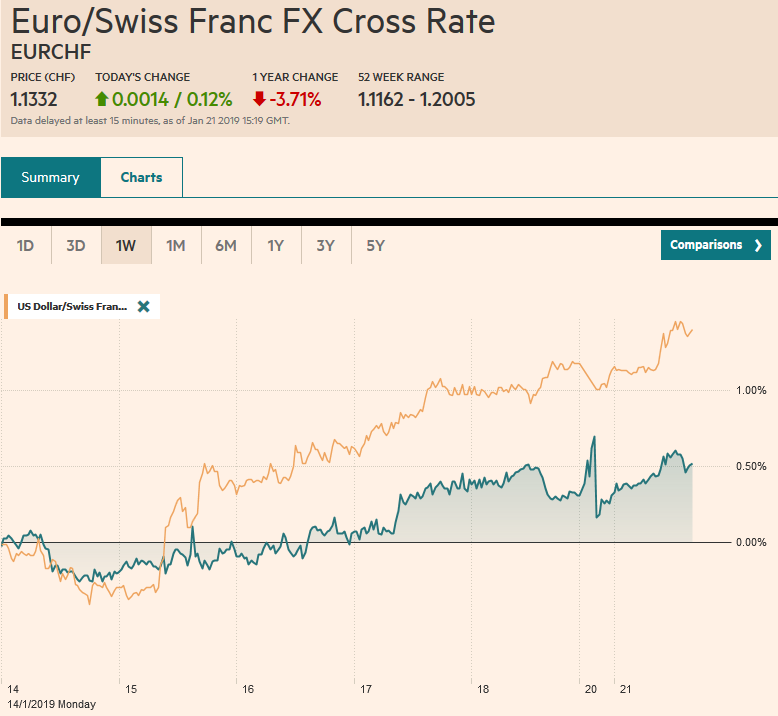

Swiss Franc The Euro has risen by 0.12% at 1.1332 EUR/CHF and USD/CHF, January 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Mixed data from China and the anticipation of Prime Minister May’s “Plan B” are the main talking points, while US stock and bond markets are closed today. Asia Pacific equities were higher, while European markets have failed to follow suit. Benchmark 10-year bond yields are mostly softer, with the on-the-run Japanese Government Bond yield dipping back into negative territory. The US dollar is narrowly mixed, gaining a little against the dollar-bloc currencies and sterling while slipping against the euro, yen, and Scandis. Most

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CAD, EUR, Featured, GBP, JPY, MXN, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.12% at 1.1332 |

EUR/CHF and USD/CHF, January 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Mixed data from China and the anticipation of Prime Minister May’s “Plan B” are the main talking points, while US stock and bond markets are closed today. Asia Pacific equities were higher, while European markets have failed to follow suit. Benchmark 10-year bond yields are mostly softer, with the on-the-run Japanese Government Bond yield dipping back into negative territory. The US dollar is narrowly mixed, gaining a little against the dollar-bloc currencies and sterling while slipping against the euro, yen, and Scandis. Most emerging market currencies are trading heavier, but the euro is helping the central and eastern European currencies steady. Oil prices edged higher initially but have reversed to trade marginally lower. |

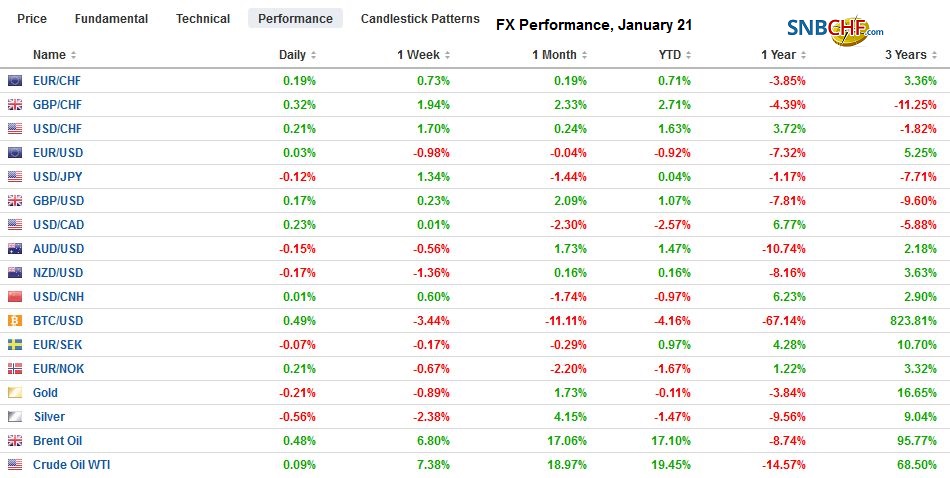

FX Performance, January 21 - Click to enlarge |

Asia Pacific

The uptick in China’s December retail sales and industrial output seems to offset the slightly disappointing Q4 GDP figures. Retail sales rose 8.2% year-over-year, up from 8.1%. Economists had forecast an unchanged report. Industrial output rose 5.7% year-over-year in December. The Bloomberg survey showed a median forecast for a 5.3% pace after 5.4% in November. Fixed asset investment was unchanged at 5.9%. Economists had anticipated a small increase. Fourth quarter GDP slowed to 6.4% from 6.5%, the slowest pace since 2009. The main idea is that, to the extent that one is willing to take the data at face value, the gains in retail sales and industrial production suggests that growth is finding a bottom and that the various efforts to stimulate the economy may have begun working.

Last week, press reports played up the debate within the Trump Administration over tactics ahead of China’s Vice Premier’s visit next week to Washington. The idea that Treasury was in some way sympathetic to easing tariff pressure on China was quickly and now repeatedly denied. Today’s reports suggest, as we suspected, there has been little progress in what is a key issue for the Trump Administration and that is intellectual property rights, not tariff barriers to trade per se. Separately, but related, the Administration is reportedly drafting measures that would impose restrictions on state-owned Chinese electronic firms operating in the US. It does not mention Huawei or ZTE by name.

The dollar is consolidating in a narrow range near the best levels seen before the weekend. It has been confined to about a quarter of a yen range above JPY109.50, The five-day moving average has crossed above the 20-day moving average for the first time since December 18, reflecting the recovery from the flash crash low that saw it break below JPY105 briefly. The BOJ meets in the middle of the week. It is not expected to take fresh initiatives. Despite the gradual reduction in its bond purchases (tapering by another name?), and the widening of the band last year under the Yield Curve Control policy to 20 bp, the yield, after some initial volatility, has been straddling zero. The Australian dollar is holding above last week’s low just below $0.7150. The upside momentum faded a little above $0.7200. A break of $0.7100 is needed to confirm a top.

Europe

UK Prime Minister May is to present Plan B to the House of Commons later today. The leaks in the media suggest it is Plan A with changes in the backstop provision, which EC has indicated it is not willing to negotiate further. May continues to rule out alternatives, including a postponement of the actual exit date, a second referendum, and remaining in a customs union. Some reports suggest that she wants to re-open the Good Friday Agreement that made for peace between Northern Ireland and the Republic. The House of Commons is to vote on Plan B next week. It is not just officials that are terribly divided on what to do next, but so are the people. According to a recent ICM poll (January 16-18), the most popular choice with 28% support was no-deal exit and on WTO terms. In second place with 24% was to start the process toward a second referendum. A general election was favored by 11%, while 8% wanted to press ahead with May’s plan.

Before the weekend, the Bank of Italy cut is GDP forecasts to 0.6% and 0.9% from 1.0% and 1.1% for this year and next respectively. It is a disappointing way to start the New Year but is probably prudent given that it also warned that the economy may have contracted in Q4, which if so, would meet the rule of thumb definition of a recession. There will be a knock-on effect on the deficit through a smaller denominator in the deficit/GDP calculations and also from the losses of revenue and increased expenditures that result from slower growth. There are some countervailing measures too, that automatically kick-in if the budget deficit goal is not reached like the VAT. After protracted negotiations with the EC, Italy’s budget deficit was projected at 2.04% of GDP this year. It is early to look for a revised budget, but this is likely the direction the situation will move.

The euro ran into sellers near $1.1400. There is a 1.2 bln euro option struck there that will be cut later today. There is another option for almost 860 mln euros at $1.1435 that will also roll-off today. Last week’s low, set ahead of the weekend was a little above $1.1350. That range will likely confine the euro into tomorrow’s activity as well. Our call this week is for the euro to bottom later in the week with the ECB meeting and then as attention turns to next week’s FOMC meeting and US jobs data, for the euro to recovery from the lower end of its range. Sterling reached $1.30 last week, a two-month high. That looks like an important high. The risk of more drama that ultimately appears to be going nowhere quickly keeps officials preparing for a no-deal exit. Initial support now for sterling is seen in a $1.2800-$1.2825 band.

North America

The US stock and bond markets are closed today, while the partial government shutdown enters Day 31. Some see a window of opportunity to resolve the dispute, but officials may still be a week away from realizing it. The shutdown is not just disrupting employees who are going without pay, but also the important activities of the government and interfering with the President’s agenda and cutting into his support, according to opinion polls.

Mexico President AMLO seems even more determined to press ahead with his efforts to end the fuel theft following an explosion at an illegal tap that killed at least 85 people and injuring more. The theft is estimated to be worth as much as $3.5 bln a year in more than three dozen illegal taps a day. Meanwhile, fuel shortages are plaguing Mexico City.

Before the weekend, Canada reported firmer than expected headline inflation, lifted by airfares. The core rates were steady. Services prices are firm (3.5% year-over-year, the highest since 2008), and excluding gasoline, headline CPI is at a four-year high (2.5%). However, the cumulative effect of the seven rate hikes since the middle of 2017 is still to be seen and, arguably under the weight of a slowdown in the housing market, the economy has lost some momentum. The main report this week is November retail sales. A 0.6% decline, which is what the median Bloomberg forecast anticipates, would offset the gains since June when it last fell.

The US dollar fell sharply in the first part of the month against the Canadian dollar, but over the past several sessions, including all last week, consolidative tone emerged. That range is roughly CAD1.3230 to about CAD1.3320. We suspect the break will eventually come to the upside and are more inclined to buy pullbacks. The US dollar also slid against the Mexican peso, but that move began earlier than against the Canadian dollar and last longer. The US dollar appears to have bottomed a little below MXN18.89 last week. Initial resistance is pegged near MXN19.22. Gains through there would target MXN19.45.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,Featured,MXN,newsletter