It is not easy to recall another week in which there were so many potential changes to the broad investment climate. The relatively light economic calendar in the week ahead may allow investors to continue to ruminate about some of those developments. Here we provide thumbnail assessments of the main drivers. China The PBOC modified the way the reference rate is set. Currencies are allowed to trade in a band around the reference rate. The US dollar trades in a two percent band, while other major currencies, such as the euro are allowed to trade in a wider band. China had previously introduced what it called a “counter-cyclical” component, which was a bit of a black box, and allowed Chinese officials a tool to exert

Topics:

Marc Chandler considers the following as important: Canada, China, Featured, FX Trends, Germany, Japan, newsletter, U.K., US

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

It is not easy to recall another week in which there were so many potential changes to the broad investment climate. The relatively light economic calendar in the week ahead may allow investors to continue to ruminate about some of those developments. Here we provide thumbnail assessments of the main drivers.

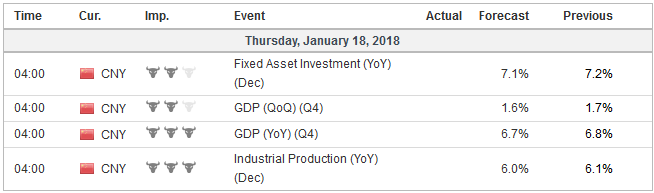

ChinaThe PBOC modified the way the reference rate is set. Currencies are allowed to trade in a band around the reference rate. The US dollar trades in a two percent band, while other major currencies, such as the euro are allowed to trade in a wider band. China had previously introduced what it called a “counter-cyclical” component, which was a bit of a black box, and allowed Chinese officials a tool to exert greater discretionary influence over the currency. This was particularly important when China was in a vicious cycle of currency depreciation and capital outflows. A combination of capital controls and the broadly weaker US dollar environment saw the yuan strengthen and reserves grow over the past year. Officials no longer need the “counter-cyclical” lever, so they jettisoned it. This is seen as a step to allowing market forces greater sway and neutralizes a criticism that had been levied. The apparent embrace of market forces seems opportunistic rather than ideological. There was one newswire story claiming that people close to Chinese officials were advised to be cautious about adding more Treasuries to the country’s reserves. It was like a child’s party game of “telephone” where a message is whispered and by the time the last child hears it, the message is often nothing like the original. By the end of the day, there were reports saying that China was not going to buy any more US Treasuries. The following day, the State Administration of Foreign Exchange (SAFE) suggested the original journalists had either were quoting the wrong people or was fake news. Some then began arguing that China was trapped into holding Treasuries, but this is to misunderstand. The decision of how many Treasuries it wants is a function of the level of reserves it wants. Given the relative size of different asset markets, once the decision is made to accumulate reserves, now in excess of $3.2 trillion, its choices are terribly constrained. Roughly speaking, a little more than 60% of global reserves, including China’s, are invested in US Treasuries. There may be room for a marginal shift into euros, which China appears to have below average exposure, but the cost is significantly lower yields and less liquidity. Moreover, European officials are buying all of the net new supply. Lastly, we note that the dollar bond market is huge, and in any event, bigger than China. We see little correlation between the month-to-month changes in China’s Treasury holdings, reported by the US Treasury, and the change in US yields. |

Economic Events: China, Week January 15 - Click to enlarge |

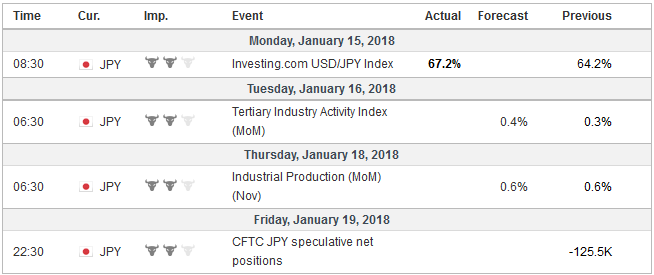

JapanThe Bank of Japan’s extraordinary monetary policy has evolved under Governor Kuroda. The shift to yield curve targeting from an aggressive quantitative easing requires the purchase of few government bonds to achieve the goal. Consequently, the BOJ bought fewer bonds than the JPY80 trillion signaled. The BOJ does not know how much buying will be required, nor is it committed to replacing maturing issues like other central banks, including the Fed, ECB, and BOE. The BOJ balance sheet did shrink slightly in December. It was a bit of a quirk. The BOJ it is not content with the progress on inflation. Officials have been explicit that they will continue to pursue an aggressive monetary policy to achieve the inflation target. While the BOJ slightly trimmed the amount of bonds with long maturities that it was buying, it has not changed the purchases of short- and medium-term securities, or the others assets that it buys, including ETFs, J-REITs, and bank loans. Even if many observers were confused by the BOJ’s operation, it was a good reminder to investors and policymakers alike about the sensitivity to a perceived change in policy. It may show the limits of forward guidance, with the BOJ saying this is not a change in policy and some investors saying “yes, it is.” This also underscores our discomfort with the concept of quantitative tightening. The Fed has been seemingly clear on this point. Reducing the balance sheet is not about monetary policy, even if the expansion of the balance sheet was. The primary tool for monetary policy is the Fed funds target range. The next step in the evolution of the BOJ’s policy may be a change in the target of the 10-year JGB. Now it stands at +/- 10 basis points on either side of zero. If the synchronized global upturn continues to spill-over and supports the Japanese economy, BOJ officials prepared to lift the target. The timing though may be involved the appointment of the new BOJ Governor. Kuroda’s term ends in early April. |

Economic Events: Japan, Week January 15 - Click to enlarge |

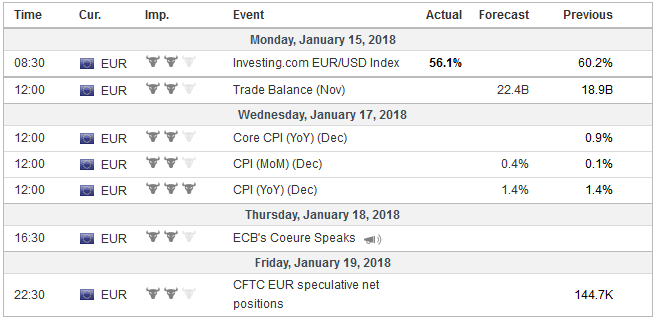

EurozoneThe record from last month’s ECB was read particularly hawkishly by market participants. The euro and interest rates jumped. The focus apparently was on a couple of lines suggesting that the forward guidance will likely change early this year. The market reacted like this was new news, and we suspect that many ECB officials were surprised by the market reaction. We think comments by Draghi, who takes pains to be clear about what was and wasn’t discussed, at the press conference delivered essentially the same message. More market participants began talking about an ECB rate hike this year. We think it is far-fetched, and before the weekend Bundesbank President Weidmann cautioned against the rate hike speculation. Recall too the meeting was before the December flash CPI reading, which disappointed (core rate was unchanged at 0.9%), and it will likely be confirmed when the report is out in the coming days. The ECB’s record was indeed upbeat but was also clear that inflation continued to undershoot, and that is was committed to the sequence of finishing asset purchases and then, after some time, lifting rates. If anything, the strong euro will dampen inflation pressures and squeeze earnings. Anglo-American companies are more likely to pass along currency developments to customers, while Continental and Japanese businesses appear to put more emphasis on market share than short-term profitability, are less likely. The rule of thumb is that a 6% appreciation on a trade-weighted basis has the equivalent impact of 100 bp tightening on economic conditions. The euro’s 2.5% appreciation on a trade-weighted basis is tantamount to a 40 bp tightening of monetary policy. How will the ECB’s forward guidance evolve? The ECB record was clear. The vast majority do not want to delink inflation from the asset purchases. Announcing firm date-end to the purchases, as some of the hawks have argued, will, in fact, delink the two. The policy would become date-dependent, not data-dependent. Instead, a more likely course, we suspect is providing some guidance about the other components of ECB’s unconventional monetary policy. Recall too that starting near mid-year, European banks can repay the TLTRO borrowings early. They had borrowed around 750 bln euros. A small, say 10%, early prepayment would offset 2 1/2 months of ECB purchases, and spur a reduction of the ECB’s balance sheet just as officials begin to provide guidance of what is going to happen at the end of September when the 30 bln a month of purchases is to conclude. |

Economic Events: Eurozone, Week January 15 - Click to enlarge |

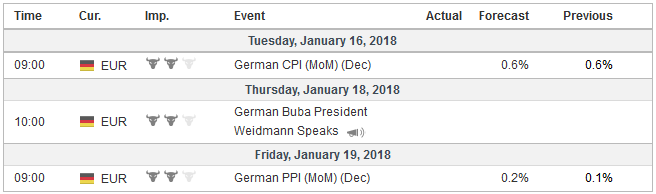

GermanySome of the euro’s gains before the weekend were attributed to news that the CDU/CSU and the SPD reached an agreement, but the agreement was not to form a new government, as several reports suggested, but an agreement to begin formal talks. Even if this agreement increases the likelihood of a new Grand Coalition, it is not a done deal. The SPD holds a party congress on January 21 and will vote whether to proceed with negotiations. If negotiations for begin, the members will vote by mail on the final agreement. The preliminary agreement gives a sense of the direction of a new government. Both the CDU/CSU and SPD were punished by voters with the weakest support in modern times. A somewhat more pro-Europe stance is likely but falls well shy of SPD leader Schulz vision of a United States of Europe. There is also the suggestion that there could be a modest middle-class tax cut, and a plan to end the solidarity levy introduced for reunification. One of the arguments against a Grand Coalition is that populist AfD would be the main opposition party. In Germany’ s parliamentary system, the main opposition party is credited with certain privileges and committee representation, which may give it a larger platform. |

Economic Events: Germany, Week January 15 - Click to enlarge |

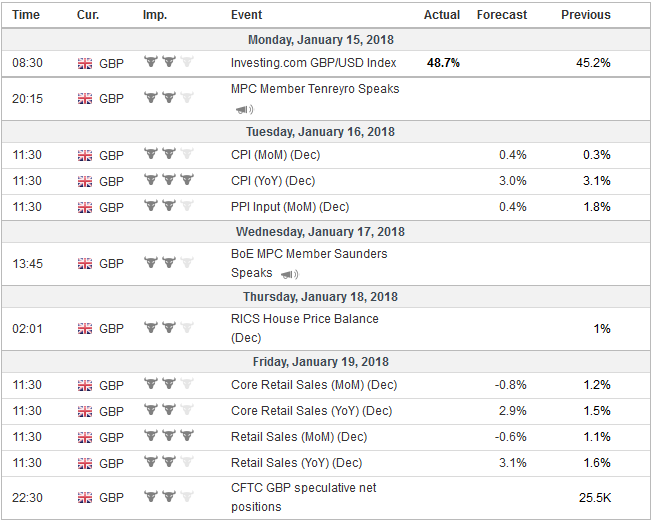

United KingdomPrime Minister May’s troubled cabinet shuffle did appear to shift power between the hard and soft Brexit factions. Sterling’s strength had appeared to be mostly a function of the dollar’s weakness, but the gains were bolstered by reports that the Spanish and Dutch finance ministers were endorsing more generous terms of negotiations. This too was exaggerated. Since the UK’s referendum in mid-2016, the other EU countries have shown a united front. Neither Spain nor the Netherlands is defecting. Of course, the EU wants a deal that keeps the UK as close as possible to the EU. Moreover, we note that Spain’s de Guindos is thought to be a leading candidate to replace Constancio as vice president of the ECB in June. On the other hand, the prospect of a second referendum, which has been talked about almost since the last referendum that had been decided by a tight 52-48 margin may be increasing. Some recent polls have suggested that the Remain camp would win if another referendum was held. |

Economic Events: United Kingdom, Week January 15 - Click to enlarge |

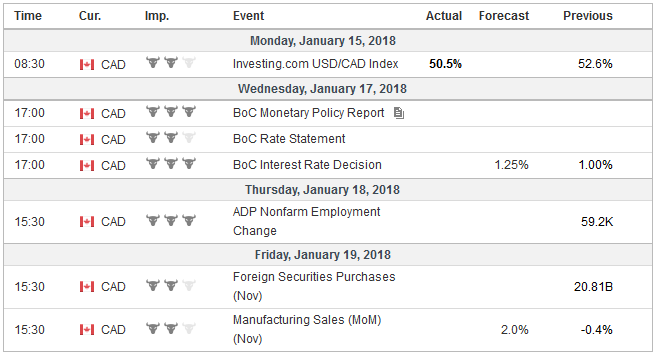

CanadaIt is the only major central bank to meet in the week ahead, and it will most likely hike rates. We had thought that the stagnation of the economy net-net since the two rate hikes in Q3 (judging from the monthly GDP readings), signs of softness in house prices in Toronto and Vancouver areas, coupled with the strength of the Canadian dollar and NAFTA uncertainties would have removed any sense of urgency from the central bank. However, the closing of the output gap and the accelerated jobs growth has given the Bank of Canada what is tantamount as a free option to remove some accommodation, which it says it wants to do. The speculative market is not nearly as long the Canadian dollar in the futures market as it was at the end of September. The gross long position of 17.5k contracts compares with 74.6k at the end of Q3. The net long position stood at 58.6k contracts as of January 9. It was over 100k at the end of September. Nevertheless, we suspect the market is still vulnerable to buy the rumor sell the fact type of trading, or outright disappointment if the Bank of Canada stands pat. |

Economic Events: Canada, Week January 15 - Click to enlarge |

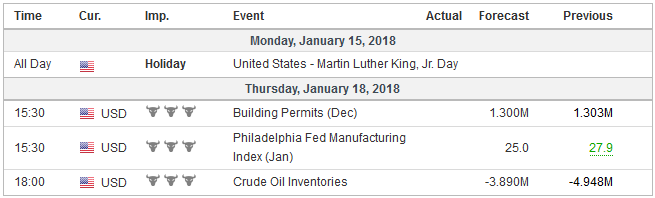

United StatesThe most recent data strengthen the conviction that the US economy finished 2017 on a firm note. The Atlanta Fed’s GDPNow tracker was boosted to 3.3% from 2.8%. The New York Fed’s model is tracking 3.9% Q4 GDP and 3.2% Q1 18 GDP. The market is slightly more confident that the Fed will hike rates in March. The implied odds rose to almost 88% from a little less than 70% than at the end of last year. The US 2-year note poked through 2% before the weekend, though the last price was just below that threshold that has not been seen since the financial crisis. Market-based measures of inflation are rising. The two-year breakeven rose to 1.74% at the end of last week and represents more than a 40 bp increase since the end of November 2018. The two-year yield has risen by half as much. The 10-year breakeven pushed to has moved above 2.0% this year and is within spitting distance of last year’s 2.07% high. It was near 1.88% at the end of November. The 10-year yields have risen by about 20 bp over the same period. Walmart joined a growing list (now reportedly over 100) of companies who are giving employees bonuses or other payments (like 401k contributions), and some are boosting wages. The companies are citing the recently passed tax cuts. Although there may be some cynicism over motivations, there are two important takeaways. First, these actions coupled with minimum wage increases should help boost income (and therefore consumption). Second, the bombastic rhetoric should not distract from the fact that through the tax cuts, deregulation, and federal court appointments, the Trump Administration is implementing the traditional (US) conservative agenda. This is creating a large windfall for corporations and their owners that may not be fully appreciated. The US Q4 corporate earnings season kicks off formally in the week ahead. The earnings of the S&P 500 are expected to have risen by about 12% from Q4 16. The S&P 500 rose 19% in 2016. Meanwhile, the political drama will be about the spending authorization that ends January 19. Part of the compromise to extend the spending authorization, and unlike the tax cuts, Democrat votes are necessary, entailed a resolution of the status of the undocumented immigrants who came to the US as children. But President Trump’s recent comments have threatened to sour the negotiations. This means that there is a greater risk that “non-essential” functions of the government may experience a shutdown. It seems to be more a political calculation (who will be blamed?) than a principle or economic interest at stake. Still, in lieu of a formal agreement that would address the discretionary budget, a continuing resolution that kicks the can a few weeks appears to be the most likely scenario. That would have a limited market impact, and we suspect a short closure of the government would not be disruptive, even if embarrassing and seemingly politically inept. |

Economic Events: United States, Week January 15 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week January 15 - Click to enlarge |

Tags: Canada,China,Featured,Germany,Japan,newsletter,U.K.,US