Marc Chandler

August 14, 2016

SNB & CHF

Summary:

The GDP deflator may be just as important as overall growth for BOJ considerations and the possibility of fresh action next month.

Falling UK rates and a weaker pound are desirable from a policy point of view.

Dudley’s press conference may be more important than FOMC minutes.

Two German state elections that will be held next month comes as Merkel’s popularity has waned.

Japan

Japan’s Q2 GDP: The...

Read More »

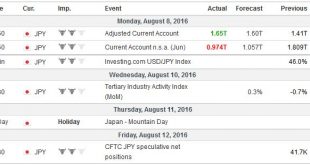

Marc Chandler

August 8, 2016

SNB & CHF

Swiss Franc

Click to enlarge.

FX Rates

Investors favor risk assets today. Global stocks are moving higher in the wake of the pre-weekend US rally that saw the S&P 500 close at record levels. Bond yields are mostly firmer, again with US move in response to the robust employment report setting the tone in Asia. European bonds participated in most of the pre-weekend move and are consolidating today with a...

Read More »

Marc Chandler

August 7, 2016

SNB & CHF

Summary:

Policy outlook is clear: ECB and BOJ review next month, FOMC still looking for opportunity.

Inventory cycle making quarterly US GDP forecasting difficult, but it looks like re-acceleration still the more likely scenario than recessions.

Why didn’t European bank stress tests results have more impact?

The drip-feed of high frequency economic data from the major economies slows in the week ahead. The data...

Read More »

Antonius Aquinas

August 4, 2016

SNB & CHF

Meet the Scapegoats

Last week, an Irish court sentenced three prominent banksters for their roles in the 2008 financial crisis. Judge Martin Nolan, who pronounced judgment, said that the bansksters had committed “a very serious crime.” He continued:

“The public is entitled to rely on the probity of blue chip firms. If we can’t rely on the probity of these banks we lose all hope or trust in institutions.”*

Meet the...

Read More »

Marc Chandler

July 21, 2016

SNB & CHF

Summary:

Draghi does not show the kind of urgency many bank economists do over the shortage of bonds to buy.

Draghi kept options open and suggested a review in September when new staff forecasts are available and more data will be seen.

The euro firmed, mostly it seemed on sell the rumor buy the fact, and/or possibly some disappointment that no fresh action was taken.

Draghi said nothing that surprised the...

Read More »

Marc Chandler

June 17, 2016

SNB & CHF

The assassination of the Jo Cox has broken the powerful momentum in the markets. Investors recognize that the tragedy potentially injects a new element into consideration for the outcome of next week’s referendum. The campaigns will be resume over the weekend, and new polls will be available. Investors will place more weight on polls conducted after the assassination.

The UK referendum is the big event next week. ...

Read More »

Marc Chandler

June 6, 2016

SNB & CHF

In March, the ECB decided to increase its asset purchases from 60 to 80 bln euros a month and to include corporate bonds. The corporate bond buying program begins this week. We use an FAQ format to discuss the key issues.

What is the ECB doing? The ECB will buy euro-denominated, investment grade bonds from companies incorporated within the eurozone.

What is the duration of the corporate bonds that the ECB will...

Read More »

Eugen von Böhm Bawerk

June 2, 2016

SNB & CHF

ECB press conference June 2 2016

Held in Vienna with Governor Nowotny

Keep key ECB interest rates unchanged

Will be kept at present or lower for an extended period of time, exceeding asset purchase program (80bn per month) which will end March 2017

sector program will start June 8

TLTRO start in June

New measures will strengthen growth in euro area through credit expansion

Very low inflation must not become entrenched in second round effects through effects on wages and prices.

ECB...

Read More »

Marc Chandler

May 29, 2016

SNB & CHF

The US dollar bottomed against nearly all the major currencies on May 3. The hawkish April FOMC minutes that began swaying opinion about the prospects for a summer rate hike were not published until two weeks later, and the confirmation by NY Fed President Dudley was not until May 19.

Nevertheless, the shift in expectations for a resumption of the Fed’s gradual normalization of monetary policy is a potent force that has fueled the greenback’s recovery. The place to look for investors’...

Read More »

Marc Chandler

May 29, 2016

SNB & CHF

The US dollar bottomed against nearly all the major currencies on May 3. The hawkish April FOMC minutes that began swaying opinion about the prospects for a summer rate hike were not published until two weeks later, and the confirmation by NY Fed President Dudley was not until May 19.

Nevertheless, the shift in expectations for a resumption of the Fed’s gradual normalization of monetary policy is a potent force that has fueled the greenback’s recovery. The place to look for investors’...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org