mute. China has eased policy formally through the required reserve ratio reduction and informally, by pressuring banks to lend.

Many observers seem to suggest one reason why the dollar is strong against all the major currencies and emerging market currencies, but have a unique explanation for the yuan’s weakness. As if the market forces would lift the dollar against all the world’s currencies except the yuan and the yuan’s weakness is manipulation. Given the divergence of policy, the slowing of the Chinese economy, debt worries, which the S&P highlighted another dimension (embedded put options in some debt instruments), all Chinese officials have to do is allow market forces to be expressed. Ironically, it seems like it is the neoliberals who want China to intervene and arrest the yuan’s decline. The dollar is near CNY6.78. It finished last month near CNY6.62. There is increased talk of a move toward CNY7.0.

The US calendar is light. The weekly initial jobless claims, however, cover the week of the July non-farm payroll survey and the Philly Fed provides insight into the start of Q3. Although it is not a market mover, the Leading Economic Indicator for June will be reported and is expected to have risen by 0.4% after a 0.2% increase in May. Concerns about a slowing of the US economy or a possible downturn are not so much a 2018 story and H2 2019 and 2020.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,Featured,Japan Trade Balance,newslettersent,U.K. Retail Sales