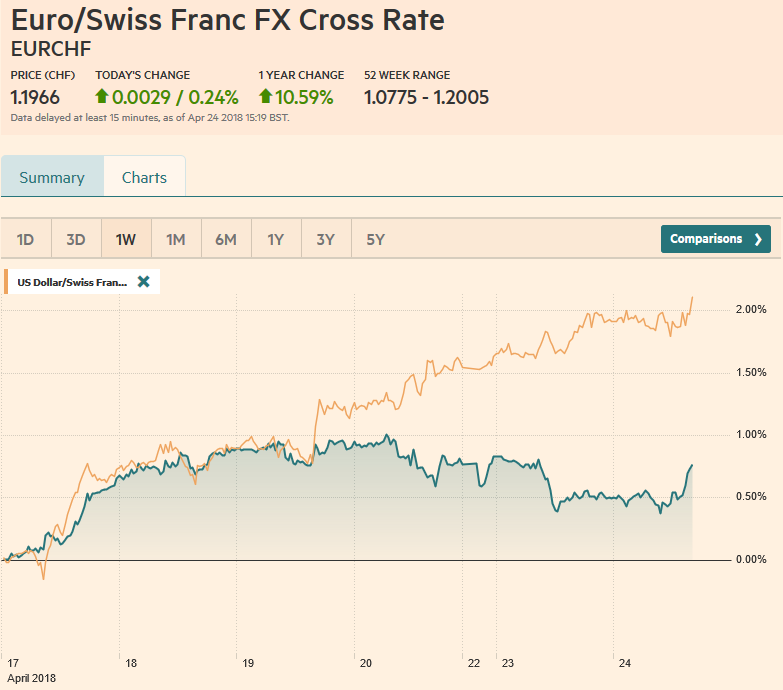

Swiss Franc The Euro has fallen by 0.23% to 1.1944 CHF. EUR/CHF and USD/CHF, April 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge GBP/CHF The pound to Swiss Franc rate has traded in a fairly tight range this week as a lack of any new fresh information to drive financial markets so far. A major driver for the Franc has been risk-sentiment as investors attitudes to risk shape the way they look at investing in certain currencies. As a safe-haven investment, the Swissie has been stronger and weaker according to such demands. Lately, the pound has been very strong helping drive GBPCHF to the post-Referendum highs, now we are seeing a scaling back in the exchange rates as the

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, EUR, EUR/CHF, Featured, GBP, gbp-chf, Germany IFO Business Climate Index, JPY, newslettersent, SPY, U.S. New Home Sales, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Swiss FrancThe Euro has fallen by 0.23% to 1.1944 CHF. |

EUR/CHF and USD/CHF, April 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

GBP/CHFThe pound to Swiss Franc rate has traded in a fairly tight range this week as a lack of any new fresh information to drive financial markets so far. A major driver for the Franc has been risk-sentiment as investors attitudes to risk shape the way they look at investing in certain currencies. As a safe-haven investment, the Swissie has been stronger and weaker according to such demands. Lately, the pound has been very strong helping drive GBPCHF to the post-Referendum highs, now we are seeing a scaling back in the exchange rates as the pound drops lower owing to market concerns. The pound has been boosted by investors believing the Bank of England will raise interest rates in the future but this is by no means a guarantee. Only last week Mark Carney stated a rate hike was not a certainty and more recent economic data has also thrown fresh concerns that perhaps the pound will not just keep rising. With the pound potentially falling if the Bank of England does not raise in May, the pound to CHF exchange rate could be in for a rocky period. This would be evidenced by the recent falls from 1.39-1.36 and there could be much further to fall. If the market loses hope in the recent unwinding of many safe-haven positions that have seen the CHF weaken, GBPCHF could actually soon be sitting closer to 1.30 than 1.40. |

GBP/CHF, April 24(see more posts on GBP/CHF, ) Source: markets.ft.com - Click to enlarge |

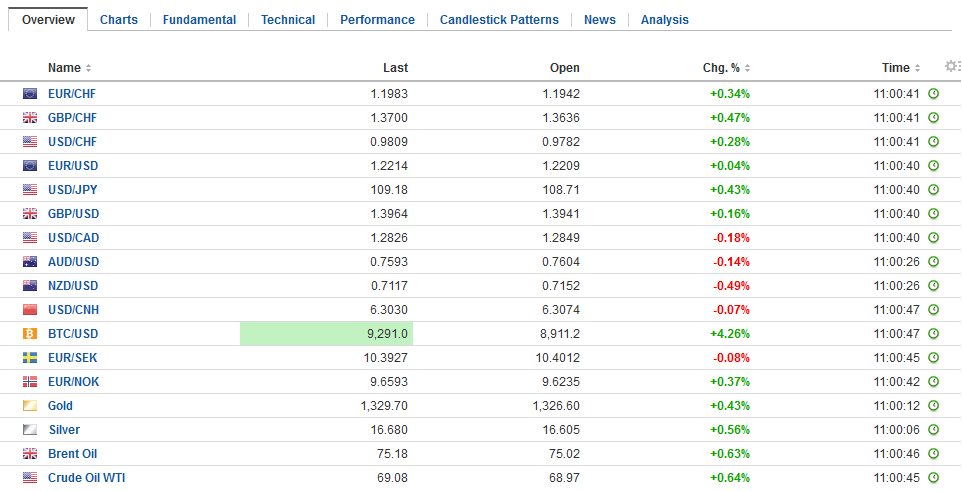

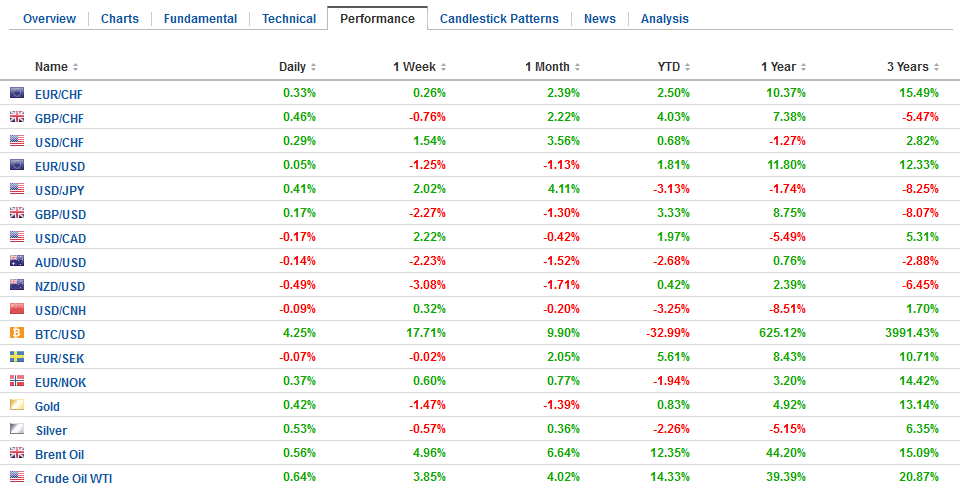

FX RatesThe US dollar looked set to launch a new leg higher, but rates stalled, which in turn is unleashing some mild corrective pressures. The US two-year yield has been unable to extend its increase beyond 2.50%, while the 10-year rate has stalled within a whisker of the 3% psychological threshold. The greenback’s momentum did indeed carry it, but by late morning on the Continent, a consolidative tone was evident. Perhaps it is most clear in against the yen, where it has been confined to a quarter of a yen range. Although the dollar has not pushed through JPY109, it has not traded below JPY108.50 since Europe’s close yesterday. |

FX Daily Rates, April 24 - Click to enlarge |

| In Europe, sterling held barely above the low it had seen in Asia (a brief dip below $1.3920), but the euro makes a marginal new low, almost $1.2180.

The euro is straddling the $1.22 area. There is a 1 bln euro option struck there that expires today. The ECB meets Thursday, and there is a 3.4 bln euro option that is also struck there that expires toward the end of Draghi’s subsequent press conference. The low since mid-January was set on March 1 near $1.2155. Initial resistance is now seen in the $1.2220-$1.2240. |

FX Performance, April 24 - Click to enlarge |

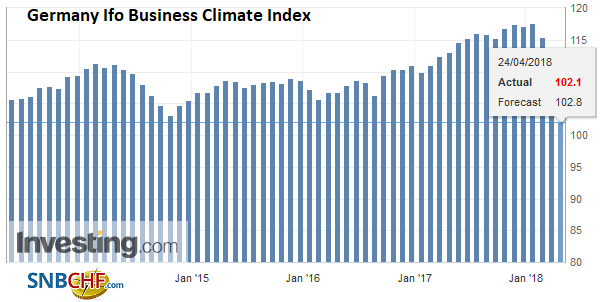

GermanyGermany reported a fifth consecutive decline in the IFO sentiment survey and the decline appears to be larger than expected. However, there were some methodological changes, which include a new base year, 2015, and reducing the weight of the manufacturing sector by half ( to 30%) and boosting the service sector. Without getting lost in the details, the takeaway is that the deterioration of investor sentiment seen in Q1 has spilled over to Q2. This is broadly consistent with yesterday’s PMI that reported a fourth consecutive month that manufacturing slowed. The service sector rose slightly, but the reading was still the second lowest since last August. |

Germany Ifo Business Climate Index, May 2013 - Apr 2018(see more posts on Germany IFO Business Climate Index, ) Source: Investing.com - Click to enlarge |

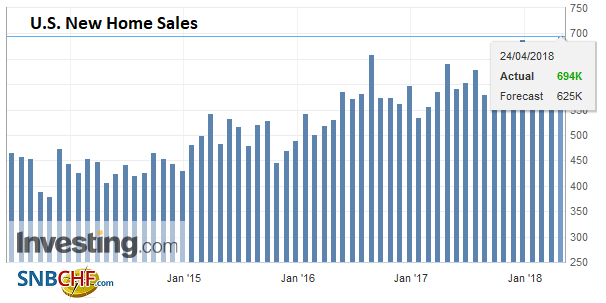

United StatesThe US session sees more housing data (prices and new home sales) and typically are not market-movers. Richmond Fed manufacturing survey for April and the Conference Board’s consumer confidence measure do not draw much attention. The Fed is in its quiet period ahead of the May 2 FOMC meeting. |

U.S. New Home Sales, May 2013 - Apr 2018(see more posts on U.S. New Home Sales, ) Source: Investing.com - Click to enlarge |

The UK reported its first current fiscal surplus (excluding capital investment), for 2001-2002, helped by the smaller than expected shortfall in March. Overall, the deficit fell from 9.9% of GDP in 2009 to 2.1% last year. The Office for Budget Responsibility to did not anticipate this milestone until this year. The holds local elections, and the government’s austerity is an issue in some areas. While the odds of a BOE hike next month were halved by the soft data and the seemingly cautious comments from Governor Carney last week, the probability, projecting from derivatives’ market has increased slightly over the last couple of sessions to stand near 55%.

Sterling needs to resurface above $1.3965 to improve the tone but the intraday technical indicators warn that this may be difficult sustain. There may be some intermittent support (e.g., 100-day moving average ~$1.3855), but nothing looks strong nearer $1.38.

News that the US softened its position toward Russia’s Rusal and gave US companies more time to unwind exposures spurred a dramatic 7% drop in Aluminum prices yesterday. Rusal shares gained more than a third in Hong Kong turnover. Most of the other producers in the sector fell. The ruble itself is about 0.25% firmer today and is outperformed by the South African rand and Turkish lira, both of which are up about 0.5%. Russia’s benchmark 10-year dollar bond yield is off eight basis points to 4.70%, while the ruble benchmark yield is five basis points lower at 7.23%.

Brent oil edged to a new high today of almost $75.30. WTI for June delivery is firm, but it has held below last week’s high ($69.55). The market is anticipating another drawdown of US inventories. There the May 12 deadline for the Iranian decision from the White House is beginning to become a market factor. One camp, which includes some of Trump’s new national security team, and internationally, by Saudi Arabia and Israel, advocate a hardline, while Europe (Macron and Merkel this week) want to add and build on the agreement to include a ban on missile tests.

Global equities are firmer, even without much leadership out of the US yesterday. The MSCI Asia Pacific Index snapped a two-day 1.6% drop. The soft yen may have boosted Japanese shares. The Topix added 1.1% to reach a two-month high. Ideas that China may relax some of the squeeze on credit helped lift mainland shares by around 2%. Europe’s Dow Jones Stoxx 600 is up for the second consecutive session and the fifth of the past six. Energy and information technology is leading the way, though telecom and consumer discretion, industrials, and financials are nursing losses. Note that the MSCI Emerging Market Index is underperforming and is extending its decline for a third session. However, the downside momentum has eased as the lower end of this year’s range is approached.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$EUR,$JPY,EUR/CHF,Featured,gbp-chf,Germany IFO Business Climate Index,newslettersent,SPY,U.S. New Home Sales,USD/CHF