Economic, social and human cost Beyond privacy, there is also widespread concern over the economic impact of a fully cashless system. For one thing, as citizens slowly become exclusively dependent on big banks and card companies the systemic risk to the wider economy spikes. But it goes further than that too. Without the option to keep some cash outside the banking system and retain some degree of financial flexibility, banks have the potential to essentially keep their clients hostage. Bail-in scenarios and deposit “haircuts”, allowing distressed banks to directly take funds from their clients’ accounts, a scenario we saw in Cyprus in 2013, are instantly simplified. Good old-fashioned bank runs are all but eliminated as leverage, while policies like NIRP and ZIRP face significantly

Topics:

Claudio Grass considers the following as important: capital exchange control, Economics, Finance, Gold, Greece, India, Monetary, Politics, printed freedom, private property rights, Uncategorized, War on cash

This could be interesting, too:

Investec writes The Swiss houses that must be demolished

Claudio Grass writes The Case Against Fordism

Claudio Grass writes “Does The West Have Any Hope? What Can We All Do?”

Investec writes Swiss milk producers demand 1 franc a litre

Economic, social and human cost

Beyond privacy, there is also widespread concern over the economic impact of a fully cashless system. For one thing, as citizens slowly become exclusively dependent on big banks and card companies the systemic risk to the wider economy spikes. But it goes further than that too. Without the option to keep some cash outside the banking system and retain some degree of financial flexibility, banks have the potential to essentially keep their clients hostage. Bail-in scenarios and deposit “haircuts”, allowing distressed banks to directly take funds from their clients’ accounts, a scenario we saw in Cyprus in 2013, are instantly simplified. Good old-fashioned bank runs are all but eliminated as leverage, while policies like NIRP and ZIRP face significantly lower obstacles, as without the option to take cash out of the system, the banks can easily pass down the associated costs to the clients.

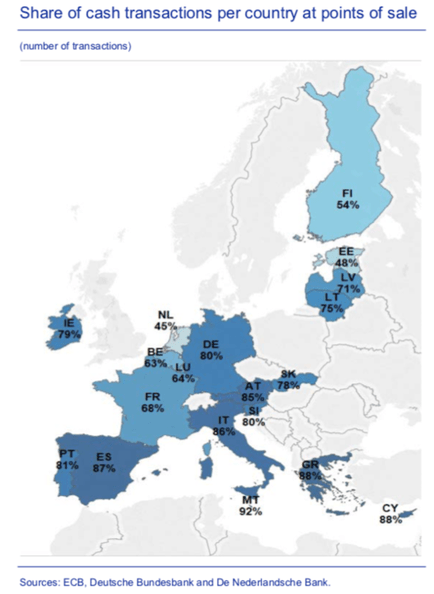

Capital controls also become much easier to comprehensively enforce, while their impact is multiplied. These measures were already proven catastrophic in Greece, where citizens had to live for over 3 years with an ATM withdrawal limit of EUR60 a day and draconian restrictions on payments abroad. Businesses were put under immense pressure, unable to pay their international suppliers without special permission, while elderly citizens formed endless lines in front of ATMs to receive their pensions in the allowed increments and many struggled to pay for their daily needs. And yet, disastrous as the policy was for the public, their predicament would have been infinitely more severe if Greece did not have a solid cash-loving tradition. The small Mediterranean nation holds the second place (tied with Cyprus) among EU members with the highest share of cash transactions, while due to the country’s history, citizens are inclined to keep significant amounts or parts of their savings stored at home, something that helped soften the impact of the capital control measures.

Capital controls also become much easier to comprehensively enforce, while their impact is multiplied. These measures were already proven catastrophic in Greece, where citizens had to live for over 3 years with an ATM withdrawal limit of EUR60 a day and draconian restrictions on payments abroad. Businesses were put under immense pressure, unable to pay their international suppliers without special permission, while elderly citizens formed endless lines in front of ATMs to receive their pensions in the allowed increments and many struggled to pay for their daily needs. And yet, disastrous as the policy was for the public, their predicament would have been infinitely more severe if Greece did not have a solid cash-loving tradition. The small Mediterranean nation holds the second place (tied with Cyprus) among EU members with the highest share of cash transactions, while due to the country’s history, citizens are inclined to keep significant amounts or parts of their savings stored at home, something that helped soften the impact of the capital control measures.

Furthermore, there is another important risk as the war on cash escalates, affecting significant parts of the population, namely the threat of financial exclusion. In most Nordic countries, among the first and most eager to adopt the move from cash to electronic money, pensioners have seriously struggled with the shift, as they do not use the internet or have access to online banking. In Norway, the conversion to cashless bank branches has left many towns without a single bank, the Swedish National Pensioners Organization has stressed that 1 million people in the country are not ready for cashless transactions, while Denmark’s DaneAge Association, representing more than 750,000 senior citizens, has strongly criticized the limits on cash-based payments. Apart from the elderly, those at the lower end of the socio-economic pyramid are also victimized by these policies. The war on cash effectively ensures that those without access to baking services, those living in poverty and the homeless population is banned from participating in the economy and by extension socially marginalized even more.

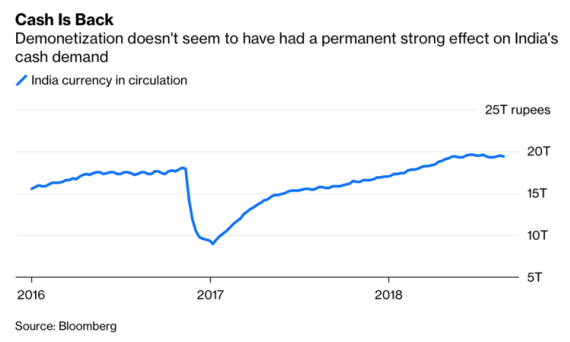

Once again, let us underline the practical and realistic nature of this threat, by recalling another real-life example, this time from India. Following the Indian government’s decision in 2016 to withdraw the very widely used 500- and 1000-rupee notes from circulation, a policy that we know now has spectacularly failed in its objectives, the disastrous implementation of the law saw chaos reign all over the country and the economy in disarray. Business operations were disrupted, employees went unpaid and even everyday transactions, as simple as grocery shopping, became a formidable challenge. During this mayhem, tens of millions of Indians, having no access to banking services and most of them from the lowest economic strata, found themselves without the means to pay for their basic needs. As their money wasn’t accepted anymore, they were deprived of bare necessities, including food, essential medicine and medical services. The situation was so dire, that dozens of people died. This even included children and infants that were refused treatment in hospitals, as the staff would not accept their families’ banknotes as payment.

The way forward

Given the aggressive and persistent steps that governments, institutions and banks have taken so far to annihilate cash, it is reasonable to expect the pressure to keep building up. However, while the fate of physical banknotes might be already sealed, it definitely doesn’t mean that investors, savers and everyday citizens have no moves left.

The technological progress that has allowed this shift away from individual financial sovereignty to take place to begin with is now providing ways to reclaim it. The rise of cryptocurrencies and of decentralized systems that protect their users’ privacy and eliminate the need for a central authority have already shown great promise. And while their disruptive potential might indeed be considerable, their real strength arguably lies in the fact that they provide more choices to consumers, adding options, instead of limiting them and allowing free, voluntary engagement with different ideas and concepts, instead of forcing people to use a single system.

While new technologies might one day prove valuable tools to resist centralization and to keep transactions outside the banking system, when it comes to saving and storing value, the solution has always been there. As cash and the relative autonomy that came with it quickly fades, the role of precious metals becomes more important than ever. Physical gold and silver, stored outside the banking system and in a stable jurisdiction, such as Switzerland, is an essential step towards limiting one’s exposure to these risks, preserving wealth and safeguarding one’s autonomy and financial independence. Combined with the potential of new blockchain-based technologies and the capacity for the digitalization of real assets, gold can even be used in a decentralized trading platform, where it can be traded outside the banking system, offering the capacity to overcome controlling governmental pressures and reclaim privacy rights.

Claudio Grass, Hünenberg See, Switzerland

Bildrechte: © v.poth / Foltolia