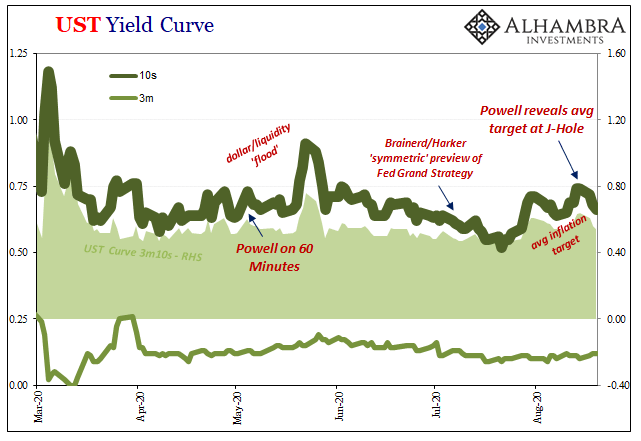

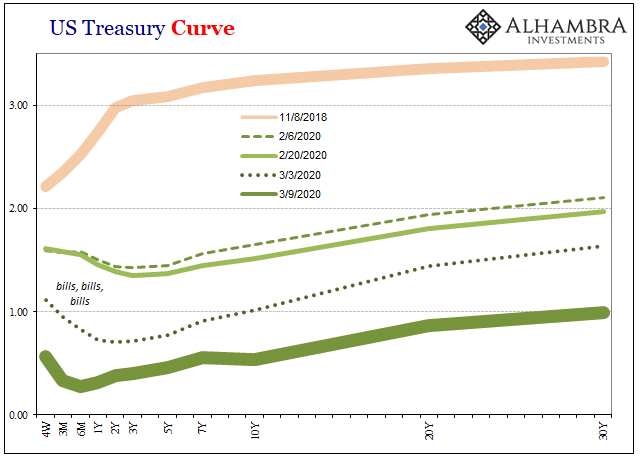

Since the unnecessary destruction brought about by GFC2 in March 2020, there have been two detectable, short run trendline upward moves in nominal Treasury yields. Both were predictably classified across the entire financial media as the guaranteed first steps toward the “inevitable” BOND ROUT!!!! Each has been characterized as the handywork of master monetary tactician Jay Powell. There is some truth underlying, only stripped of all that hyperbole. These backups in yields over the last few months do coincide with major Federal Reserve initiatives (if you can call them that). The first one was the “flood”, a couple weeks punctuated by Chairman Powell’s wild appearance on 60 Minutes. Тhe 10-year yield “surged” upward, reaching at one point above 90 bps. The next

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, average inflation target, bond yields, bonds, currencies, economy, Featured, Federal Reserve/Monetary Policy, flood, inflation, interest rate swap, Interest rates, jay powell, Liquidity, Markets, money printing, newsletter, swap spreads, symmetric inflation target, U.S. Treasuries, Yield Curve

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Since the unnecessary destruction brought about by GFC2 in March 2020, there have been two detectable, short run trendline upward moves in nominal Treasury yields. Both were predictably classified across the entire financial media as the guaranteed first steps toward the “inevitable” BOND ROUT!!!! Each has been characterized as the handywork of master monetary tactician Jay Powell.

There is some truth underlying, only stripped of all that hyperbole. These backups in yields over the last few months do coincide with major Federal Reserve initiatives (if you can call them that). The first one was the “flood”, a couple weeks punctuated by Chairman Powell’s wild appearance on 60 Minutes. Тhe 10-year yield “surged” upward, reaching at one point above 90 bps. The next retrace in Treasuries began in early August. Two weeks beforehand a couple of FOMC members had tipped their hand as to what the results of the central bank’s GRAND STRATEGY reassessment was going to look like. Governor Brainerd and Philly President Harker both made a really big deal out of “symmetry” in mid-July – as if the entire FOMC hadn’t made a big deal out of “symmetry” two years and two months before then. To this point in early September, the rising trend in yields, as markets digested this symmetrical inflation target becoming an average one (with every participant in them scratching their heads trying to figure out why central bankers seem to believe everyone will believe these are somehow different), fittingly seems to have ended right when Jay Powell appeared (virtually) at Jackson Hole and unveiled this “new” masterpiece. |

UST Yield Curve, 2020 - Click to enlarge |

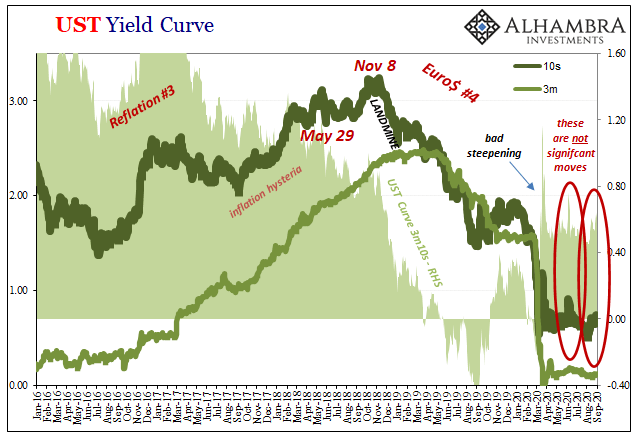

| Of course, neither of those actually qualifies as anything but the smallest little blip. In the big picture, longer run context I’m not even sure they qualify as a blip.

So, the Fed makes a huge deal, full publicity blitz, twice, out of its rush toward monetary recklessness which barely, ever-so-slightly registered in the bond markets (including, as you can see, rate swap markets). If I was Jay Powell, I’d ask for my money back from both CBS as well as whomever fleeced the FOMC for the strategy review. Then again, the Federal Reserve doesn’t do money, so the joke’s on Jay. |

. |

| The problem, therefore, and what bond yields are all about, quite simply, is how we are the ones who always have to pay for it. |

UST Yield Curve, 2016-2020 - Click to enlarge |

UST Yield Curve, 2003-2020 - Click to enlarge |

|

Swap Spreads, 2016-2020 - Click to enlarge |

|

. |

You Might Also Like

So Much Bond Bull

So Much Bond Bull

Count me among the bond vigilantes. On the issue of supply I yield (pun intended) to no one. The US government is the brokest entity humanity has ever conceived – and that was before March 2020. There will be a time, if nothing is done, where this will matter a great deal.That time isn’t today nor is it tomorrow or anytime soon because it’s the demand side which is so confusing and misdirected.

No Flight To Recognize Shortage

No Flight To Recognize Shortage

If there’s been one small measure of progress, and a needed one, it has been the mainstream finally pushing commentary into the right category. Back in ’08, during the worst of GFC1 you’d hear it all described as “flight to safety.” That, however, didn’t correctly connote the real nature of what was behind the global economy’s dramatic wreckage. Flight to safety, whether Treasuries or dollars, wasn’t it.

Transitory, The Other Way

Transitory, The Other Way

After a record three straight months of decline for the seasonally-adjusted core CPI March through May 2020, it turned upward again in June. Buoyed by a partially reopened economy, the price discounting (prerequisite to the Big D) took at least one month off.

This Has To Be A Joke, Because If It’s Not…

This Has To Be A Joke, Because If It’s Not…

After thinking about it all day, I’m still not quite sure this isn’t a joke; a high-brow commitment of utterly brilliant performance art, the kind of Four-D masterpiece of hilarious deception that Andy Kaufman would’ve gone nuts over. I mean, it has to be, right?I’m talking, of course, about Jackson Hole and Jay Powell’s reportedly genius masterstroke.

Three Short Run Factors Don’t Make A Long Run Difference

Three Short Run Factors Don’t Make A Long Run Difference

There are three things the markets have going for them right now, and none of them have anything to do with the Federal Reserve. More and more conditions resemble the early thirties in that respect, meaning no respect for monetary powers. This isn’t to say we are repeating the Great Depression, only that the paths available to the system to use in order to climb out of this mess have similarly narrowed.

From QE to Eternity: The Backdoor Yield Caps

From QE to Eternity: The Backdoor Yield Caps

So, you’re convinced that low rates are powerful stimulus. You believe, like any good standing Economist, that reduced interest costs can only lead to more credit across-the-board. That with more credit will emerge more economic activity and, better, activity of the inflationary variety. A recovery, in other words. Ceteris paribus. What happens, however, if you also believe you’ve been responsible for bringing rates down all across the curve…and then no recovery.

Wait A Minute, What’s This Inversion?

Wait A Minute, What’s This Inversion?

Back in the middle of 2018, this kind of thing was at least straight forward and intuitive. If there was any confusion, it wasn’t related to the mechanics, rather most people just couldn’t handle the possibility this was real. Jay Powell said inflation, rate hikes, and accelerating growth. Absolutely hawkish across-the-board.And yet, all the way back in the middle of June 2018 the eurodollar curve started to say, hold on a minute.

Part 2 of June TIC: The Dollar Why

Part 2 of June TIC: The Dollar Why

Before getting into the why of the dollar’s stubbornly high exchange value in the face of so much “money printing”, we need to first go back and undertake a decent enough review of the guts maybe even the central focus of the global (euro)dollar system.

Tags: average inflation target,bond yields,Bonds,currencies,economy,Featured,Federal Reserve/Monetary Policy,flood,inflation,interest rate swap,Interest rates,jay powell,Liquidity,Markets,money printing,newsletter,swap spreads,symmetric inflation target,U.S. Treasuries,Yield Curve