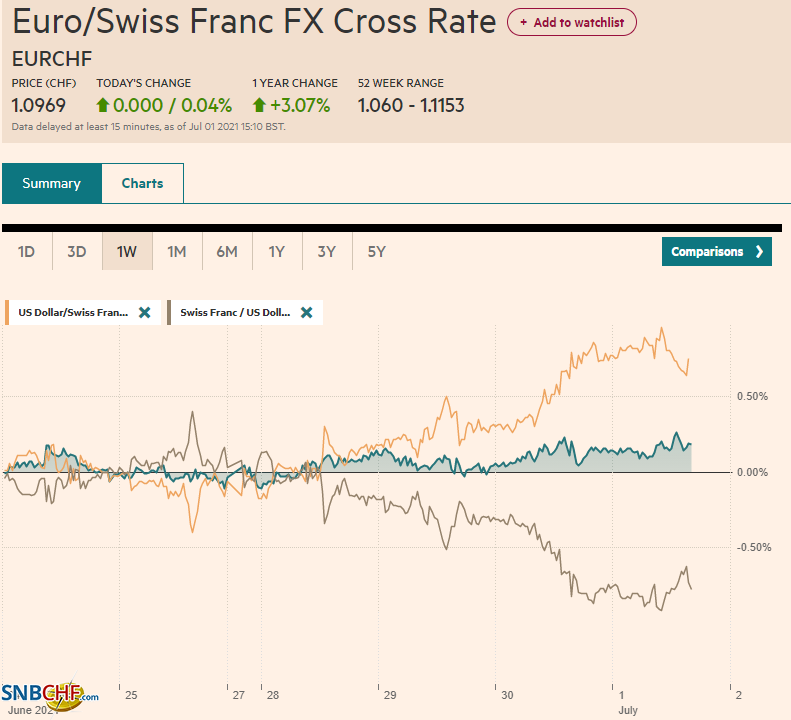

Swiss Franc The Euro has risen by 0.04% to 1.0969 EUR/CHF and USD/CHF, July 01(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Soft Asian manufacturing PMIs weighed on local shares after the S&P 500 set new record highs yesterday. European shares are recouping yesterday’s month-end losses, while US futures indices are bid. The US 10-year yield is around 1.47%, and European yields are 1-2 bp higher. The dollar is beginning the quarter on firm footing, making new highs for the year against the Japanese yen (~JPY111.60). The euro has been unable to resurface above .1860 and is at its lowest level in nearly three months. No change by the Riksbank left the krona vulnerable, and the krona’s 0.3% loss leads the

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Asia, Brazil, Currency Movement, Featured, newsletter, PMI, Sweden, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.04% to 1.0969 |

EUR/CHF and USD/CHF, July 01(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Soft Asian manufacturing PMIs weighed on local shares after the S&P 500 set new record highs yesterday. European shares are recouping yesterday’s month-end losses, while US futures indices are bid. The US 10-year yield is around 1.47%, and European yields are 1-2 bp higher. The dollar is beginning the quarter on firm footing, making new highs for the year against the Japanese yen (~JPY111.60). The euro has been unable to resurface above $1.1860 and is at its lowest level in nearly three months. No change by the Riksbank left the krona vulnerable, and the krona’s 0.3% loss leads the majors. Russia, Turkey, and South Africa are firmer, while many emerging market currencies are softer. The JP Morgan Emerging Market Currency Index has a four-day slide in tow. Gold extended its recovery from $1750 but ran into resistance in front of $1780. Oil prices are firm in the wake of the latest drawdown of US inventories. The August contract set new highs above $74.50 as the outcome of the OPEC meeting is awaited. Speculation has centered around an increase of 500k barrels next month. The CRB Index settled yesterday at its best level in nearly six years. With June’s gain of 3.75%, the index rose for the seventh month in the past eight. |

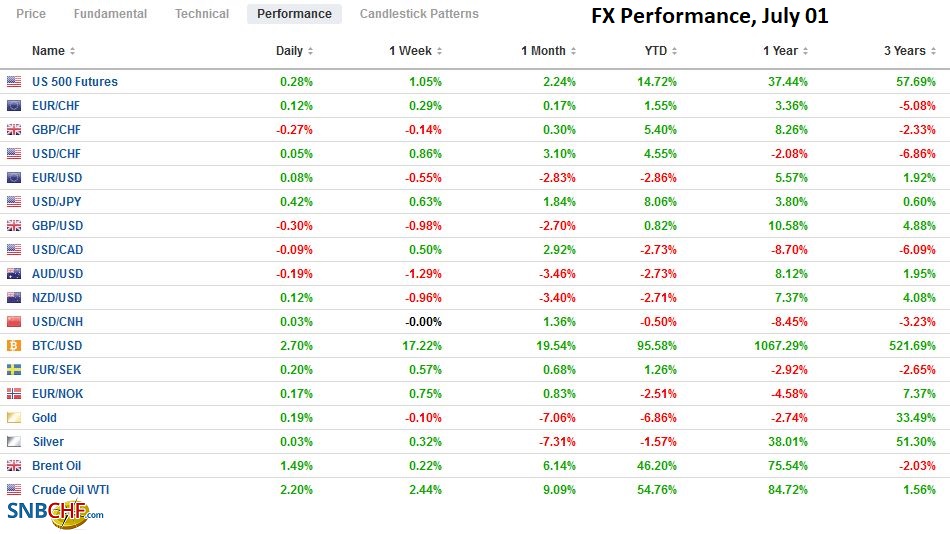

FX Performance, July 01 - Click to enlarge |

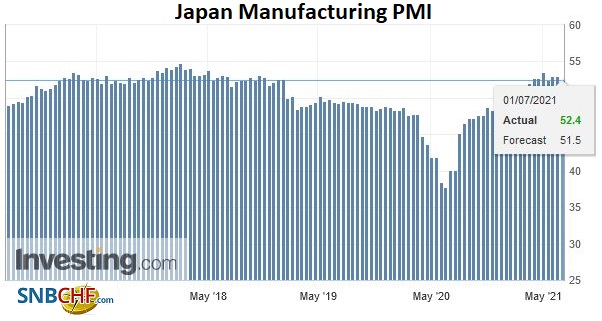

JapanJapan’s Tankan survey showed improvement in large and small businesses. The outlooks also were better. While the gains lagged expectations, the results are consistent with a stronger economy going forward. Also, of note, capex plans were one area that beat expectations. A 9.6% increase is expected now after a 3% increase in the Q1 survey and expectations for a 7.2% gain. Separately, the June manufacturing PMI was revised to show a small decline from May’s 53.0 reading than the 51.5 flash estimate. The final reading stands at 52.4. Recall that the decline from 53.6 in April to 53.0 in May coincided with a 5.9% slump in industrial output reported yesterday. |

Japan Manufacturing PMI, June 2021(see more posts on Japan Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

Asia Pacific

Australia’s preliminary June PMI estimate of 58.4 was revised to 58.6. It stood at 60.4 in May and was at 55.7 at the end of 2019. The May trade surplus was reported at A$9.7 bln, an improvement from April’s A$8.0 bln but less than the A$10.5 bln projected. Through May, the average monthly trade surplus was A$8.3 bln. This compares with an average of A$6.4 bln in the first five months last year and A$5.0 bln in 2019. Despite China’s use of trade to express its dissatisfaction with Canberra’s foreign policy, bilateral trade has risen by a little more than 6% this year. Iron ore and wheat exports reached record levels, and coal exports rose almost 10%, their highest (value) in a year.

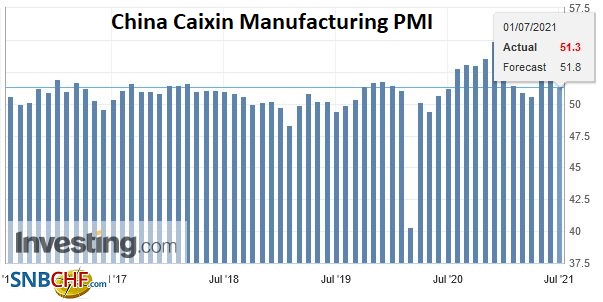

ChinaChina’s Caixin manufacturing PMI slipped to 51.3 from 52.0, which was a little weaker than expected. This reflects a regional pattern in Asia, spurring some talk that the peak in the recovery has passed. Social restrictions in Taiwan and Malaysia took a toll, and with the former falling to 57.6 from 62.0 and the latter contracting a slower rate (49.5 vs. 47.6). Indonesia’s PMI eased to 53.5 from 55.3. The Philippines and South Korea were more resilient, with the manufacturing PMI rising to 50.8 from 49.9, and edging higher to 53.9 from 53.7, respectively. Separately, South Korea reported a somewhat smaller than expected trade surplus of $4.44 bln, a sharp improvement from the $2.94 bln surplus seen in May. Exports slowed from 45.6% year-over-year to 39.7%. Imports accelerated to 40.7% year-over-year from 37.9%. |

China Caixin Manufacturing PMI, June 2021(see more posts on China Caixin Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

The dollar posted a big outside up day against the yen yesterday by trading on both sides of Tuesday’s range and closing above its high. Follow-through buying has lifted the greenback to around JPY111.60 to draw closer to the high from March 2020 near JPY111.70. The JPY111.00-level holds an expiring option today (~$575 mln) and tomorrow (~$1.9 bln). More interesting may be the option for $1.1 bln at JPY111.75 that expires tomorrow.

The Australian dollar is slipping for the fourth consecutive session. Recall that it rose in all five sessions last week. It has returned to the low for the year set last month, near $0.7475. A convincing break could signal a test on $0.7400. Resistance is seen at $0.7500, where a A$500 mln option expires today.

The greenback has edged higher against the Chinese yuan to about CNY6.4690, the upper end of this week’s narrow range. The lower end of the range is around CNY6.4535. The PBOC set the dollar’s reference rate at CNY6.4709, a little larger of a positive dollar deviation from the median bank model (CNY6.4692) in Bloomberg’s survey than seen in recent days.

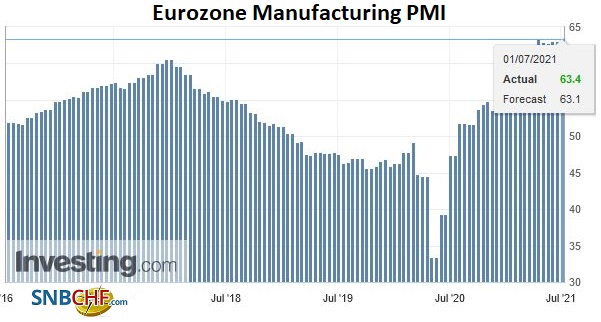

EurozoneThe manufacturing PMI for the eurozone was revised to 63.4 in the final reading from 63.1 of the flash report that had been unchanged from May. Germany’s was revised to 65.1 from the 64.9 preliminary estimate and 64.4 in May. The French reading was revised up to 59.0 from 58.6, which pared the loss from May’s 59.4. Spain’s manufacturing PMI beat expectations to rise to 60.4 from 59.4. Italy’s showed a slight decline to a still-high 62.2 from 62.3. Separately, Italy reported an unexpected decline in unemployment in May to 10.5% from 10.7%. |

Eurozone Manufacturing PMI, June 2021(see more posts on Eurozone Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

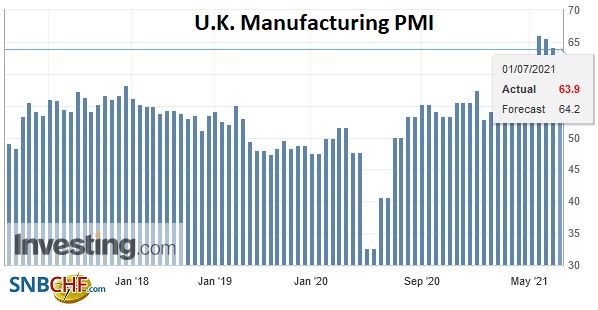

United KingdomThe UK’s manufacturing PMI showed a deeper pullback than the preliminary estimate, but at 63.9, it can hardly be considered weak. Initially, it was estimated to be 64.2, down from 65.6 in May. Separately, the EU granted the UK a three-month longer grace period for checking chilled meat shipments to Northern Ireland until the end of September. While the extension may ease the immediate strain, the problem is unlikely to be resolved. The border check between Northern Ireland and the rest of Britain, the arrangement that the UK insisted on, is untenable from a political and economic vantage point. |

U.K. Manufacturing PMI, June 2021(see more posts on U.K. Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

Sweden’s Riksbank stood pat but failed to change its projected path of policy rates, which remained flat through Q3 2024. It boosted its growth forecast and now sees the economy expanding 4.2% this year. In April, it had projected 3.7% growth. Inflation is expected to average 1.2% this year and rise toward 1.7% in 2024. It maintained the pace of bond buying and anticipates buying almost SEK69 bln in Q4 to exhaust the SEK700 bln envelop by the end of the year. The Riksbank stance offers a stark contrast with Norway, where the Norges Bank has indicated it will hike rates as early as September. Separately, Sweden continues to struggle to find a governing coalition from the existing parliament following the recent collapse of the government.

The euro made a marginal new two-month low slightly below $1.1840 today. It has stabilized in the European morning. A move above $1.1860-$1.1880 would help the technical tone, but a move back above $1.19 may be needed to suggest a low is in place. There is an option for 2 bln euros at $1.1850 that expires tomorrow.

Sterling is heavier and has not stabilized, making new lows in late morning turnover in London. It has been sold to almost $1.3770, its lowest level in mid-April. The intraday momentum studies are over-extended, and a better tone may emerge in North American dealings. The $1.3800 area offers the initial cap now, and a move above $1.3840 would help the tone.

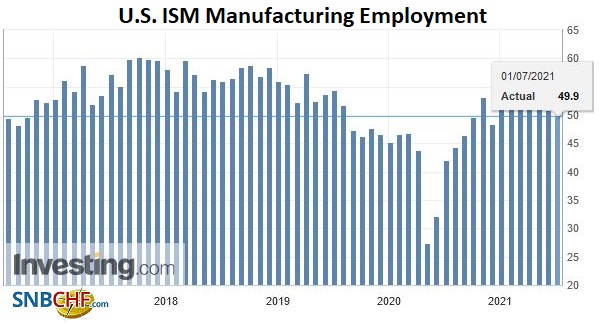

United StatesThe focus is on the US labor market ahead of tomorrow’s June national figures. Yesterday’s ADP estimate of 692k private-sector jobs growth beat expectations but was marred by an almost 100k downward revision in the May estimate (886k vs. 978k). Today sees the Challenger Job cuts and the weekly initial jobless claims. Even if the weekly jobless slip to 388k from 411k as the median forecast in Bloomberg’s survey had it, it would keep the four-week moving average unchanged after falling last week for the first time since April. |

U.S. ISM Manufacturing Employment, June 2021(see more posts on U.S. ISM Manufacturing Employment, ) Source: Investing.com - Click to enlarge |

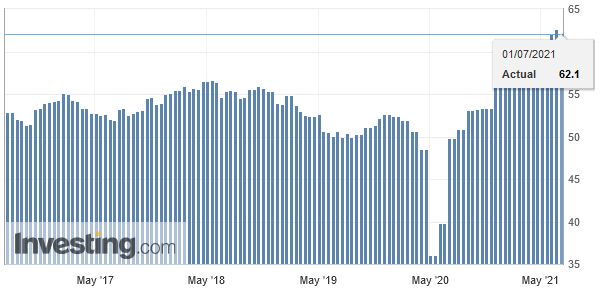

| Separately, the final manufacturing PMI and ISM manufacturing survey will be released. Rather than the headline, the market may be more sensitive to the prices paid sub-index, which may have fallen for the second consecutive month. US auto sales will trickle in over the course of the session. Projections have gradually eroded and now, according to Bloomberg’s survey, have fallen to a 16.5 mln seasonally adjusted annual pace, down from almost 17 mln in May, which itself less than the lofty 18.5 mln rate seen in April. |

U.S. Manufacturing PMI, June 2021(see more posts on U.S. Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

Canada’s economic diary is light today, ahead of tomorrow’s May trade figures and the manufacturing PMI. Yesterday, Canada reported a smaller than expected contraction in April (-0.3% vs. -0.8% projected), and March’s GDP was revised higher to 1.3% from 1.1%. Canada reports its June employment data on July 9, a few days ahead of the next central bank meeting.

Mexico reports May worker remittances. The importance of these may not be fully appreciated. They are a more important source of hard currency (dollars) than the trade surplus. Through April, they have averaged almost $3.7 bln a month. In 2020, the average was nearly $3.4 bln, and in 2019 they averaged a little more than $3 bln. Through May, the trade surplus averaged $66.5 mln a month. The surplus averaged $2.8 bln a month in 2020 and a little less than $500 mln a month in 2019. Mexico will also report the Markit manufacturing PMI and the IMEF surveys for manufacturing and non-manufacturing sectors. Brazil sees the manufacturing PMI and June trade figures. Brazil’s trade surplus has averaged $5.4 bln a month through May. The monthly average was $4.2 bln last year and $2.9 bln in 2019.

The US dollar continues to hover around CAD1.24. A two-month high was set on June 21 near CAD1.2490. A downtrend line connecting the January, April, and June highs are found today around CAD1.2465. There is an option for $320 mln at CAD1.2475 that expires today. Support may be found in the CAD1.2330-CAD1.2350 area.

The dollar broke out of the consolidative triangle pattern yesterday to the upside and is edging a bit higher today to approach MXN20.00. A move above MXN20.02 can see MXN20.10. Stronger resistance may be encountered in the MXN20.20-MXN20.22 area. The greenback pushed above BRL5.0 yesterday for the first time since June 22 but settled below, as Brazil remains one of the favorites of bond fund managers. The real rose 5% last month, the largest advance of major and emerging market currencies. It was off about 0.4% for the year through May and is now the top performer year-to-date.

You Might Also Like

FX Daily, June 29: Fear that the Mutating Virus Could Slow Recoveries Takes a Toll on Risk Appetites Ahead of Quarter-End

FX Daily, June 29: Fear that the Mutating Virus Could Slow Recoveries Takes a Toll on Risk Appetites Ahead of Quarter-End

2021-06-29

Fear that the new mutation of the covid virus will slow the global recovery has sent ripples across the global capital markets. The foreign exchange market has the clearest reaction, and the dollar is bid.

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-06-28

Update June 28 2021: SNB intervening. Sight Deposits have risen by +0.4 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

FX Daily, June 17: Fed Rocks the World

FX Daily, June 17: Fed Rocks the World

2021-06-17

A more hawkish than expected Federal Reserve sent the US dollar and interest rates higher and spurred an equity sell-off. The knock-on effect sent ripples through the capital markets today. Most equity markets in the Asia Pacific region fell. China, Hong Kong, and Taiwan were notable exceptions.

FX Daily, June 09: Without Yield Support, the Dollar Wilts

FX Daily, June 09: Without Yield Support, the Dollar Wilts

2021-06-09

Falling US yields weigh on the US dollar. The 10-year Treasury yield is flirting with the 1.50% mark, and the greenback is trading heavily against all the major and most emerging market currencies. European and the Asia Pacific benchmark yields are lower as well.

FX Daily, May 12: The Dollar Stabilizes but Stocks, Not So Much

FX Daily, May 12: The Dollar Stabilizes but Stocks, Not So Much

2021-05-12

The markets remain on edge. Asia Pacific and US equities have yet to find stable footing, and inflation fears are elevated. The foreign exchange market has turned quiet as the dollar consolidates its recent losses.

FX Daily, March 15: Big Week Begins Quietly

FX Daily, March 15: Big Week Begins Quietly

2021-03-15

The capital markets are beginning a new and busy week in a non-committal fashion. Equities are mixed. Except for Japan, Hong Kong, and Australia, most markets in the Asia Pacific region were lower, led Chinese and Indian shares.

FX Daily, February 19: Equities Stabilizing While the Greenback Remains Under Pressure

FX Daily, February 19: Equities Stabilizing While the Greenback Remains Under Pressure

2021-02-19

Overview: The bond and equity markets are trying to stabilize ahead of the weekend. The dollar remains under pressure. In the Asia Pacific region, Hong Kong, China, and South Korean markets advanced, but most markets could not overcome the profit-taking pressures.

FX Daily, January 19: Even When She Speaks Softly, She’s Yellen

FX Daily, January 19: Even When She Speaks Softly, She’s Yellen

2021-01-19

Overview: The animal spirits are on the march today. Equities are mostly higher, peripheral European bonds are firm, and the dollar is mostly softer. After posting the first back-to-back decline this year, the MSCI Asia Pacific Index bounced back today, led by a 2.7% gain in Hong Kong (20-month high) and a 2.6% rise in South Korea’s Kospi.

Tags: #USD,Asia,Brazil,Currency Movement,Featured,newsletter,PMI,Sweden