Summary: For the US jobs data to rally the dollar, it needs to increase the likelihood of a Fed hike in September, a high bar. The BOE will stand pat, a 6-2 vote would likely be accompanied by a hawkish inflation report. The RBA will also hold rates steady, and of course, it would prefer a weaker currency. The tide of sentiment has turned against the dollar. The enthusiasm seen in the second part of last year, when the real broad trade weighted dollar rose in seven of the last eight months have been put into reverse. This measure of the dollar is set to record its seventh consecutive monthly decline this year, among the longest such runs in the modern era. The tide against the dollar is both political and

Topics:

Marc Chandler considers the following as important: AUD, CAD, EUR, Featured, FX Trends, GBP, JPY, newslettersent, South Korea, TLT, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Summary:

For the US jobs data to rally the dollar, it needs to increase the likelihood of a Fed hike in September, a high bar.

The BOE will stand pat, a 6-2 vote would likely be accompanied by a hawkish inflation report.

The RBA will also hold rates steady, and of course, it would prefer a weaker currency.

The tide of sentiment has turned against the dollar. The enthusiasm seen in the second part of last year, when the real broad trade weighted dollar rose in seven of the last eight months have been put into reverse. This measure of the dollar is set to record its seventh consecutive monthly decline this year, among the longest such runs in the modern era.

The tide against the dollar is both political and economic. At the start of this year, many feared the populist-nationalist wave which was seen as on its way to Europe after sweeping the UK out of the EU and Trump into the White House. As we anticipated, Europe has turned back the populist threat at every opportunity. The political anxiety has been deflected back to the US, where distractions, inexperience, and/or incompetence have frustrated the legislative process despite one party enjoying a majority in both houses of the legislative branch and control of the executive branch. Also, with a UK snap election, after repeated denials, and an unexpected outcome, UK politics is anything but settled, as the Brexit countdown continues.

Leaving aside the filibuster rules that require 60 votes to proceed, the Republicans failed to marshall a simple majority to repeal and replace the national health care system, despite several years of critiquing it. The health care reform was initially also intended to help fund tax reform. Nearly $1 trillion was expected to have been saved. Last week saw the House leadership finally drop its insistence of a Border Adjustment Tax (BAT). The controversial tax was supposed to free up another trillion dollars to fund tax reform. With those two pieces gone, the prospect of tax reform diminishes.

Tax cuts are still possible, but if by CBO’s reckoning that the tax cuts will increase the debt level in a decade, then a 60-vote majority is needed. The Bush Administration’s work around was to make the tax cuts temporary. When those tax cuts expired, the country contended with a “fiscal cliff” and what felt like tax increases.

Still, it is not clear that the current leadership can bridge the chasm between its conservative and moderate-wings to agree to cut taxes. The basis for an agreement would likely mean that the tax cuts are fiscally neutral, which in turn could limit the stimulative impact. Moreover, without tax reform, the tax holiday to encourage repatriation of earnings held offshore would simply keep the cycle going, whereby mostly the same industries accumulate earnings offshore and wait for the inevitable break. By seeking to tax some of those earnings, Ireland has added pressure to reform the US approach to corporate taxes.

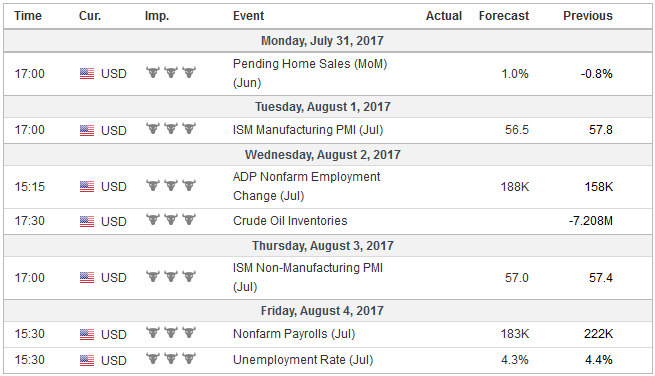

United StatesThis leaves the US economy expanding around trend (~1.8%). The labor market continues to improve as the job creation has accelerated after a slow start to the year. Productivity growth is weak, and apparently without an immediate solution, and labor costs increases are also subdued. This was underscored by the disappointing 0.5% increase in the Q2 Employment Cost Index, released before the weekend. The expected 0.3% rise in average hourly earnings will not be sufficient to avoid the year-over-year pace slipping back to 2.4%, the lower end of a two-year range. The last time it was weaker was in September 2015. Barring a significant upside surprise, the jobs report is unlikely to increase the risk of a September hike by the Fed or spur sharp backing up of long-term rates. Given the poor sentiment and interest rate backdrop, the dollar may struggle to sustain more than shallow bounces. |

Economic Events: United States, Week July 31 - Click to enlarge |

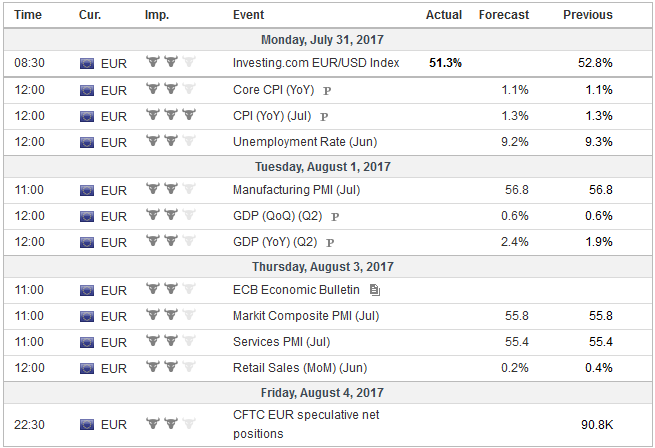

EurozoneSimilarly, news from the eurozone is unlikely to dampen expectations that the ECB will announce in September plans to scale back its asset purchases starting next year. Many investors have concluded that the ECB expanding its balance sheet around 180 bln euros in H1 18 (vs. 360 bln euros in H2 17) is somehow more supportive of the currency than the Fed likely shrinking its balance sheet $150 in H1 18. It does bring forward the day that the ECB may begin raising rates, but remember, it is beginning with its deposit rate at minus 40 bp. If it is hiked to minus 20 bp in H2 18, is that really a tightening? And isn’t it reasonable to expect the Fed to hike before this happens? This week’s eurozone data include PMI (Spain and Italy are the focus since the flash), Q2 GDP (0.6%-0.7%, after 0.6% in Q1), unemployment (tick down to 9.2%, more than twice the US rate). At the start of the week, investors will see the first estimate of July CPI. Both the headline and core rates are unexpected to be unchanged at 1.3% and 1.1% respectively. Even a slightly disappointing inflation report is unlikely to impact expectations for ECB tapering. |

Economic Events: Eurozone, Week July 31 - Click to enlarge |

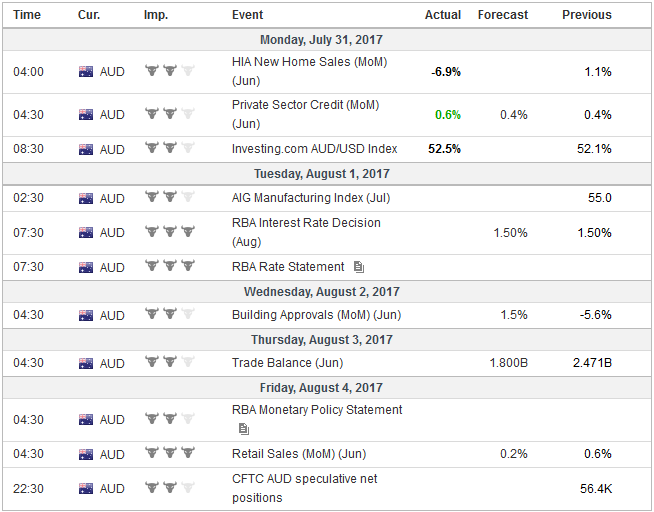

AustraliaTwo central banks hold policy making meeting, the Reserve Bank of Australia and the Bank of England. The RBA is expressing no sense of urgency to change the cash rate from 1.5%. Governor Lowe recently noted that a weaker currency would be more helpful, but this is a low-level protest and one the market’s duly shrugged-off. Speculators have been drawn to the Aussie, which for the sixteen sessions beginning July 7, has only declined four times. |

Economic Events: Australia, Week July 31 - Click to enlarge |

United KingdomThe Bank of England also most likely will stand pat. The vote may attract interest. One of the three dissenters at the last meeting (Forbes) term end and her replacement (Tenreyro) is widely expected to vote with the majority. However, there is some risk that Haldane votes with the hawks, which would leave the vote 5-3. Paradoxically, if Haldane does not vote for a hike, the quid pro quo may be a more hawkish quarterly inflation report, that is released at the same time as the MPC meeting concludes and the minutes are released. Ahead of the BOE meeting, the July PMIs for construction, manufacturing, and service will be reported. Forward looking new orders and business expectations have softened, this batch of PMIs will likely suggest that the UK economy is gradually slowing, and the Bank of England is must recognize this in word and in their forecasts. After a slow H1 (Q1 02% and Q2 0.3% vs. 0.2% and 0.6% in Q1 16 and Q4 16), the economy is not expected to accelerate in H2. We suspect that the peak in UK inflation is within a month or two. The base effect of sterling’s sharp drop is eliminated from the year-over-year comparison, the pullback in energy prices, and softer consumption as the squeeze on real wages bite. The contest is between these forces and the patience of a majority of the MPC. |

Economic Events: United Kingdom, Week July 31 - Click to enlarge |

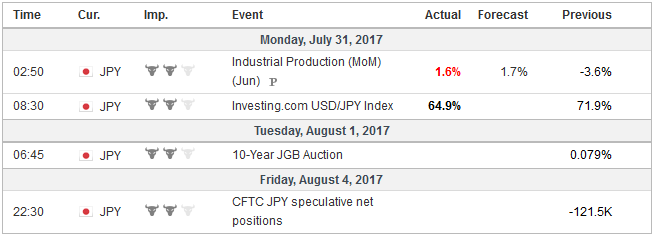

JapanThe main interest in Japan does not lay with its economic data, but with politics. First, the LDP, with a comfortable majority is an increasingly facing disenchanted citizenry. It lost the Tokyo election resoundingly, and the Abe government and the Prime Minister himself have been accused of abuse of power and favoritism. The allegations and scandals led to the Defense Minister’s resignation at the end of last week. This is a prelude of a large cabinet reshuffle in the coming days. Domestic problems in Japan are not as bearish for the yen as may be intuitively assumed. Japan’s large net international investment position provides the wherewithal to repatriate savings back home. Also, to address his low level of support, Abe would not be the first politician to offer a shot of fiscal stimulus. A second political issue emerged before the weekend. Due to a surge of imports of frozen beef, Japan announced, in apparent compliance with the WTO, have levied a surcharge on top of its customary tariff. Currently, US exports of frozen beef to Japan have a 38.5% tariff assigned. Under emergency rules, the tariff rises to 50%. The surcharge will remain in place through March and can be automatically imposed if imports surge by more than 17% year-over-year in any quarter. But wait, the plot thickens. |

Economic Events: Japan, Week July 31 - Click to enlarge |

CanadaLastly, we turn to Canada, where the positive news stream has sent the Canadian dollar to levels not seen in a couple of years (above $0.80). The surge in May’s GDP (0.6% for a 4.6% year-over-year pace) reinforces ideas that the Bank of Canada will take back the other cut that it provided for support in 2015, having taken the first back earlier this month. Canada reports June trade balance and July employment at the end of next week. Employment surged in June, and a more subdued pace is expected (~10k). Growth differentials and the terms of trade warn of downside risks of Canada’s trade balance. Widening of trade deficit may not be negative for the Canadian dollar because it would increase the likelihood of a hike in Q4 (October?). Extrapolating for the OIS, there appears to be a little more than a 50% chance of a hike discounted. Since the day before the July 12 rate hike, the December the implied yield of the December BA futures have risen by 14 bp to 1.51%, which is where it finished last week. |

Economic Events: Canada, Week July 31 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week July 31 - Click to enlarge |

The US and Australia account for 9/10 of the Japanese market for imported frozen beef. Japan has a free-trade agreement with Australia, which is exempt from the surcharge. Its normal tariff is 27.5% and is to be reduced in stages, according to the agreement. Japan accounts for about a quarter of the international market for US frozen been exports. US cattle futures sold off when the news was initially announced.

The Trans-Pacific Partnership agreement would have addressed these issues. This may be one of the first tangible results of pulling out of the late-stage negotiations. Still, it is surprising that Abe did not intercede. The strategy that officials had intimated was to seek to avoid antagonizing an unknown, volatile, if not vitriolic partner. This goes does the opposite, and before Finance Minister Aso and Vice President Pence hold bilateral trade talks later this year. On the other hand, if the roughly $400 mln export issue dominates the agenda, then more substantive issues might not be discussed and thus strengthening the inertia that defends the status quo.

North Korea tested another intercontinental ballistic missile over the weekend. Some reports suggest that this second test this month suggests the capability to hit the midwest of the US, though there seems to be some disagreement. The US appears to have responded by testing its missile defense system in Alaska and flew to supersonic bombers over South Korea. Tensions remain high, but investors do not appear alarmed. The Korean won is the strongest currency in Asia this month, appreciating nearly 2% against the US dollar. Korean shares have underperformed, with the Kospi up about 0.4% in July while the MSCI Asia Pacific Index has rallied about 3.3% and a nearly 5. 2% gain in the MSCI Emerging Market equity index this month.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,$TLT,Featured,newslettersent,South Korea