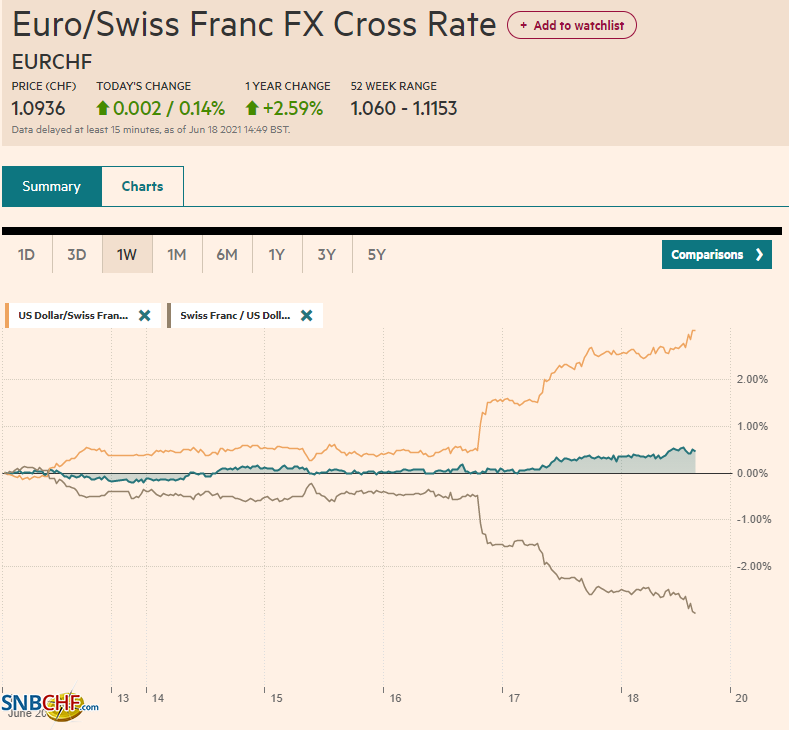

Swiss Franc The Euro has risen by 0.14% to 1.0936 EUR/CHF and USD/CHF, June 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: After some dramatic moves over in the immediate post-Fed period, the markets have quieted. The kind of volatility that is sometimes associated with triple witching expirations in the US may have already taken place. Asia Pacific equities were mixed, but the MSCI benchmark finished with its second consecutive weekly decline. Europe’s Dow Jones 600 ended its nine-day run with a small loss yesterday and additional slippage so far today. Still, near midday, it is holding on to about a 0.25% gain for the week. US futures are steady to slightly firmer. The US 10-year yield unwound the

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Bank of Japan, commodities, Currency Movement, Featured, Federal Reserve, newsletter, U.K., USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.14% to 1.0936 |

EUR/CHF and USD/CHF, June 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

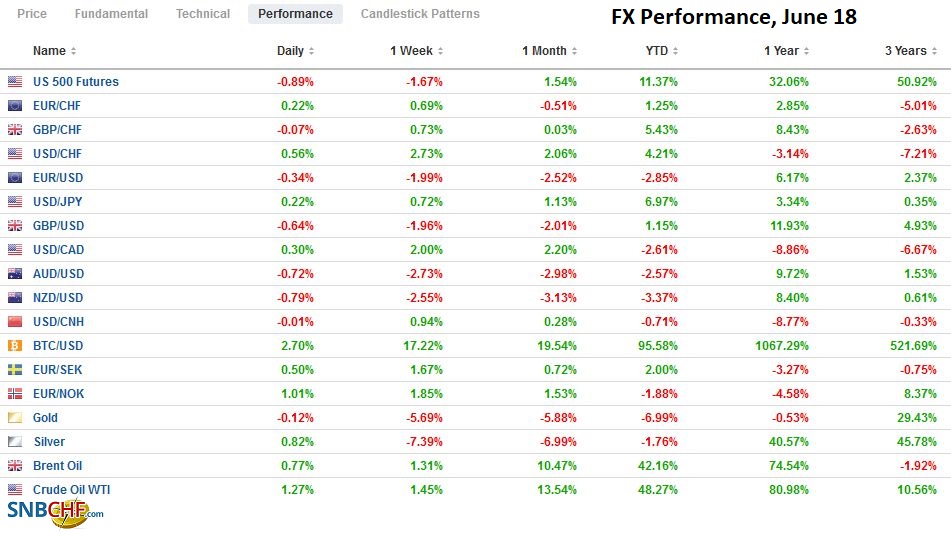

FX RatesOverview: After some dramatic moves over in the immediate post-Fed period, the markets have quieted. The kind of volatility that is sometimes associated with triple witching expirations in the US may have already taken place. Asia Pacific equities were mixed, but the MSCI benchmark finished with its second consecutive weekly decline. Europe’s Dow Jones 600 ended its nine-day run with a small loss yesterday and additional slippage so far today. Still, near midday, it is holding on to about a 0.25% gain for the week. US futures are steady to slightly firmer. The US 10-year yield unwound the gains registered in the immediate aftermath of the Fed’s less dovish signals, and near 1.48%, it is practically flat on the week. Most European yields have edged up today and are 3-5 bp higher on the week. An unexpected decline in UK retail sales and the most Covid cases in a few months appears to have dragged Gilt yields lower. The dollar is mostly firmer against the major currencies, but the euro and yen stable but fragile. The greenback is having its best week here in Q2. The Scandis are the weakest with 2.5%-2.8% losses for the week, while the yen is the strongest, off a little less than 0.5% this week. Emerging market currencies are mostly firmer today, though a handful of Asian currencies are slightly softer. The JP Morgan Emerging Markets Currency Index is posting its first gain in six sessions. Brazil, which hiked its key Selic rate by 75 bp and signaled another hike in August, has the only emerging market currency posting gains for the week (~2.2% coming into today). Gold is also seeing its first gains in six sessions, though it remains below $1800 and is off around 4.5% this week. Oil is nursing its second consecutive loss. The July WTI contract finished last week a touch below $71, and with today’s slippage is near $70.50. Iron ore and steel rebar futures prices are higher, and copper is slightly firmer after dropping 4.7% yesterday. Grains and livestock prices tumbled yesterday, and the CRB Index fell 2.8%. It had not risen so far this week and is off around 3.8% coming into today, which, if sustained, would be the largest weekly loss since before the Covid vaccine was announced. |

FX Performance, June 18 - Click to enlarge |

Asia Pacific

The BOJ made two announcements today while not changing its policy settings. First, it extended its emergency lending facilities for six months through next March. This is not so surprising and was expected now or at the next meeting. Second, and more innovative, it announced the intention to launch a new lending facility to help fight climate change. At his press conference, BOJ Kuroda did not rule out the BOJ buying green bonds at some point. Also, while agreeing that US price pressures may be transitory, Kuroda suggested Fed’s tapering could help lift the dollar against the yen.

Separately, Japan reported that the headline CPI in May improved from -0.4% to -0.1%, slightly better than expected. The core rate, which excludes fresh food, stands at 0.1% after being negative for the previous nine months. However, this seems to reflect the surge in oil and gas prices. Excluding bot fresh food and energy, Japan’s consumer prices were off 0.2% year-over-year, the same as in April.

The dollar slipped below JPY110 in Tokyo but found a bid and continues to straddle the area in the European morning. There is an option for around $975 mln at JPY110.00 that expires today, and another one for a billion dollars there expires on Monday. After the Fed’s announcement in the middle of the week, the dollar flirted with JPY110.80, but now initial resistance is seen around JPY110.20.

The Australian dollar’s losses were extended to almost $0.7510, new lows for the year before finding a bid. Resistance is seen in the $0.7555-$0.7560 area, which holds the 200-day moving average. A close below the $0.7530 would be a poor omen for the start of next week.

After jumping nearly 0.8% against the Chinese yuan yesterday, the greenback slipped by almost 0.2% today. Still, it is the third consecutive week that it has risen against the yuan, and the 0.6% gain is the largest weekly advance since last September. Although officials insist on a two-way market, the PBOC set the dollar’s reference rate stronger than the models expected for the fourth consecutive session (CNY6.4361 vs. CNY6.4356).

Europe

The UK’s May retail sales disappointed. Economists had anticipated a 1.5% gain and 1.4% excluding gasoline. Instead, retail sales fell by 1.4% and 2.1%, respectively. Yet, the negativity should be tempered by the strong 9%+ increase in April. At the same time, the extension of social restrictions into the middle of next month warns the recovery may be a bit slower than anticipated a few weeks ago, as the UK experiences a surge in covid cases. The Bank of England meets next week. It announced a slowing of bond purchases at its last meeting, and although inflation is above the medium-term target, the BOE need not be in a hurry to slow the purchases further.

France goes to the polls this weekend for regional elections. It also about positioning ahead of next year’s presidential contest. A key issue is whether the political climate has changed sufficiently for Le Pen to draw support from the center-right. Some polls suggest her National Rally party may secure its first regional presidency. Meanwhile, in recent days, the EU’s former chief negotiator for Brexit, Barnier, and the Socialist mayor of Paris, Hidalgo, seems to be hinting at a run themselves. Still, the polls show no other potential candidate can break into the duopoly between Macron and Le Pen, both with a little more than 25% support. In the second round, Macron is running ahead of Le Pen by a smaller margin than in 2017.

After extending its losses to around $1.1885, the euro has been holding above the $1.1900-level in the European morning. The drop to two-month lows has seen many bulls pull in their horns amid ideas that the Fed’s dot plots represent a new phase for the dollar. Still, the euro moved three standard deviations from its 20-day moving average (remember Bollinger Bands at set at two standard deviations), illustrating the short-term over-extended condition. We note that the 10-year interest rate differential has narrowed this week, and the two-year differential is only a couple of basis points wider. Market positioning ahead of today’s triple-witching (expiration of futures and options) likely contributed to the exaggerated price action.

Sterling slid to $1.3855 today, which is also more than three standard deviations from its 20-day moving average. Congestion and a retracement objective of the rally since the late December low below $1.32 is found near $1.3840. A break of that could target the $1.3720 area. Sterling has recovered a bit in the European morning, and a move back above $1.3950 would help stabilize the tone.

America

The markets continue to digest the implications of the Fed’s new forecasts. The fact that the 10-year yield unwound the Fed-induced increase, while the shorter end held firm, encouraged talk of bullish curve flattening trades, as if the market, clamoring for the Fed to adjust its stance, quicky become worried that officials did too much. Yet besides acknowledging that the pace of Fed purchases is being discussed and some changes in near-term individual projections, the Fed did not really do anything. Moreover, the market, as we have noted, had priced in one hike by the end of next year (in the December 2022 Eurodollar futures) and have long expected a tapering announcement at either the Jackson Hole confab at the end of August or the September FOMC meeting, with a move effective late this year or early next year. Still, the later the tapering begins, the more likely it will continue to buy long-term assets after the ECB’s PEPP efforts end and the BOJ’s program extensions end (both now projected to end in March 2022).

The anticipation of better weather conditions and reports suggesting China’s swineherd has been rebuilt helped send grain and lean hog prices sharply lower. There is also uncertainty over the Biden administration’s biofuel policies. Soy, corn, and canola are used to produce biofuels, and prices tumbled. Soy is now flat on the year, and corn and canola futures were limit down yesterday. Lean hogs saw their biggest slide since late last year. Platinum, nickel, sugar, and lumber are also well off their previous highs. Copper prices rallied for the past seven sessions but are trading heavier today. Oil prices have pulled back but are still above $70 a barrel. The concern is that US demand is rising faster than output. Also, Iran votes today, and the risk is that the new government is not as enthusiastic about striking a deal to get the US back into the nuclear pact, without which most of its oil will stay off the market.

As part of its effort to prevent more disruption to the US money markets and to ensure that the Fed funds rate does not slip closer to the zero bound, the Federal Reserve increased the rate it pays on reserves to 15 bp and the rate offered on its reverse repo facility (from zero to five basis points). The reverse repo facility was attracting hundreds of billions of dollars every day, and Powell indicated that it was working as the Fed had imagined it would. So what happens when the Fed offers to pay users of this facility, which they were actively using? It does not seem surprising that the usage jumped to a new record high of $756 bln yesterday, surpassing the record set earlier the week near $584 bln.

The greenback is extending its gains against the Canadian dollar for the fourth consecutive session and is drawing near CAD1.2400. A break of this area would target the CAD1.2530 area, but the technical readings are extended, and the greenback is above its upper Bollinger Band for the third consecutive session. It was more than three standard deviations above the 20-day moving average yesterday. That mark comes in today near CAD1.2420. Support now is seen around CAD1.2340.

The Mexican peso has been hit hard this week as its interest rate advantage was undercut by the Fed and the central bank of Brazil, which hiked the Selic rate by 75 bp for the third time. It now stands 25 bp above Mexico’s target rate, and it has signaled another hike in August. At the same time that Mexico is looking to further secure the privileged place for Pemex, Brazil is moving closer to privatizing Electobras. The dollar is holding above the 200-day moving average against the Mexican peso (~MXN20.40). A move above MXN20.60 could signal a move toward MXN20.80-MXN20.85.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-06-21

Update June 21 2021: SNB intervening. Sight Deposits have risen by +1.1 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

FX Daily, June 16: Will the Fed Talk the Talk?

FX Daily, June 16: Will the Fed Talk the Talk?

2021-06-16

With the outcome of the FOMC meeting awaited, the dollar is narrowly mixed in quiet turnover. The Scandis are the weakest (~-0.3%) among the majors, while the Antipodeans are the strongest (~+0.25%). JP Morgan’s Emerging Market Currency Index is snapping a three-day decline

FX Daily, June 11: US Yields Stabilize After Falling to Three-Month Lows

FX Daily, June 11: US Yields Stabilize After Falling to Three-Month Lows

2021-06-11

The 10-year US Treasury yield steadied after reaching a three-month low near 1.43%, despite the US CPI rising more than expected to 5% year-over-year. On the week, the decline of around a dozen basis points would be the largest in a year. Australia, New Zealand, and Italy benchmark yields have seen a bigger decline this week.

FX Daily, June 02: The Dollar Snaps Back

FX Daily, June 02: The Dollar Snaps Back

2021-06-02

The US dollar is enjoying broad, even if not large, gains today following yesterday’s recovery from three-year lows against sterling and four-year lows against the Canadian dollar. The greenback is firmer against all the major currencies.

FX Daily, May 26: RBNZ Joins the Queue, while Yuan’s Advance Continues

FX Daily, May 26: RBNZ Joins the Queue, while Yuan’s Advance Continues

2021-05-26

The decline in US rates and the doves at the ECB pushing back against the need to reduce bond purchases next month have seen European bond yields unwind most of this month’s gain. The inability of US shares to hold on to early gains yesterday did not deter the Asia Pacific and European equities from trading higher.

FX Daily, May 18: Risk Appetites Return Bigly

FX Daily, May 18: Risk Appetites Return Bigly

2021-05-18

In Asia, equities markets rallied strongly, led by the more than 5% gain in Taiwan, the most in over a year as Monday’s 3% drop was more than overcome. The Nikkei gained more than 2% despite the deeper than expected contraction in Q1 GDP. Hong Kong, South Korea, and India also rose more than a 1% gain as tech came roaring back.

FX Daily, May 14: Softer Yields = Softer Dollar

FX Daily, May 14: Softer Yields = Softer Dollar

2021-05-14

The surge in consumer prices reported on Wednesday saw rates jump and the dollar push higher. Stronger than expected producer prices yesterday, and news of wage increases (average 10%) at Mcdonalds and for 75,000 people Amazon wants to hire, saw rates ease and the dollar’s upside momentum stall.

FX Daily, May 10: The Dollar Remains on the Defensive

FX Daily, May 10: The Dollar Remains on the Defensive

2021-05-10

Last week’s cyberattack on the largest US gasoline pipeline continues to lift oil and gasoline prices. The June gasoline futures gapped higher to extend last week’s 2.4% gain but has subsequently moved lower to enter the gap.

Tags: #USD,Bank of Japan,commodities,Currency Movement,Featured,federal-reserve,newsletter,U.K.