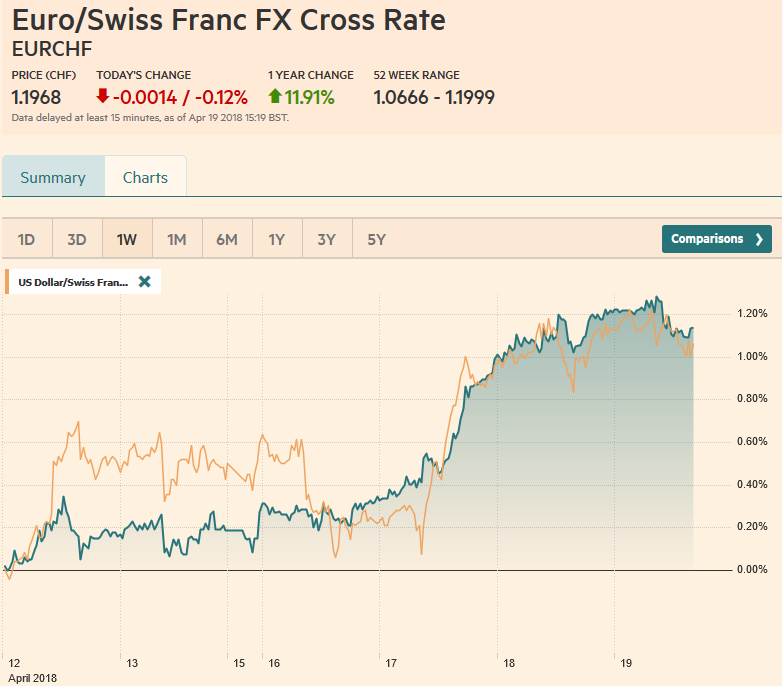

Swiss Franc The Euro has fallen by 0.11% to 1.1968 CHF. EUR/CHF and USD/CHF, April 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates A light news stream and less trade rhetoric lend the equity markets a positive impulse amid a strong US earnings season while leaving the dollar narrowly mixed. The MSCI Asia Pacific Index rose 0.5% and is up 1% for the week with one session left. It would be the second consecutive weekly advance. The Dow Jones Stoxx 600 has edged higher for a third consecutive session. It is up about 0.7% for the week, and if sustained, would extend the advance for a fourth consecutive session. The most interesting thing about the euro today, which

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CAD, EUR, EUR/CHF, Featured, GBP, JPY, newslettersent, NZD, U.K. Core Retail Sales, U.K. Retail Sales, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Swiss FrancThe Euro has fallen by 0.11% to 1.1968 CHF. |

EUR/CHF and USD/CHF, April 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesA light news stream and less trade rhetoric lend the equity markets a positive impulse amid a strong US earnings season while leaving the dollar narrowly mixed. The MSCI Asia Pacific Index rose 0.5% and is up 1% for the week with one session left. It would be the second consecutive weekly advance. The Dow Jones Stoxx 600 has edged higher for a third consecutive session. It is up about 0.7% for the week, and if sustained, would extend the advance for a fourth consecutive session. The most interesting thing about the euro today, which remains mired in a little more than a two-cent range since the end of January (~$1.22-$1.24) is the large number of options that expire today. There are over one billion euros of options struck at $1.23 and $1.24 today, and several smaller options. There are nearly 1.7 bln euros struck between $1.2310 and $1.2325. There are 760 mln euros struck at $1.2350 and 570 mln euros struck at $1.2385. |

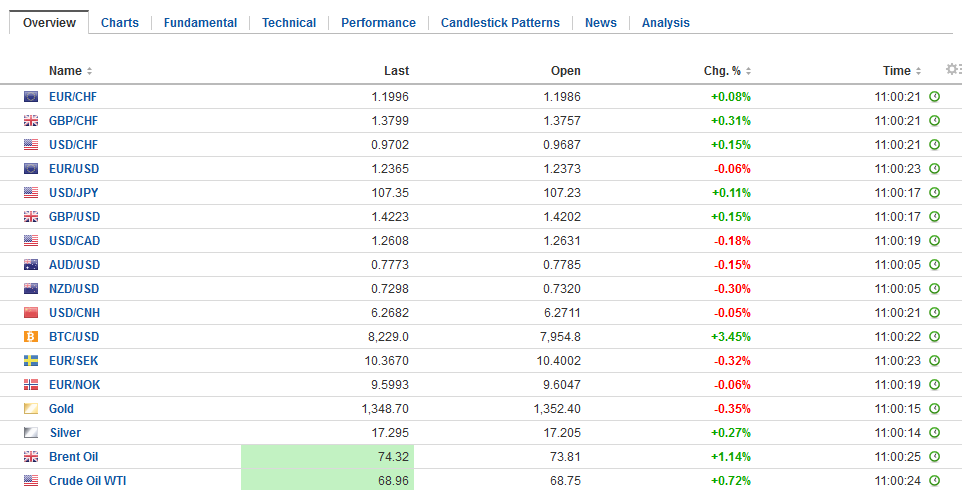

FX Daily Rates, April 19 - Click to enlarge |

| The dollar has entered the upper end of its two-month range against the yen. Resistance is seen in the JPY107.60-JPY107.80 band. A move above JPY108, which corresponds to a 38.2% retracement of the dollar’s losses since the January 8 high near JPY113.40, and has not happened since mid-February would lift the technical tone.

The US dollar rallied against the Canadian dollar in February and consolidated in March, forming a head and shoulders technical topping pattern, which projects toward CAD1.2475. The greenback made great strides toward the target, but momentum stalled last week, and our read of the technical indicators warned of a coming bounce. Even though the US dollar made new lows on Monday, the short-term market seemed vulnerable to some profit-taking. |

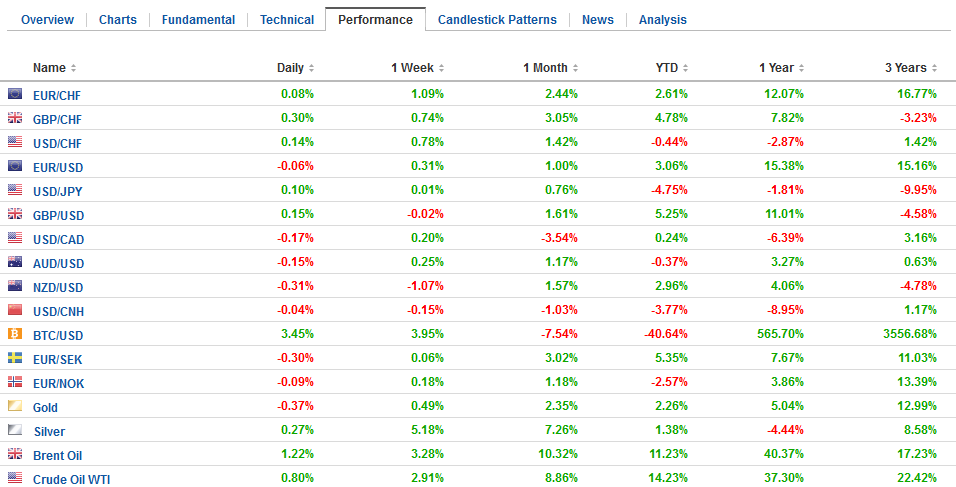

FX Performance, April 19 - Click to enlarge |

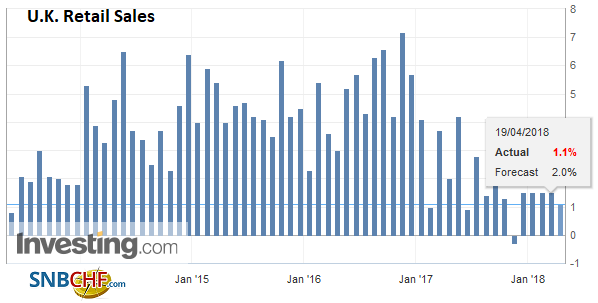

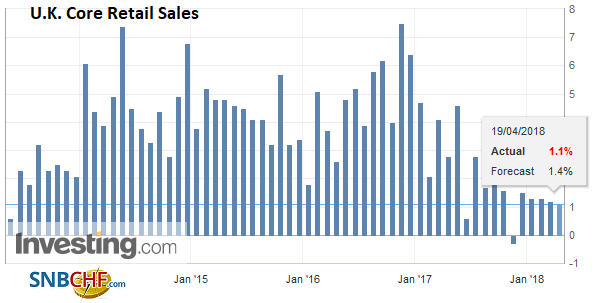

United KingdomSterling recorded its low near $1.4175 before the House of Lords voted. This corresponds to the 50% retracement objective of the leg up that began from the brief dip below $1.40 on April 5. The slightly larger than expected decline in retail sales in March (-0.5% vs. -0.4% expected, excluding gasoline) saw sterling slip further. The next retracement objective and 20-day moving average are found in the $1.4125-$1.4145 area. |

U.K. Retail Sales YoY, May 2013 - Apr 2018(see more posts on U.K. Retail Sales, ) Source: Investing.com - Click to enlarge |

U.K. Core Retail Sales YoY, May 2013 - Apr 2018(see more posts on U.K. Core Retail Sales, ) Source: Investing.com - Click to enlarge |

The Bank of Canada held policy steady yesterday, and although the Canadian dollar sold off, the statement was dovish. A rate hike in Q3 still seems to be the most likely scenario, and by then, some of the uncertainty about NAFTA will likely be lifted. The overnight rate at 1.25% is half of the lower bound of what the BOC has identified as neutral policy (2.5%-3.5%).

Growth potential was lifted to 1.8% this year and next from 1.6% estimated in January. It did slash Q1 18 growth forecast to 1.3% from its earlier 2.5% projection. However, for the year as a whole, the GDP was shaved only 0.2% to 2%, while 2019 growth forecast was lifted to 2.1% from 1.6%. The Bank of Canada is saying look past Q1 softness, and as demand has picked up, investment has expanded capacity.

Our target was the CAD1.2640 area. After the Bank of Canada, the dollar reached CAD1.2660 was reached but closed back below our target. A move below CAD1.2580 would suggest the greenback’s slide push toward CAD1.2475 is resuming.

Sterling was sold more in response to the slightly softer than expected inflation data than in response to the government’s loss in the House of Lords. As sterling reached its best level since the referendum this week, so was the vote the strongest pushback by the pro-EU camp. They defeated the government twice.

First, it succeeded in attaching an amendment to the Withdrawal Bill requiring remaining in the customs union, something Prime Minister May has explicitly ruled out. Second, the House of Lords passed a bill to prevent the government from changing the regulations governing employment, consumers, and the environment without parliament’s consent. While the House of Commons can and most likely will swat away House of Lords’ initiatives, it gives a sense of what lies ahead as Brexit requires votes on at least three other crucial bills (trade, customs, implementation).

The euro has staged an important reversal against sterling at the end of last week, but there was no follow-through, though the technicals seemed to favor it. Patience was rewarded yesterday. The euro bounced 0.6%, the most since the late February. From a low near GBP0.8620 the day before, the euro reached GBP0.8720 yesterday, which is where the 61.8% retracement of the drop since the peak on March 1 and the 20-day moving average. Nearby resistance is seen near GBP0.8750.

New Zealand’s CPI slowed to 1.1% in Q1 from 1.6% in Q4 17 on a year-over-year basis. This was in line with expectations but reinforced the conviction that monetary policy is on hold. Australia’s employment report disappointed, with a loss of full-time positions (-19.9k), a decline in the participation rate (65.5% from 65.6%, the second consecutive decline), and meaningful downward revisions to the February series.

The Australian dollar’s advance has stalled near $0.7800, but short-term market participants have not given up on it. A move above $0.7820 would be a convincing break and would suggest a move toward $0.7900. The New Zealand dollar has been underperforming, and a break of the $0.7290 area could spur losses toward $0.7200 before strong chart support is encountered.

The Fed’s Beige Book seemed to mostly confirm what the market already knows. The economy is expanding at a moderate pace, and many are optimistic about the near-term outlook Trade issues have become more salient. Tariffs are already lifting the price of steel. More broadly, the price of building materials (lumber, drywall, concrete) is rising. The labor market is tightening, and while some employers are increasing pay, others are boosting training and looking for places to automate, which are non-inflationary strategies.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,Featured,newslettersent,NZD,U.K. Core Retail Sales,U.K. Retail Sales,USD/CHF