May 2022’s payroll estimates weren’t quite the level of downshift President Phillips had warned about, though that’s increasingly likely just a matter of time. In fact, despite the headline Establishment Survey monthly change being slightly better than expected, it and even more so the other employment data all still show an unmistakable slowdown in the labor market. What’s left open for argument and concern is now a matter of how much of a downside there might end up being. Politicians and other officials have confidently reassured the public this is a natural and welcome progression or transition from red-hot inflation-y to, in the President’s word, stability. Markets (inverted curves) are stridently betting there’s more to it than that; and by more, they’ve

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, average weekly earnings, currencies, economy, employment, establishment survey, Featured, Federal Reserve/Monetary Policy, household survey, inflation, labor force, Labor market, Markets, newsletter, payrolls, unemployment rate, wages

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| May 2022’s payroll estimates weren’t quite the level of downshift President Phillips had warned about, though that’s increasingly likely just a matter of time. In fact, despite the headline Establishment Survey monthly change being slightly better than expected, it and even more so the other employment data all still show an unmistakable slowdown in the labor market.

What’s left open for argument and concern is now a matter of how much of a downside there might end up being. Politicians and other officials have confidently reassured the public this is a natural and welcome progression or transition from red-hot inflation-y to, in the President’s word, stability. Markets (inverted curves) are stridently betting there’s more to it than that; and by more, they’ve priced less. |

. |

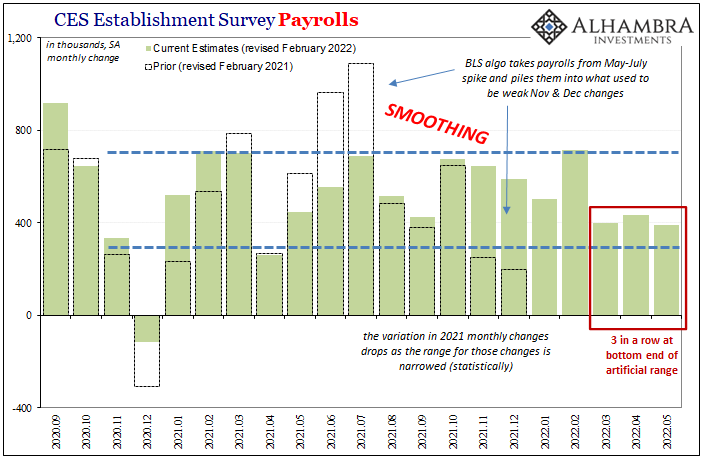

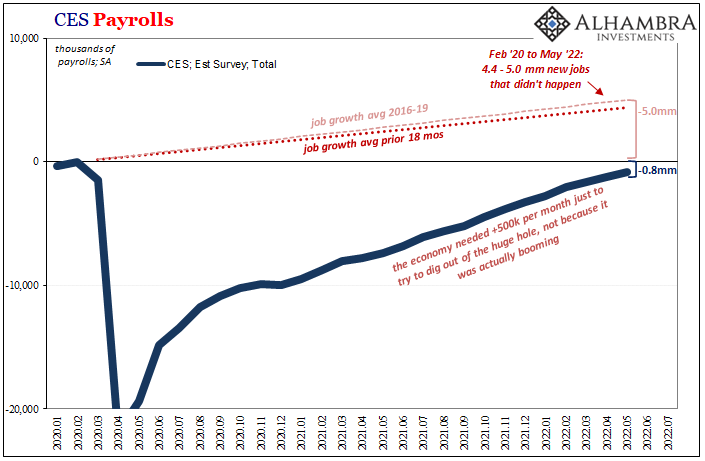

| It had been thought that the Establishment Survey would add about 350,000 this month, down from the 450,000 or so over the past few months and on the way toward the 150,000 Biden had predicted. The BLS today reported a rise of 390,000 seasonally-adjusted April to May, but also downward revisions to each of the prior two (March and April). It all evened out in the end, which is exactly what CES is “famous” for.

Having set up basically an arbitrary statistical range, we have to judge the data by those bounds rather than by indicated headcount. While 400,000 months are double what the labor market used to average before 2020, that’s not an apples-to-apples comparison. Building off this year’s benchmark changes, we start with how between October 2021 and February 2022 the monthly gains were consistently near the top of the range. Since gasoline prices surged in March, they now average consistently near the bottom. With three in a row in that position, chances of this being random noise or statistical aberration fall with each successive monthly datapoint. |

. |

| Rather than looking at +390,000 and breathing a politics-sized sigh of relief thinking all is well, the economy seemingly hanging in there despite all the headwinds, what the data actually shows is that something changed.

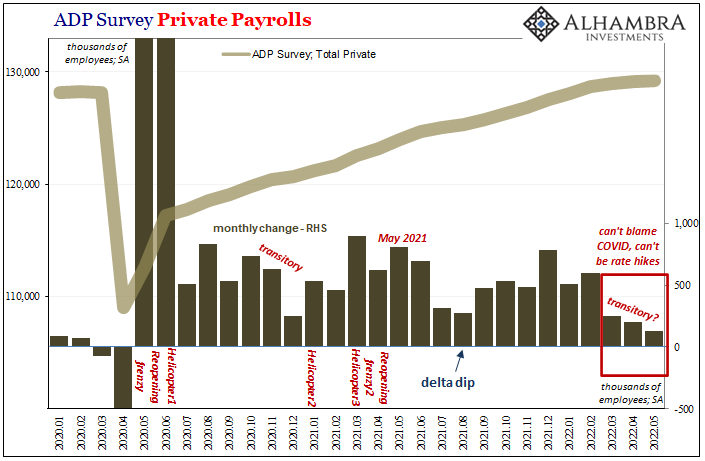

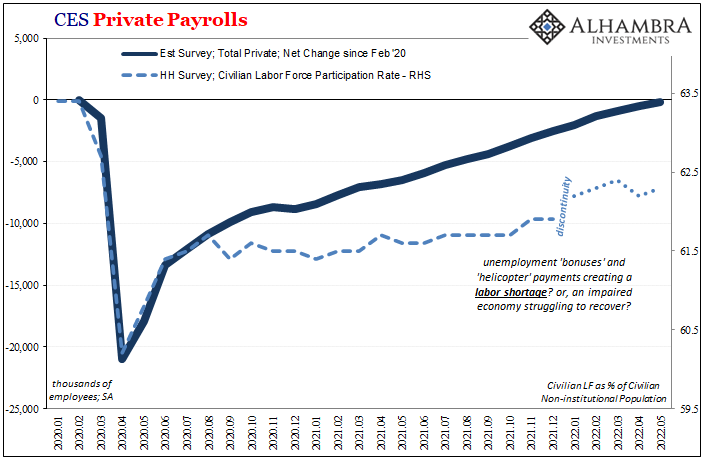

This “something changed” is replicated all over both the CES and CPS figures (ADP’s, too). I pointed out last month how it had been the Household Survey which already suggested that very point. Given the HH is the noisy stepcousin of CES means you can’t put too much emphasis on a single month of data, though the fact that it was the first decline since the recession in 2020 already strongly proposed there was more to it than randomness. By being substantially negative, that itself meant there was a more than significant possibility April truly had been a “bad” month for workers even if we couldn’t say for sure just how bad. As expected, the latest HH employment estimate for May rebounded, though not enough to offset last month’s drop. |

. |

| In other words, that’s two months in a row where the net change remains a minus, reducing the chances this is some anomaly down even more, simultaneously propelling the possibility the data really is picking up something bad, at the very least like the Establishment Survey some as-yet undetermined downturn in the labor market.

To show you what I mean, look (below) at how many times (how few) the HH Survey has been negative on any two-month basis over the last eleven years dating back to 2011 and the start of the labor market “recovery” after the Great “Recession.” Apart from 2013’s government shutdown and 2017’s double-hurricane wreck, there are only a handful of two-month minuses and every one of those corresponds with economic downturn. |

. |

| The HH Survey also agrees with CES as to the latter half of last year and some part of this year. Both indicate an acceleration in the labor market, though in this series it was thought to have occurred between July 2021 and March 2022.Given that Euro$ #5 began back in May 2021 (by my unofficial declaration), this acceleration ran contrary to what “should” have been, and normally would’ve been, a much quicker downshift in employment (factoring employment as a lagging indicator) therefore strongly suggesting that particular upswing in labor had been non-economic; the last big push of the final reopening (after the delta-COVID interference). |

. |

| That not actual recovery is almost certainly why the employment situation had seemingly defied Euro$ #5, if only until more recently.

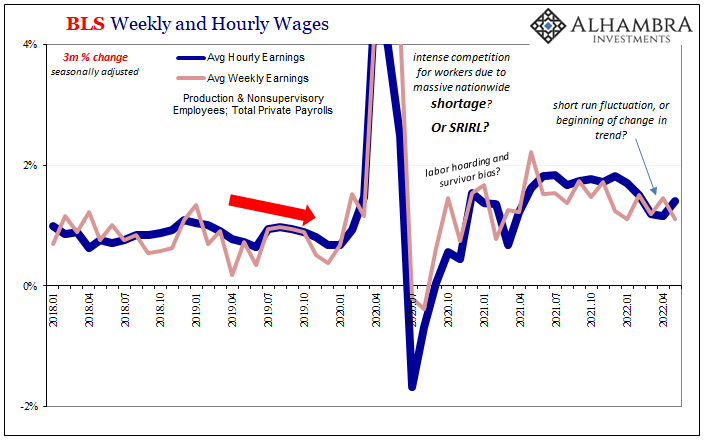

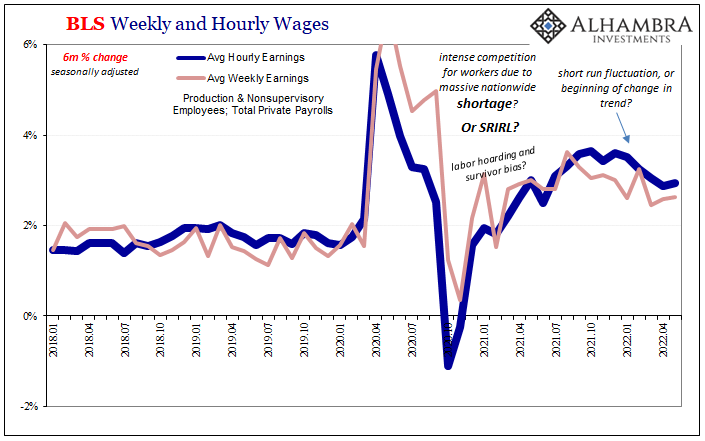

In other words, the economy finished up last year and began this year on far more uncertain ground than it might otherwise have appeared, or had been made to appear (especially when viewed from any CPI perspective). The jobs market wasn’t taking off into the red-hot stratosphere of Phillips Curve inflation, merely still trying to dig out from the prior huge hole, more and more struggling to do so as that momentum of reopening began to fade. The difference between those two scenarios accounts for what we see developing now (and why markets have been priced in anticipation of it). Had it truly been inflation/max employment/full recovery playing out instead of mere reopening, we wouldn’t see wage gains decelerate as they have nor could we account for the timing. |

. |

| If the economy was playing currently by the Phillips Curve, we’d be at if not above full employment and wages would be accelerating wildly – you know the thing: labor shortage and scarce workers driving competition among companies who then have to pass higher employment costs back to consumers.

It’s not a crash in wages by any means, but that’s not something you ever see anyway. Second derivatives are what matter here, and whether by 3-month change or 6-month, wage gains in hourly and weekly terms are absolutely slowing down and have been since late last year (that is Euro$ #5 not labor shortage). Even the level of acceleration in wages had always been a product of the supply shock, too, like overall consumer prices a much faster recovery in demand for workers than the labor market’s ability to supply them. |

. |

| It wasn’t ever a shortage, just the same artificial imbalances (rightward shift in demand given inelasticity in worker supply, often self-imposed, raising prices but not the overall level of activity; see: below). |

. |

Put it all together and, yes, labor market downturn, though one stemming from the emerging downside to that supply shock and not an inflationary overshoot beyond recovery now being rescued by a proactive government goosed up on rate hikes (and the absurdity of QT’s theatrical manipulation of always-useless bank reserves). As I wrote a few days ago:

There’s a vast difference between things-are-great-so-pump-the-brakes-a-little-bit and the-plane-never-really-got-far-off-the-ground-and-now-its-engines-have-shut-down. Political theater surrounding rate hikes and now this administration-wide lean on the Phillips Curve is all about making believe of the former.

Therefore, the slowdown that is already all over every bit of labor market data looks very different from the “stability” pitched by President Phillips. Despite this month’s headline relief, even that is more than it seems. And by more, like markets I mean less.

You Might Also Like

ADP Front-Runs BLS and President Phillips

ADP Front-Runs BLS and President Phillips

2022-06-04

It’s gotten to the point that pretty much everyone is now aware of the risks. Public surveys, market behavior, on and on, hardly anyone outside politics thinks the economy is in a good place. Gasoline, sentiment, whatever, Euro$ #5 in total is much more than what’s shaping up inside the American boundary. Globally synchronized of which the US is proving to be a close part.

Neither Confusing Nor Surprising: Q1’s Worst Productivity Ever, April Decline In Employed

Neither Confusing Nor Surprising: Q1’s Worst Productivity Ever, April Decline In Employed

2022-05-13

Maybe last Friday’s pretty awful payroll report shouldn’t have been surprising; though, to be fair, just calling it awful will be surprising to most people. Confusion surrounds the figures for good reason, though there truly is no reason for the misunderstanding itself. Apart from Economists and “central bankers” who’d rather everyone look elsewhere for the real problem.

For The Fed, None Of These Details Will Matter

For The Fed, None Of These Details Will Matter

2022-03-06

Most people have the impression that these various payroll and employment reports just go into the raw data and count up the number of payrolls and how many Americans are employed. Perhaps the BLS taps the IRS database as fellow feds, or ADP as a private company in the same data business of employment just tallies how many payrolls it processes as the largest provider of back-office labor services.That’s just not how it works, though. In fact, sampling and statistical processing first, and then something called trend-cycle (cringe). Benchmarking is in many ways about just this; subjectively estimating the “baseline” economic trend and then for the high frequency data marking up or down any monthly changes from it (I’m oversimplifying on purpose). For employment data more than any other

Taper Discretion Means Not Loving Payrolls Anymore

Taper Discretion Means Not Loving Payrolls Anymore

2022-01-10

When Alan Greenspan went back to Stanford University in September 1997, his reputation was by then well-established. Even as he had shocked the world only nine months earlier with “irrational exuberance”, the theme of his earlier speech hadn’t actually been about stocks; it was all about money.The “maestro” would revisit that subject repeatedly especially in the late nineties, and it was again his topic in California early Autumn ’97.

How Many More Americans Might Have Quit Their Jobs Than The Huge Number Already Estimated, And What Might This Mean For FOMC Taper

How Many More Americans Might Have Quit Their Jobs Than The Huge Number Already Estimated, And What Might This Mean For FOMC Taper

2022-01-07

There were a few surprises included in the BLS JOLTS data just released today for the month of November (note: the government has changed its release schedule so that JOLTS, already one month further in arrears than the payroll report, CES & CPS, will now come out earlier so that its numbers are publicly available for the same monthly payrolls before the next CES & CPS get released).

As The Fed Tapers: What If More Rapid (published) Wage Increases Are Actually Evidence of *Deflationary* Conditions?

As The Fed Tapers: What If More Rapid (published) Wage Increases Are Actually Evidence of *Deflationary* Conditions?

2022-01-05

Since the Federal Reserve is not in the money business, their recent hawkish shift toward an increasingly anti-inflationary stance is a twisted and convoluted case of subjective interpretation.

A Global JOLT(s) In July

A Global JOLT(s) In July

2021-12-09

The Bureau Labor Statistics reported today another huge month for Job Openings (JO). According to their methodology (which I still believe is flawed, but that’s not our focus this time), the level for October 2021 (JOLTS updates are for one month further back than payrolls) was a blistering 11.03 million.

Tags: average weekly earnings,currencies,economy,employment,establishment survey,Featured,Federal Reserve/Monetary Policy,household survey,inflation,labor force,Labor Market,Markets,newsletter,payrolls,unemployment rate,wages