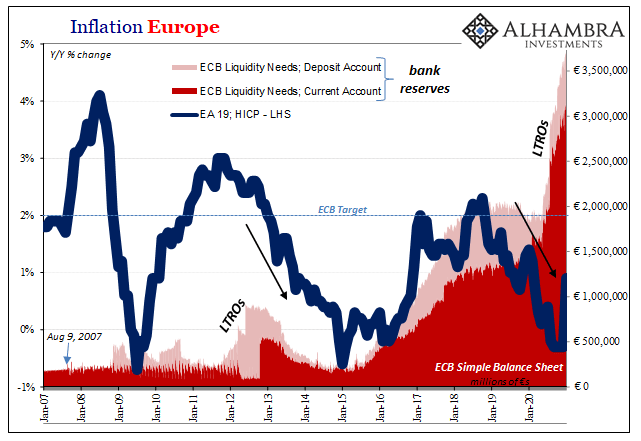

Everyone in Europe has long forgotten about what was going on there before COVID. First, an economy that had been stuck two years within a deflationary downturn central bankers like Italy’s new recycled top guy Mario Draghi clumsily mistook for an inflationary takeoff. Both the inflation puzzle and ultimately a pre-pandemic recession have taken a back seat to everything corona. Whereas Draghi spent those years howling for inflationary conditions that were nowhere in sight – and plenty which unambiguously dictated its opposite – this supposedly virus-driven recession has provided official cover. Inflation Europe, 2007-2020 - Click to enlarge As a result, official numbers and commentary surrounding them have become more honest. With no one else to blame back

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bank reserves, currencies, ECB, economy, Europe, Featured, Federal Reserve/Monetary Policy, HICP, inflation, Mario Draghi, Markets, newsletter, QE

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

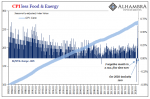

| Everyone in Europe has long forgotten about what was going on there before COVID. First, an economy that had been stuck two years within a deflationary downturn central bankers like Italy’s new recycled top guy Mario Draghi clumsily mistook for an inflationary takeoff. Both the inflation puzzle and ultimately a pre-pandemic recession have taken a back seat to everything corona.

Whereas Draghi spent those years howling for inflationary conditions that were nowhere in sight – and plenty which unambiguously dictated its opposite – this supposedly virus-driven recession has provided official cover. |

Inflation Europe, 2007-2020 - Click to enlarge |

| As a result, official numbers and commentary surrounding them have become more honest.

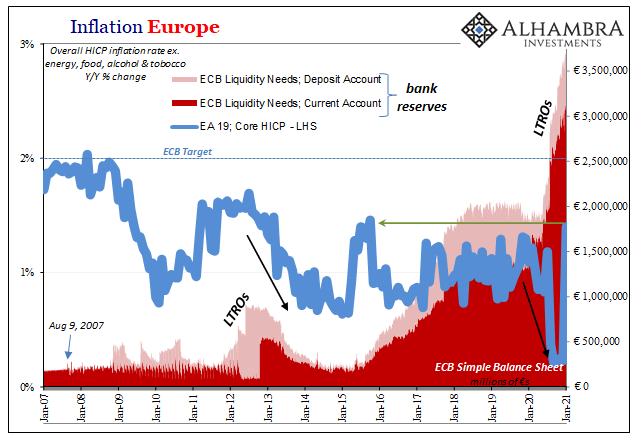

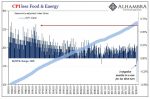

With no one else to blame back then, inflation they said was guaranteed without the slightest trace. Nowadays, even when there might be the slightest trace, those at the ECB, anyway, are approaching this differently. If Eurostat’s flash inflation report for January 2021 had time-traveled back to January 2018 when Draghi was reaching the heights of his unbacked confidence, who knows the greater hysteria which might’ve come from it. Europe’s statistical agency instead reported yesterday that inflation rates jumped last month, accelerating unusually. The headline HICP increase was 0.9% year-over-year, not a whole lot but a serious improvement from five straight months of outright deflation which had December’s rate at -0.3%. The core HICP figure for Europe surged to 1.4% from its record low of 0.2% each the prior three months. Not just well off its lowest ever December to January, the latter’s acceleration left the core number at its highest since 2015. Nobody loves the “highest since…” phrase more than central bankers talking inflation and relatedly interest rates. |

Inflation Europe, 2007-2020 - Click to enlarge |

| Rather than embrace what seems like all its “money printing” coming to fruition finally, the ECB immediately poured reasonable and honest cold water all over it. This wasn’t the economy roaring back to life seasoned by an over-abundance of liquidity, instead the jump in consumer prices were products of one-off factors related largely to governments beginning January 1 reimposing full VAT tax rates previously suspended last year as “stimulus” measures.

Even Bloomberg wasn’t buying it, the headline all you’d need: Euro-Area Inflation Jumps as ECB Warns Against Undue Optimism.

|

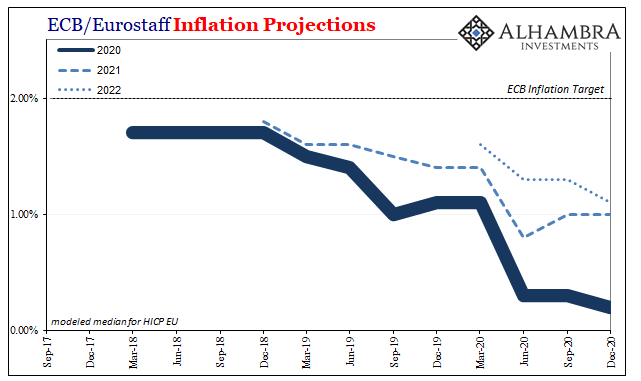

ECB/Eurostaff Inflation Projections, 2017-2020 - Click to enlarge |

| “With wage growth weakening and unemployment expected to increase in 2021, sustainable moves toward target remain a while away.”

In fact, the ECB (and Eurosystem staff) has been downgrading its inflation forecasts all along; which simply raises the uncomfortable question, what is it the ECB has actually been doing all this time? If these projections are what Economists working for the central bank and the central government actually believe of QE’s effectiveness, why are so many in the media and around the world so convinced of some huge inflationary blitz for these same QE’s? As of December’s forecasts, Eurosystem staff downgraded 2020 estimates to just 0.2%, kept 2021 figured for only 1.0% (even knowing what these January numbers would look like) before dropping 2022 down to a paltry 1.1% from the 1.3% the models had been thinking for two years down the road when bank reserves reach, what, €4.5 trillion? Five? More? Trillions in bank reserves, and the first “official” forecast for 2023 (not pictured above) is…1.4%. So much for excessive “money printing” – and this from the very people doing it! In other words, despite all this hoopla, the same mainstream-driven fuss which its own officials relentlessly hyped several years ago during Inflation Hysteria #1, these central bank models don’t believe much in their own same measures. |

Continues Central Bank Failure, 1999-2020 - Click to enlarge |

They’re not thinking of even reaching close to the inflation target, let alone exceeding it in some major way, for years out beyond the current forecast window.

Inflation Hysteria #2, then, oddly enough doesn’t even include the very people who are actually “printing” all the “money” and yet it persists unabated and largely unchallenged. Hysteria #1 at least had Draghi and the rest. Number two is, in every way, even more hysterical. When you really look at the details, it’s not really a stretch as to why the current environment comes up so much short of even Reflation #3. Perhaps those two things really are related and inversely proportional. The worse it is now, the more unsupported the claims it won’t be. As always, this isn’t really about just Europe. |

European Economy, 2004-2020 - Click to enlarge |

European Economy, 2004-2020 - Click to enlarge |

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

2021-02-08

Update February 8 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -0.3 bn. compared to last week, this means the SNB is selling euros and dollars.

They’ve Gone Too Far (or have they?)

They’ve Gone Too Far (or have they?)

2021-01-10

Between November 1998 and February 1999, Japan’s government bond (JGB) market was utterly decimated. You want to find an historical example of a real bond rout (no caps nor exclamations necessary), take a look at what happened during those three exhilarating (if you were a government official) months.

Where Is It, Chairman Powell?

Where Is It, Chairman Powell?

2020-11-15

Where is it, Chairman Powell? After spending months deliberately hyping a “flood” of digital money printing, and then unleashing average inflation targeting making Americans believe the central bank will be wickedly irresponsible when it comes to consumer prices, the evidence portrays a very different set of circumstance.

Meanwhile, Outside Today’s DC

Meanwhile, Outside Today’s DC

2020-11-05

With all eyes on Washington DC, today, everyone should instead be focused on Europe. As we’ve written for nearly three years now, for nearly three years Europe has been at the unfortunate forefront of Euro$ #4. We could argue about whether coming out of GFC2 back in March pushed everything into a Reflation #4 – possible – or if this is still just one three-yearlong squeeze of a global dollar shortage.

Consumer Confidence Indicator: Anesthesia

Consumer Confidence Indicator: Anesthesia

2020-10-24

Europeans are growing more downbeat again. While ostensibly many are more worried about a new set of restrictions due to (even more overreactions about) COVID, that’s only part of the problem. The bigger factor, economically speaking, is that Europe’s economy has barely moved, or at most not moved near enough, off the bottom.

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

2020-10-02

It’s always something. There’s forever some mystery factor standing in the way. On the topic of inflation, for years it was one “transitory” issue after another. The media, on behalf of the central bankers it holds up as a technocratic ideal, would report these at face value. The more obvious explanation, the argument with all the evidence, just couldn’t be true otherwise it’d collapse the technocracy right down to the ground.And so it was also in the bond market. Inflation and their yields very much related, the lack of the former wasn’t ever used to explain the curious absence of the BOND ROUT!!! No, the US Treasury market has been beset by its own set of “transitory” factors, too. As ridiculous as some of the inflation excuses had been, Verizon’s unlimited wireless data plans the

This Has To Be A Joke, Because If It’s Not…

This Has To Be A Joke, Because If It’s Not…

2020-08-28

After thinking about it all day, I’m still not quite sure this isn’t a joke; a high-brow commitment of utterly brilliant performance art, the kind of Four-D masterpiece of hilarious deception that Andy Kaufman would’ve gone nuts over. I mean, it has to be, right?I’m talking, of course, about Jackson Hole and Jay Powell’s reportedly genius masterstroke.

Fama 2: No Inflation For Old Central Banks

Fama 2: No Inflation For Old Central Banks

2020-08-14

The Bureau of Labor Statistics reported that the core CPI in July 2020 jumped by the most (+0.62%) in almost thirty years. After having dropped month-over-month for three months in a row for the first time in its history, it has posted back to back gains the latest of which pushing the index back above its February level.

Tags: bank reserves,currencies,ECB,economy,Europe,Featured,Federal Reserve/Monetary Policy,hicp,inflation,Mario Draghi,Markets,newsletter,QE