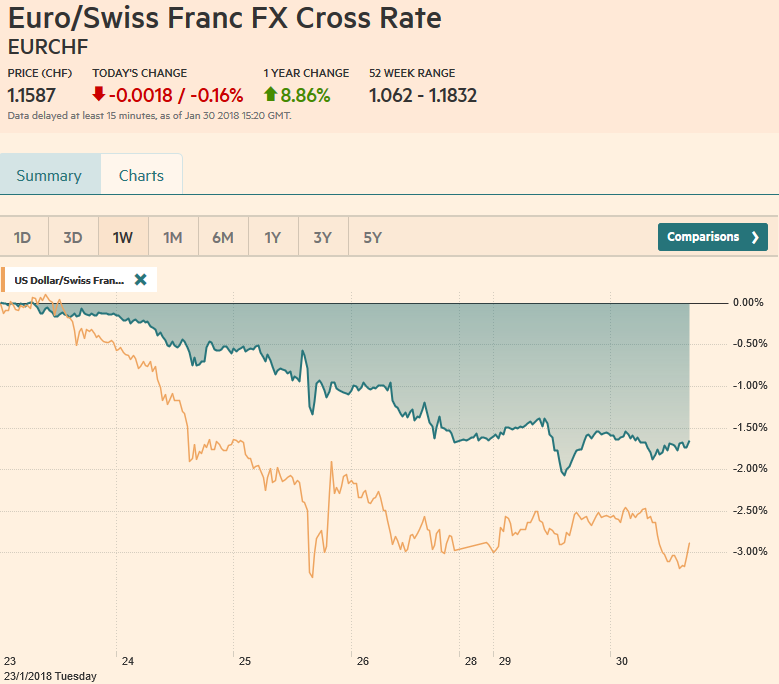

Swiss Franc The Euro has fallen by 0.16% to 1.1587 CHF. EUR/CHF and USD/CHF, January 30(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates The US dollar is paring yesterday’s gains, and the 10-year Treasury yield has slipped back below the 2.70% level after pushing 2.73% briefly. European bonds have also eased, with yields one-two basis points lower. It is thus far a mild Turn Around Tuesday but suggests that the market psychology that has driven the dollar lower and yields higher persistently since mid-December have not been broken. One implication is that since these markets do not act in a vacuum is that equities will likely also recover, though it is not evident yet.

Topics:

Marc Chandler considers the following as important: EUR/CHF, Eurozone Consumer Confidence, Eurozone Gross Domestic Product, Featured, France Gross Domestic Product, FX Trends, Japan Household Spending, Japan Retail Sales, Japan Unemployment Rate, newsletter, Spain Gross Domestic Product, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.16% to 1.1587 CHF. |

EUR/CHF and USD/CHF, January 30(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

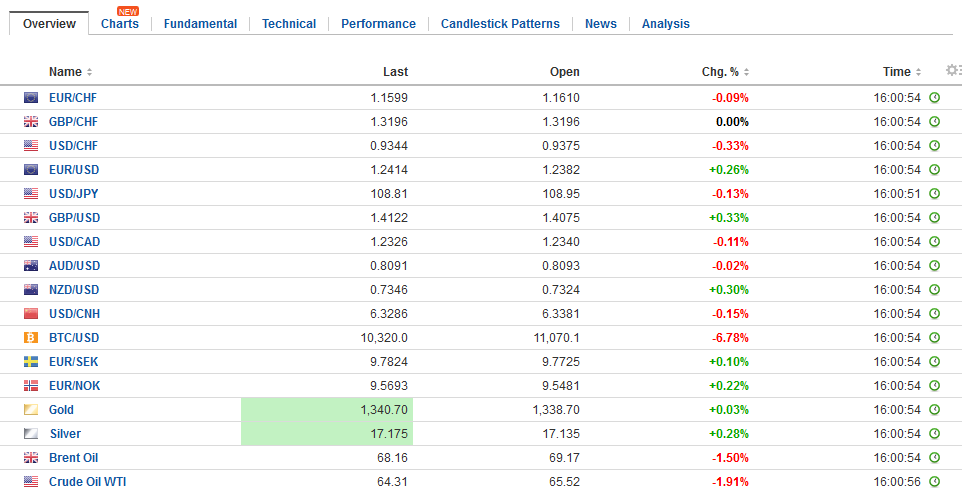

FX RatesThe US dollar is paring yesterday’s gains, and the 10-year Treasury yield has slipped back below the 2.70% level after pushing 2.73% briefly. European bonds have also eased, with yields one-two basis points lower. It is thus far a mild Turn Around Tuesday but suggests that the market psychology that has driven the dollar lower and yields higher persistently since mid-December have not been broken. One implication is that since these markets do not act in a vacuum is that equities will likely also recover, though it is not evident yet. The MSCI Asia Pacific Index pulled back by a little more than 1% for the largest loss since early December. No regional market was unscathed, though the regional leader has been Korea’s KOSDAQ and it was down marginally (almost 0.7%), leaving it up 15.3% so far this month. The Hong Kong Enterprise Index that tracks China’s H-shares fell nearly 2% to bring this month’s gain to a still-amazing 14.4%. |

FX Daily Rates, January 30 - Click to enlarge |

| In Europe, the Dow Jones Stoxx 600 gapped lower. It is trying to fill that gap in the early turnover, but all the main bourses are still lower on the day, and the S&P 500 is trading about 0.25% lower.

The news stream is picking up. Japan reported employment and consumption, while the focus in Europe is on Q4 GDP, but also Germany’s preliminary inflation reports ahead of tomorrow’s advance estimate for EMU. In the US, the focus is on President Trump’s first State of the Union speech. |

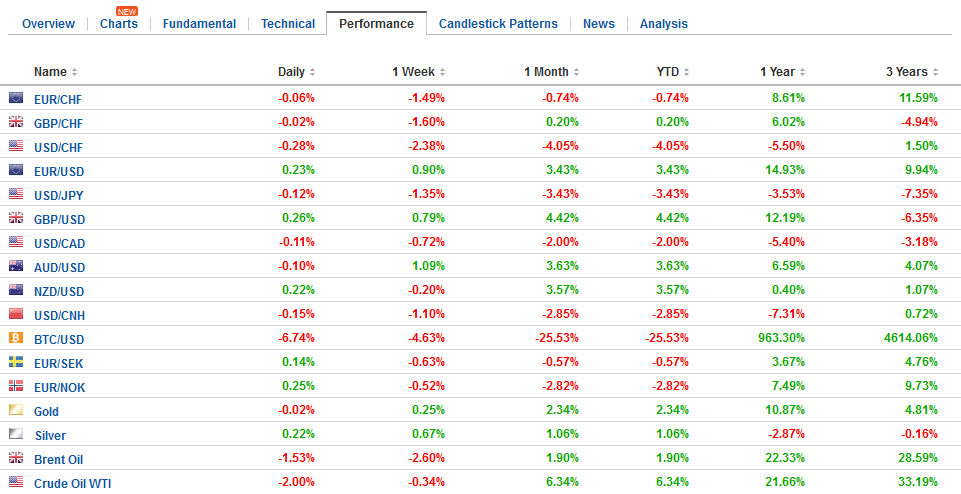

FX Performance, January 30 - Click to enlarge |

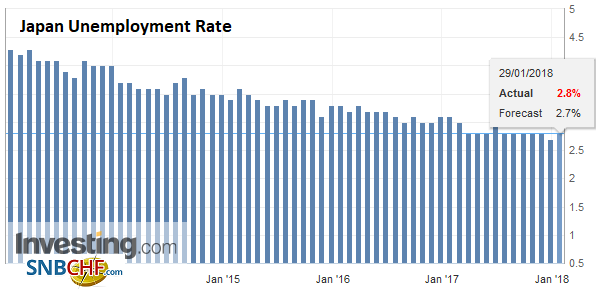

JapanJapanese unemployment unexpectedly ticked up to 2.8% from 2.7%, but it appears to have been driven by people leaving jobs, which is also in this context, a sign of the tightness of the labor market. Jobs-to-applicants rose to a new high of 1.59 from 1.56. |

Japan Unemployment Rate, Dec 2017(see more posts on Japan Unemployment Rate, ) Source: Investing.com - Click to enlarge |

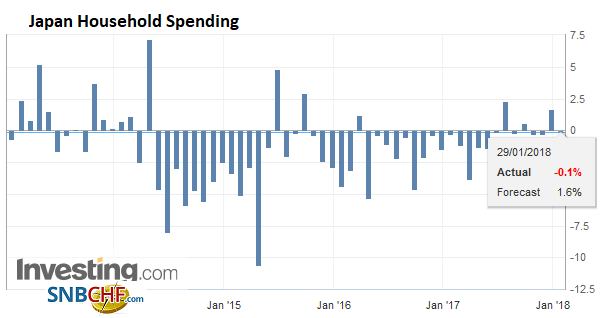

| On the other hand, overall household spending was poor. In December, it stood at -0.1% year-over-year. The median in the Bloomberg survey was for a 1.3% rise after 1.8% in November. |

Japan Household Spending YoY, Dec 2017(see more posts on Japan Household Spending, ) Source: Investing.com - Click to enlarge |

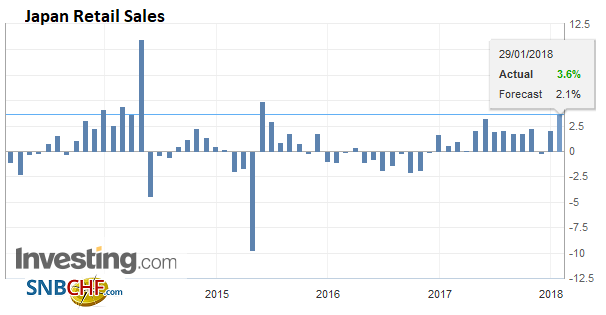

| Retail sales held up better, rising 0.9% rather than fall by 0.4% as the median had forecast. |

Japan Retail Sales YoY, Dec 2017(see more posts on Japan Retail Sales, ) Source: Investing.com - Click to enlarge |

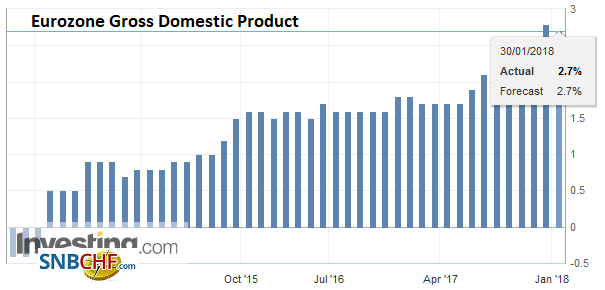

EurozoneIn the eurozone, Q4 GDP was in line with expectations. It rose 0.6% for a 2.7% year-over-year rise. The asymmetrical risk we thought was on the upside, but this impulse was picked up in Q3, with an upward revision to 0.7% from 0.6%. |

Eurozone Gross Domestic Product (GDP) YoY, Q4 2017(see more posts on Eurozone Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

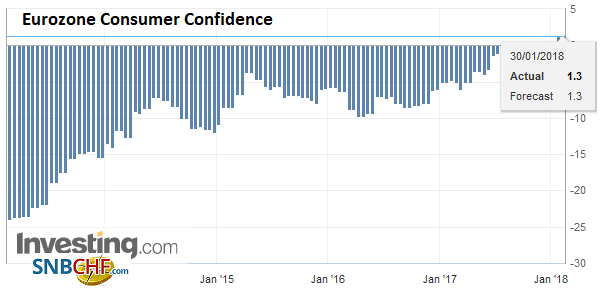

Eurozone Consumer Confidence, Jan 2018(see more posts on Eurozone Consumer Confidence, ) Source: Investing.com - Click to enlarge |

|

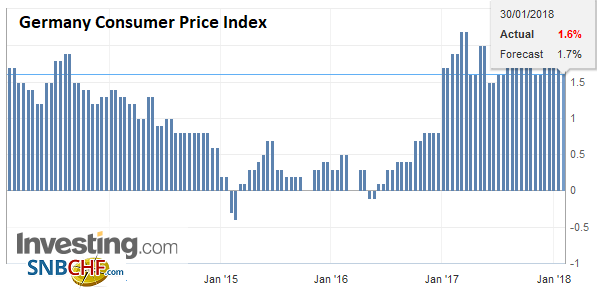

GermanyGerman states reported January CPI figures and the national one will be reported shortly. German inflation typically falls in January. A 0.7% decline is needed to keep the year-over-year pace steady at 1.6%. The risk may be on the downside after the states’ reports. |

Germany Consumer Price Index (CPI) YoY, Jan 2018(see more posts on Germany Consumer Price Index, ) Source: Investing.com - Click to enlarge |

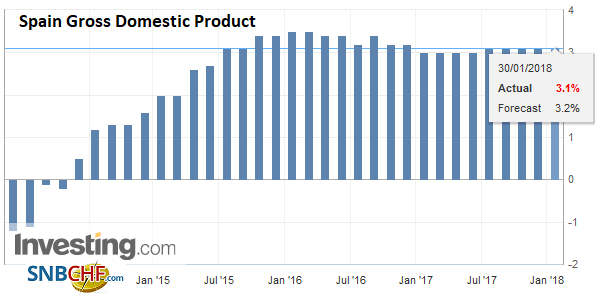

Spain |

Spain Gross Domestic Product (GDP) YoY, Q4 2017(see more posts on Spain Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

France |

France Gross Domestic Product (GDP) QoQ, Q4 2017(see more posts on France Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

The shape of the dollar’s pullback will give a better indication of whether or not the long overdue technical correction is at hand. A move above $1.2440-$1.2460 might see the euro rechallenge its recent highs above $1.25 and probe into the band of technical objectives that extends from around $1.26 to $1.28. Sterling needs to overcome the $1.4120-$1.4160 area to reignite the move higher. Most observers cannot feign surprise that new official studies suggest that under numerous scenarios, after Brexit the UK will be poorer. A break of the JPY108.00-JPY108.30 would be understood as extending the greenback’s slide. The key level in the Dollar Index is a little below 89.00.

Three key events still lie ahead. First is the preliminary EMU CPI. It will be reported tomorrow. Any disappointment will likely weigh on the euro, while an upside surprise, especially in the core rate, will send the single currency higher.

Second is the Yellen’s last FOMC meeting. A hawkish hold is the most likely scenario. It seems politically naive to suggest Yellen may unveil a new initiative, such as a rate hike or announcing a press conference after every meeting (like we have been urging). Institutionally, it is better that the new chair announces whatever changes there are going forward.

The third is the US economic data–auto sales and the employment report. Both are showing late cycle symptoms. Though occasionally masked by short-term volatility, the 12-month moving averages are gradually turning lower.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: EUR/CHF,Eurozone Consumer Confidence,Eurozone Gross Domestic Product,Featured,France Gross Domestic Product,Japan Household Spending,Japan Retail Sales,Japan Unemployment Rate,newsletter,Spain Gross Domestic Product,USD/CHF