Last week’s 50 bps Fed rate hike was not a surprise. Indeed, Fed chairman Jerome Powell’s assertion that a 75 bps hike had not been actively considered was enough to spark a stock rally. But it proved short-lived, with markets quickly returning to their fears about inflation. With the US labour market remaining tight and with inflation running well ahead of wage growth (the consumer price index rose an annual 8.5% in March, a four-decades high, compared with a 5.5% rise in average hourly earnings in April), markets may not be fully assured we won’t have a wage-price spiral, even as US credit growth continues to surge and consumers are still sitting on cash accumulated during the pandemic. With markets preferring the inflation threat to be tackled swiftly, they

Topics:

Perspectives Pictet considers the following as important: 2.) Pictet Macro Analysis, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Last week’s 50 bps Fed rate hike was not a surprise. Indeed, Fed chairman Jerome Powell’s assertion that a 75 bps hike had not been actively considered was enough to spark a stock rally. But it proved short-lived, with markets quickly returning to their fears about inflation. With the US labour market remaining tight and with inflation running well ahead of wage growth (the consumer price index rose an annual 8.5% in March, a four-decades high, compared with a 5.5% rise in average hourly earnings in April), markets may not be fully assured we won’t have a wage-price spiral, even as US credit growth continues to surge and consumers are still sitting on cash accumulated during the pandemic. With markets preferring the inflation threat to be tackled swiftly, they have been doing the Fed’s job by squeezing bond yields higher, hurting growth stocks in particular.

Last week saw other central banks continue to scramble to deal with persistent inflation. The Central Bank of Brazil and the Bank of England raised policy rates, as did (more unexpectedly) the Australian Reserve Bank and the Reserve Bank of India. The Bank of England’s (BoE) 25 bp rate hike came with some gloomy comments about the path ahead. The Bank thinks inflation could peak at an annual rate of over 10% only in October and also sees the UK economy contracting later this year. Just as in eastern Europe (although the Russian president Vladimir Putin did not use his Victory Day speech to officially declare war on Ukraine), the geopolitical temperature is rising on Europe’s western fringe. After the rise of the Scottish National Party, the nationalist Sinn Féin’s triumph in the Northern Ireland election could feed speculation about the breakup of the UK. What about the European Central Bank (ECB)? Some of its policymakers have made it clear that deposit rate could start to rise in July. Some countries are more vulnerable to rate rises than others, with Italian spreads hitting 200 bps last week. How the ECB manages to help countries facing higher funding costs will be an important test of its credibility, especially as it is scheduled to reduce its net purchases of government bonds. Yet the ECB may want to move fast to avoid raising rates in a declining economic environment later in the year. In the meantime, we remain underweight European government bonds.

All in all, volatility remains high on equity and bond markets alike. And yet; despite all the market anxiety, Q1 earnings reports have been decent. And while market conditions have become more challenging, discerning investors are still making liquidity available for some initiatives. Fitting in neatly with our sustainability theme, a high-profile climate fund last week raised USD7.5 bn.

You Might Also Like

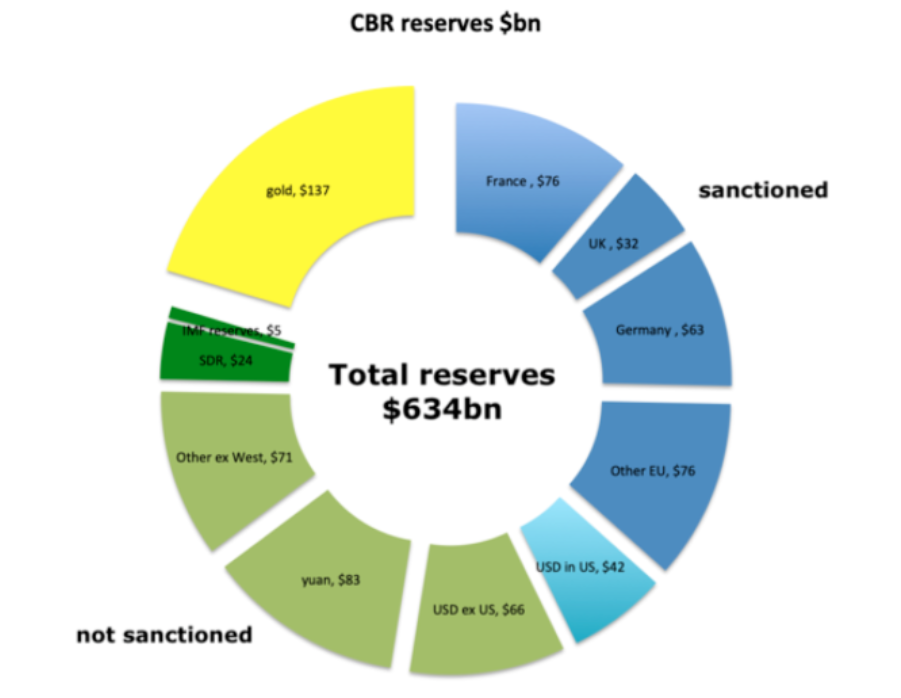

Heavy Sanctions against Russia Could Usher in a Wider Economic War

Heavy Sanctions against Russia Could Usher in a Wider Economic War

2022-04-11

Vladimir Putin’s invasion of Ukraine was met with unprecedented economic sanctions by the United States and its allies in order to cripple Russia’s capacity to wage war. Never before in post–World War II history has an economy of Russia’s size been reprimanded with such force. Moreover, the sanctions could remain in place after the war ends and reach other major economies too, in particular China. In this case, current sanctions could be the harbinger of a longer-term economic war with dire consequences for global productivity and welfare.

Sweeping Sanctions Invite Countersanctions

The round of sanctions imposed on Russia following the annexation of Crimea in 2014 were limited to travel bans, freezing of the assets of certain Russian officials, and a prohibition of credit and technology

Inflation vermeiden: Wie du deine Inflationsrate reduzierst!

Inflation vermeiden: Wie du deine Inflationsrate reduzierst!

2022-04-10

Inflation vermeiden: So reduzierst du deine Inflationsrate!

Kostenloses Depot eröffnen (+20€ Prämie): ►► https://link.finanzfluss.de/go/depot?utm_source=youtube&utm_medium=481&utm_campaign=comdirect-depot&utm_term=kostenlos-25&utm_content=yt-desc *?

In 4 Wochen zum souveränen Investor: ►► https://link.finanzfluss.de/go/campus?utm_source=youtube&utm_medium=481&utm_campaign=ff-campus&utm_term=4-wochen&utm_content=yt-desc ?

ℹ️ Weitere Infos zum Video:

Im heutigen Video geht es um die aktuell hohe Inflation. Wir zeigen euch welche Produkte besonders teuer geworden sind und was ihr tun könnt um eure persönliche Inflationsrate zu verringern. Die Daten stammen vom statistischen Bundesamt.

• Quelle der Inflationsdaten:

Börsenpsychologie – Tipps und Tricks für volatile Zeiten mit @André Stagge

Börsenpsychologie – Tipps und Tricks für volatile Zeiten mit @André Stagge

2022-04-07

02:04 Risiko- und Warnhinweis flatex

03:51 Start "Börsenpsychologie – Tipps und Tricks für volatile Zeiten"

05:47 Haftungsausschluss und Risikohinweis

06:06 IS THAT A LONG OR A SHORT POSITION?

09:25 Die meisten Trader verlieren an der Börse Geld

14:24 Aber auch Investoren tun sich schwer

16:59 Unser Gehirn ist nicht dafür gemacht, mit Geld umzugehen

19:20 Performance Coaching

21:49 Die Formel für Ihren Börsenerfolg

23:27 Verhalte Dich rational – es dreht sich nichts

27:11 Psychologie ist entscheidend für den Erfolg!

35:28 Die drei Schritte des Performance Coachings

37:31 Kenne Deine Glaubenssätze!

39:12 Kenne Deine Stärken und Schwächen

40:24 Stärken-Test "Bestimmheit"

44:00 Welche Trader-Persönlichkeit hast Du?

44:41 Stärken-Test "Orientierung"

45:44 Welche Trader-Persönlichkeit hast

The Businessman and the Holy Family

The Businessman and the Holy Family

2021-12-30

At the heart of the Christmas story rests some important lessons concerning free enterprise, government, and the role of wealth in society. Let’s begin with one of the most famous phrases: “There’s no room at the inn.” This phrase is often invoked as if it were a cruel and heartless dismissal of the tired travelers Joseph and Mary.

The Real Reason Politicians Want Legal Cannabis Is Tax Money

The Real Reason Politicians Want Legal Cannabis Is Tax Money

2021-12-28

The latest two states to legalize recreational cannabis are New York and New Jersey. However, if one believes governors and legislators in those states have finally adopted a more libertarian view of the topic, one will be severely disappointed.

Position Priority Teil 2 – so optimierst du deine Trading Performance

Position Priority Teil 2 – so optimierst du deine Trading Performance

2021-12-27

✅ Gratis Trading Basiskurs: https://thomasvittner.com/traderkurs1

▶️ Alle Ausbildungsangebote: https://thomasvittner.com/trading-angebote/

TITEL & INHALT VIDEO

In Teil 1 über die Position Priority (Video hier: ) haben wir gezeigt, welche Effekte mit der Position Priority entstehen. In diesem Video prüfen wir nun, wie groß die Unterschiede bei Performance und max. Drawdown sind, wenn wir verschiedene Priorisierungs-Logiken auf verschiedenen Aktienportfolios anwenden.

? Weiterführende Infos zu diesem Thema

– Video Position Priority Teil 1:

– Blog Post mit ergänzenden Infos: https://thomasvittner.com/position-priority-so-reihen-sie-ihre-trades-professionell/

? ?? Gefällt Dir dieses Video? ???

Dann freue ich mich über einen Daumen nach oben, oder über einen Kommentar und wenn Du

“Aktien steigen weiter!” (mit Marc Friedrich)

“Aktien steigen weiter!” (mit Marc Friedrich)

2021-12-15

► Hier kommt ihr zum Kanal von Marc Friedrich: https://www.youtube.com/c/MarcFriedrich7

Wo steht der Bitcoin in 10 Jahren? Sind es tatsächlich siebenstellige Kurse? Und was ist mit Gold und Silber? Fällt die große Rallye aus, oder kommt sie vielleicht doch noch? Und sollte man, angesichts der steigenden Inflationsraten, überhaupt noch auf Aktien setzen? Diese, aber auch sehr viel gesellschaftlichere Themen, bespreche ich heute mit meinem Gast Marc Friedrich.

► Sichere Dir meine Tipps zu Gold, Aktien, ETFs – 100% gratis: http://lars-erichsen.de/

► NEU: Gewinne von bis zu +170%… Mein exklusives Lars-Erichsen-Depot: https://www.rendite-spezialisten.de/video/depot/

——–

► Höre Dir auch meinen Podcast an! Hier findest Du ihn bei

• Google Podcasts:

Weekly View – Big Splits

Weekly View – Big Splits

2021-11-16

US prices continue to rise, with the US consumer price index (CPI) for October coming in at its highest in three decades. President Biden made a boldly worded response as inflation becomes a growing focus among politicians with their eyes fixed on next year’s midterm elections. Oil prices fell on investors’ expectations that the US could free up strategic reserves to combat energy inflation.

Tags: Featured,newsletter