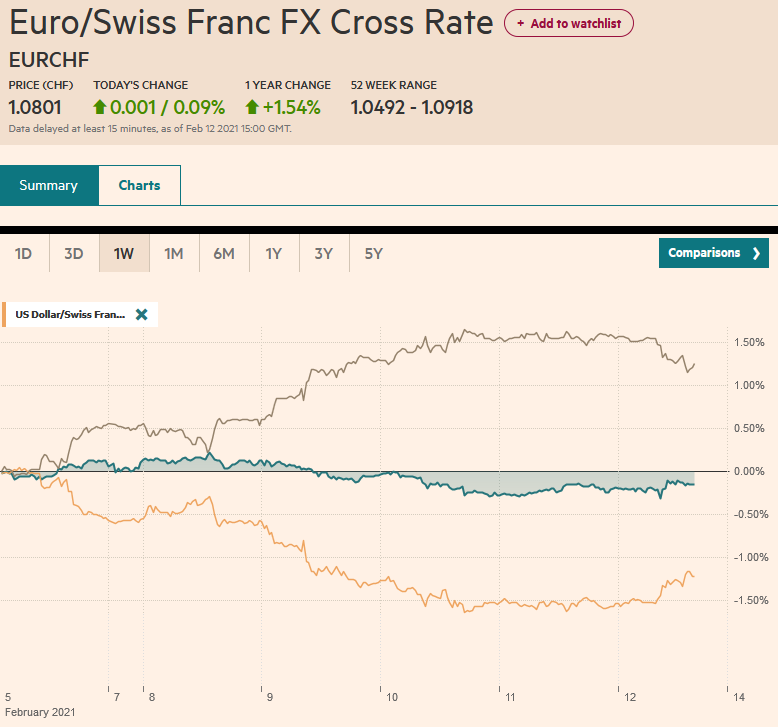

Swiss Franc The Euro has risen by 0.06% to 1.0801 EUR/CHF and USD/CHF, February 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Profit-taking weighs on equity markets, and the dollar is trading higher ahead of the weekend. Most Asia Pacific markets are still closed for the holiday, but Victoria’s snap lockdown dragged Australian shares lower. Japan and Indian markets were narrowly mixed, but the selling pressure is clearer in Europe, where the Dow Jones Stoxx 600 has had a heavier bias. US shares are also trading off, though coming into today, the S&P 500 was up about 0.75% for the week. US markets are closed on Monday. The dollar is snapping back after key levels held (.2150 in the euro and JPY104.40).

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Currency Movement, Featured, Italy, Mexico, newsletter, Olympics, U.K., USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.06% to 1.0801 |

EUR/CHF and USD/CHF, February 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Profit-taking weighs on equity markets, and the dollar is trading higher ahead of the weekend. Most Asia Pacific markets are still closed for the holiday, but Victoria’s snap lockdown dragged Australian shares lower. Japan and Indian markets were narrowly mixed, but the selling pressure is clearer in Europe, where the Dow Jones Stoxx 600 has had a heavier bias. US shares are also trading off, though coming into today, the S&P 500 was up about 0.75% for the week. US markets are closed on Monday. The dollar is snapping back after key levels held ($1.2150 in the euro and JPY104.40). The JP Morgan Emerging Market Currency Index is snapping a five-day advance but is likely to finish the week higher for only the second time this year. Gold continues to retreat after being turned by the 200-day moving average (~$1855.50) in the middle of the week. It is closer now to the low set at the start of the week, a little below $1808. Oil prices ended an eight-day rally yesterday and are seeing follow-through selling today. March WTI peaked on Wednesday shy of $59 and is pushing below $57.50 today. A break of $57 could spur a move toward $55 in the coming days. |

FX Performance, February 12 - Click to enlarge |

Asia Pacific

In an unscientific sampling of the covering of China’s decision to pull the BBC broadcasts, most seem to see it as yet another example of censorship. Beijing appears to have stepped up its harassment of the foreign press, which includes arresting reporters and denying others credentials. Few understand it as retaliation for the UK’s decision to stop China’s state-owned broadcaster CGTN broadcasts over licensing issues. As CGTN sought to correct the situation (transfer license to another company, the UK rejected it due to missing information. The UK poked a bully and feigns surprise when the bully strikes back. Separately, it is revealing that Hong Kong has also denied the BBC access to its public network. It is another sign of the Sino-ificiation of Hong Kong.

As tipped, the head of Tokyo’s Olympic Committee, former Prime Minister Mori, has resigned over insulting comments about women that triggered an uproar in Japan, which itself is noteworthy. The immediate problem is not resolved, as a leading candidate, senior in age to Mori, and a former soccer star turned down the position. The pandemic is only one of a series of challenges for the Tokyo Olympics. There was a bribery scandal over Tokyo’s bid itself. There were accusations that the logo was copied and a reversal on a stadium’s design. There are safety concerns as some events are planned in the Fukushima prefecture, where the nuclear disaster happened. Public support for the Olympics has fallen below 20% in a recent poll. His handling of the Mori incident and the Olympics has not helped Prime Minister Suga, whose support is also falling. An election needs to be held by late October.

The dollar held support near JPY104.40 in the middle of the week and has jumped back to test the JPY105.20 area in late Asian turnover. There are $3.8 bln in options struck between JPY104.85 and JPY105.00 that are expiring today and another $470 mln at JPY105.35. We suspect the upside may have limited ahead of the weekend and peg support in the JPY104.70-JPY104.80 area. Although most of our levels worked out well this week, the Australian dollar overshot a little, poking briefly through the $0.7770-area yesterday. It has come back lower today, and a break of $0.7700 lend credence to the idea that the bounce was part of the “correction within a correction) and lower levels should be expected. The dollar is enjoying a firm tone against the offshore yuan, but it is off about 0.4% on the week.

Europe

The UK economy grew by 1.2% in December, which was a bit better than expected, and follows a revised 2.3% contraction in November (from -2.6%). It translated into a 1.0% expansion in Q420, twice the median forecast in Bloomberg’s survey. Government spending provided the important impetus, jumping 6.4%. In December, industrial output (0.2%), manufacturing (0.3%), and construction (-2.9%) were weaker than anticipated. The trade deficit was larger (-GBP6.2 bln). Services were a bright spot (1.7%). Although the BOE’s Haldane was nearly euphoric, talking about how the economy will snap back like a spring and inflation will return to target next year, the key remains the evolution of the virus. There is talk of extended curb through the summer.

Italy’s benchmark 10-year bond yield has fallen to new record lows today and is approaching 40 bp. While ECB buying is, of course, a factor, recent flow data suggest it is not the only one as Japanese investors have also been keen. With yesterday’s vote by the Five Star Movement, almost 60% supported a Draghi government, the stage is set. Draghi did not need the M5S as a majority had already been secured, but it is helpful, and even the founder, Grillo, endorsed Draghi. The promise to set up an ecological transition ministry helped galvanize support. The next step is for Draghi to announce his cabinet and next week submit to a vote of confidence in both chambers.

The euro stopped 1/100 of a cent from our $1.2150 target yesterday and has backed off today. It has tested the $1.2100 area, which houses the 20-day moving average. A break of it could send it down another quarter of a cent or so today. The $1.2025-$1.2050 area may be the key early next week. Sterling held about $1.38 for the past two sessions, but not today. The expiring option for about GBP360 mln struck there is now out of the money after slipping to almost $1.3775. Support is seen closer to $1.3750.

America

There is a light economic calendar for North America ahead of the weekend. Of note, both Yellen and Powell will attend the first G7 virtual meeting of the year. There may be some headline risk around it. This week the market easily absorbed the US quarterly refunding, where it sold about $125 bln of coupons. The 10-year yield rose almost 10 bp, illustrative of the concession built, and this week it is off a basis point. The US 2-year yield slipped below 10 bp yesterday for the first time. As the Treasury pays down a significant amount of T-bills and reduces its cash balance, the short-end of the curve is very soft. There is still fear that some bills could fall to zero or below, and it has spurred a debate whether the Fed will tweak some of its tools, like interest on reserves (required and excess) or reverse repo rates.

Mexico delivered the widely expected 25 bp rate cut yesterday, and several factors will encourage the market to look for more cuts. First, the decision was unanimous. Second, there was no mention of a floor for rates or talk of limited scope for additional moves. Banixco sees core inflation back at 3% in Q3 and warns of base effect’s distortions that could lift reading in Q2 only to see them unwind in Q3. The central bank meets next on March 25. Speculation will mount for another cut then.

For the past two sessions, the US dollar fell against the Canadian dollar initially but recovered to close near session highs, as if the market was rejecting those lower levels. The greenback has bounced from around CAD1.2660 yesterday to about CAD1.2755 today, where it settled last week. Chart resistance is seen near CAD1.2775-CAD1.2800. Softer equities and a pullback in oil may weigh on the Canadian dollar. The greenback saw almost MXN19.90 yesterday but is snapping back today and has already risen above Thursday’s high (~MXN20.0575). There may be potential for MXN20.15 today. It finished last week around MXN20.0875.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

2021-02-08

Update February 8 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -0.3 bn. compared to last week, this means the SNB is selling euros and dollars.

FX Daily, February 05: Position Squaring Weighs on the Dollar Ahead of the Jobs Report

FX Daily, February 05: Position Squaring Weighs on the Dollar Ahead of the Jobs Report

2021-02-05

Overview: While equities continue to march higher, the dollar is softer amid position squaring ahead of the US jobs data. Gold has stabilized after yesterday’s shellacking. Estimates for US nonfarm payrolls appear to have been creeping higher, encouraged by the ADP, PMI, and weekly initial jobless claims.

2021-01-15

The US dollar is firm against most of the major and emerging market currencies today. Among the majors, the Japanese yen and Swiss franc are resilient. For the week, sterling and the yen appear poised to eke out small gains, while the Scandi’s are the weakest performers with around a 1% decline.

FX Daily, November 25: Risk Appetites Stall Ahead of the US Thanksgiving Holiday

FX Daily, November 25: Risk Appetites Stall Ahead of the US Thanksgiving Holiday

2020-11-25

The global equity rally appears to be stalling after the US markets rallied strongly yesterday. Chinese, Taiwan, Korean, and Indian indices fell, and the MSCI Asia Pacific Index appears to have posted only its second loss this month. European shares are narrowly mixed, leaving the Dow Jones Stoxx 600 little changed.

FX Daily, November 13: Greenback Pares this Week’s Gains while the Turkish Lira Continues to Squeeze Higher

FX Daily, November 13: Greenback Pares this Week’s Gains while the Turkish Lira Continues to Squeeze Higher

2020-11-13

Overview: The largest bourses in the Asia Pacific region followed the US equity market lower, with the Nikkei posting its first loss in nine sessions. China, Hong Kong, and Australia moved lower as well. On the week, the MSCI Asia Pacific Index gained about 1% after rising 6.3% in the prior week.

FX Daily, November 12: Nervous Calm in the Capital Markets

FX Daily, November 12: Nervous Calm in the Capital Markets

2020-11-12

There is a nervous calm in the capital markets today. The equity rally in the Asia Pacific region stalled to end an eight-day rally, though the Nikkei’s rally remains intact.

FX Daily, October 9: Animal Spirits Return

FX Daily, October 9: Animal Spirits Return

2020-10-09

Overview: The on-again-off-again fiscal stimulus in the US is back on as the White House now supports a broad stimulus program, but not as big as the Democrats $2.2 trillion package. It is the narrative being cited as the rebuilding of risk appetites is the wobble earlier in the week.

FX Daily, October 1: Hope Springs Eternal

FX Daily, October 1: Hope Springs Eternal

2020-10-01

Speculation that a new round of fiscal stimulus from the US is possible is encouraging risk-taking today. Many large Asian centers were closed for holidays today, and a technical problem prevented the Tokyo Stock Exchange from opening.

Tags: #USD,Currency Movement,Featured,Italy,Mexico,newsletter,Olympics,U.K.