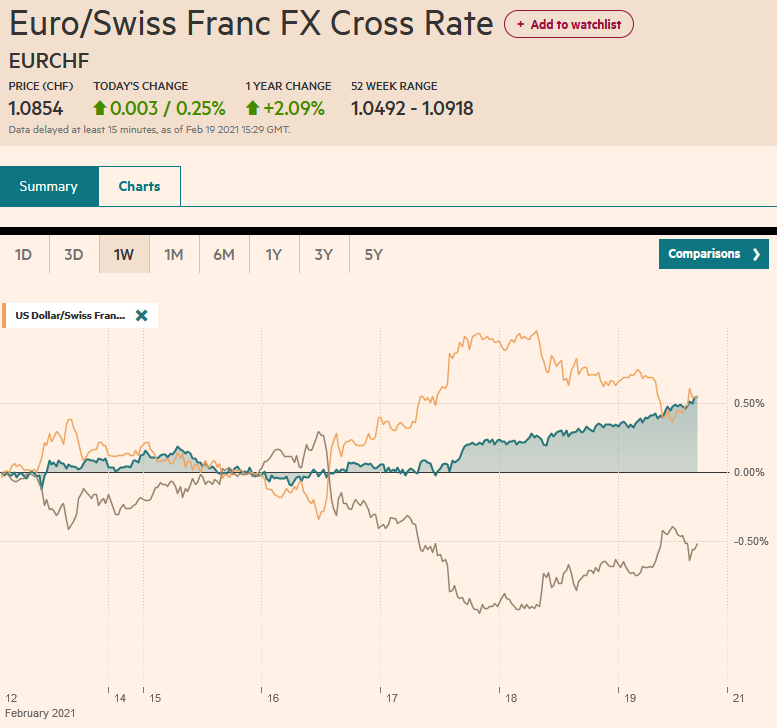

Swiss Franc The Euro has risen by 0.25% to 1.0854 EUR/CHF and USD/CHF, February 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The bond and equity markets are trying to stabilize ahead of the weekend. The dollar remains under pressure. In the Asia Pacific region, Hong Kong, China, and South Korean markets advanced, but most markets could not overcome the profit-taking pressures. Europe’s Dow Jones Stoxx 600 is faring better as it tries to snap a three-day decline. It is nearly flat on the week. US shares are trading firmer after yesterday’s afternoon recovery that pared earlier declines. The S&P 500 begins today off 0.5% for the week. The US 10-year yield is firm at 1.30%, up almost 10 bp this week.

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Currency Movement, Featured, newsletter, PMI, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.25% to 1.0854 |

EUR/CHF and USD/CHF, February 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The bond and equity markets are trying to stabilize ahead of the weekend. The dollar remains under pressure. In the Asia Pacific region, Hong Kong, China, and South Korean markets advanced, but most markets could not overcome the profit-taking pressures. Europe’s Dow Jones Stoxx 600 is faring better as it tries to snap a three-day decline. It is nearly flat on the week. US shares are trading firmer after yesterday’s afternoon recovery that pared earlier declines. The S&P 500 begins today off 0.5% for the week. The US 10-year yield is firm at 1.30%, up almost 10 bp this week. European yields are mostly 1-3 bp higher. Italy’s 10-year yield is flat to softer today, but it is up nearly 12 bp on the week, compared with 5-8 bp for the core markets. The Australian and New Zealand dollar are leading today’s advance against the greenback. Sterling traded above $1.40, but it is the weakest performer today, rising about 0.2% (~$1.4000) near midday in Europe. This week, only the Swiss franc and the Japanese yen among the majors have softened against the dollar (~0.2% and 0.4%, respectively). Most emerging market currencies are firm today. For the week, the Brazilian real (~-1.0%) and the Mexican peso (-2%) are the weakest performers, while the Chilean peso (~1.35%) is the strongest. Gold fell to about $1760, its lowest level since last July, before stabilizing. If it cannot sustain a move above $1775 today, it will be the seventh consecutive decline. News that the US is open to multilateral talks with Iran may have weighed on oil prices, even though the lifting of sanctions is still some ways off. April WTI traded near $62.30 yesterday and today’s low was near $58.60. It rebounded to around $59.60, a little above last week’s close, a touch beneath $59.40 |

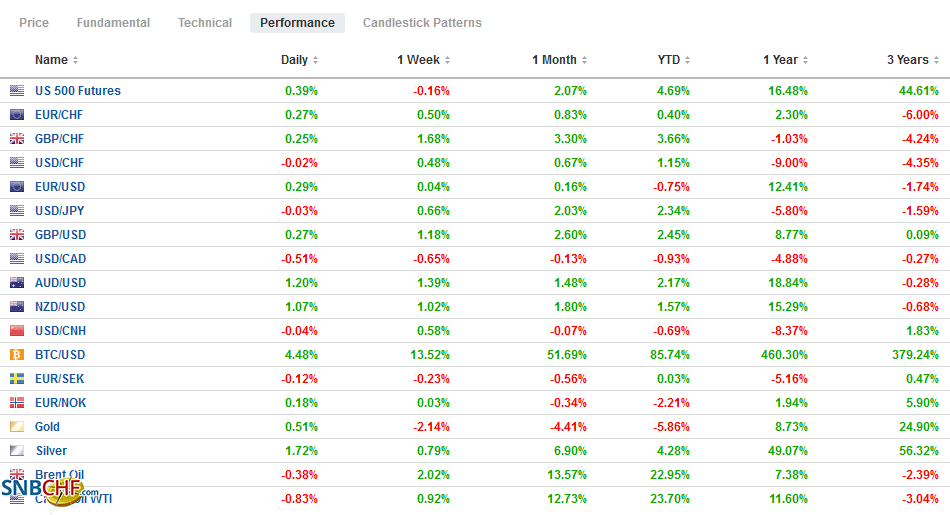

FX Performance, February 19 - Click to enlarge |

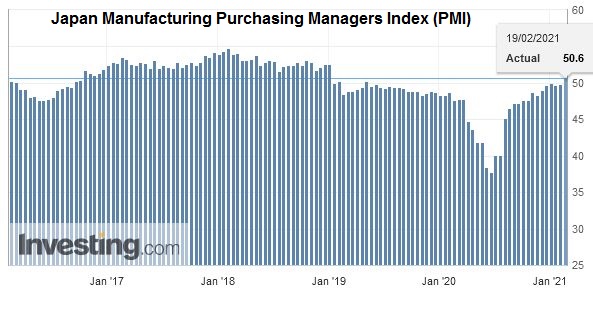

Asia PacificThere were two reports from Japan, January inflation and February preliminary PMI. At minus 0.6%, both the headline and core rate (excludes fresh food) were in line with expectations and showed an improvement from December. The less deflation reading was aided by the suspension of the government’s travel discounts. Excluding fresh food and energy, Japan’s CPI rose to 0.1% from minus 0.4%. It is the highest reading since last July. Separately, Japan’s manufacturing PMI jumped to 50.6 from 49.8, its best reading since late 2018. However, the services PMI worsened, falling to 45.8 from 46.1. The composite edged up to 47.6 from 47.1 |

Japan Manufacturing Purchasing Managers Index (PMI), February 2021(see more posts on Japan Manufacturing Purchasing Managers Index, ) Source: investing.com - Click to enlarge |

Australian data disappointed, but it too did not hold the Australian dollar back. It made a new high since March 2018 (~$0.7740). January retail sales, which economists expected a 2.0% rise, increased by only 0.6%, and the preliminary PMI softened. Manufacturing slipped to 56.6 from 57.2, and services dropped to 54.1 from 55.6. The result was the composite stands at 54.4, down from 55.9.

The dollar ended a four-day advance against the yen on Tuesday near JPY106.20. It is falling for the third session today and reached nearly JPY105.30, which is about the halfway mark of the rally that began on February 10th near JPY104.40. There are $1.2 bln in options in the JPY105.40-JPY105.50 area that expire today. The next retracement target is near JPY105.10. The Australian dollar punched through the $0.7800 area and reached nearly $0.7740. There appears to be little chart resistance now ahead of the $0.8000 area. It is the third consecutive weekly advance. The dollar rose about 0.45% yesterday against the Chinese yuan and is giving it all back today. The PBOC set the dollar’s reference rate at CNY6.4624, a bit weaker than expected (~CNY6.4656). That gap appears to be the largest in a few months.

Europe

The pattern in the eurozone preliminary PMI is for stronger manufacturing and weaker services. The German manufacturing PMI jumped to 60.6 (from 57.1), which is the highest since February 2018. The service PMI slipped to 45.9 from 46.7 and was weaker than expected. The composite edged up to 51.3 from 50.8. France’s preliminary manufacturing PMI rose to 55.0 from 51.6, which is also the highest since February 2018. Services slumped further (43.6 from 47.3), which dragged the composite to 45.2 from 47.7. The aggregate manufacturing for the eurozone rose to 57.7 from 54.8, while the services PMI fell to 44.7 from 45.4. The composite edged up to 48.1 from 47.8. Even if confirmed by the final reading, the report may not be sufficient to prevent the ECB staff from revising down their near-term forecasts at next month’s meeting (March 11).

The UK’s economic data were mixed: simply horrendous January retail and better than expected preliminary PMI. Retail sales plummeted by 8.2% in January, more than twice the decline economists expected and even worse if gasoline were excluded (-8.8%). Separately, estimates suggest that 20% of the Oxford Street shops will be permanently shut. The lockdowns took a toll. On the other hand, the manufacturing PMI rose to 54.9 from 54.1. Economists had warned of a decline. The services PMI rose to 49.7 from 39.5, while the composite rose to 49.8 from 41.2.

The euro is firm, extending its recovery off the $1.2020 area approached at midweek. It has recovered back to almost $1.2150. The high for the week was closer to $1.2170. The $1.2200 area marks the (61.8%) retracement of the decline from $1.2350 on January 6. Sterling is closing in on its sixth consecutive weekly advance. Since the end of last October, it has fallen in only two weeks and has rallied more than 10 cents during this run. Initial support now is seen near $1.3950. The next notable chart point is the 2018 double high, around $1.4345-$1.4375.

America

The US appears on a diplomatic offensive. The Biden administration is making itself available to multilateral talks with Iran and pulled away from Trump’s efforts to get the UN to reimpose sanctions. Iran’s rhetoric insists on the US lifting its sanctions before talks, but this does not look realistic. Separately, the State Department’s report on Nord Stream 2 sanctions is due today, but it may not be ready. Still, the signal is that rather than antagonize Germany, the US sanctions may be applied to a few Russian entities. Lastly, the G7 call today allows the Biden administration to continue its multilateral charm offensive.

Economists expect the US preliminary February PMI to soften a little but remains at elevated levels. Some suggested doubts about the US recovery, after weekly jobless claims rose to a four-week high last week, housing starts were weaker than expected, and the February Philadelphia Fed eased. Be skeptical. Housing starts remain at elevated levels, and poor weather needs to be taken into account. More importantly, the leading indicator, permits, surged by 10.4%. The decline in the Philly Fed survey was minor, and at 23.1, it remains above the three- and six-month average (~19.6). While Europe and Japan appear to be contracting here in Q1, the US is expanding. The real signal is being generated by the fiscal stimulus that has already begun being felt. Fed speakers include Barkin and Rosengren. Their views are known and overshadowed by next week’s congressional testimony by Powell and speeches by several governors. Separately, Canada reports December retail sales. They are too dated to be of much interest, but the weakness expected (~-2.6%) may pose some headline risk.

The US dollar is trading heavily against the Canadian dollar and looks poised to re-test the CAD1.26 level that held earlier this week. Recall that last month, the greenback recorded a low near CAD1.2590. A convincing break of CAD1.26 signals a test on the CAD1.25 area, which may offer stronger support. It may require a move back above CAD1.2700-CAD1.2725 to stabilize the US dollar’s technical tone. Meanwhile, the US dollar appears to have entered a new and higher range against the Mexican peso. The lower end of the recent range is in the MXN19.90 area, and the upper end of the range is around MXN20.50. It has covered the range this week. The dollar is trading firmer today, which, if sustained, would mean the greenback rose every session this week for the first time since last April.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

2021-02-15

Update February 15 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -0.1 bn. compared to last week, this means the SNB is selling euros and dollars.

FX Daily, February 3: The Greenback Remains Resilient as the Bulls Drive Equities Higher

FX Daily, February 3: The Greenback Remains Resilient as the Bulls Drive Equities Higher

2021-02-03

Equities have charged higher, and the greenback is mostly firmer. News that Draghi may become Italy’s next Prime Minister has boosted Italian bonds. The PBOC unexpectedly drained liquidity, and this may have deterred buying of Chinese stocks, a notable exception in the regional rally.

FX Daily, February 1: Markets Snap Back

FX Daily, February 1: Markets Snap Back

2021-02-01

Global equities are snapping back today, while the greenback retained the strength seen last week that was attributed to safe-haven flows. The MSCI Asia Pacific Index snapped a four-day decline led by Hong Kong, South Korea, India, and Indonesia.

FX Daily, January 6: High Drama Weighs on the Greenback and Lifts Yields

FX Daily, January 6: High Drama Weighs on the Greenback and Lifts Yields

2021-01-06

Overview: One of the two Georgia Senate contests remains too close to call, but the market appears to be pricing in a Democrat sweep. The 10-year yield has punched above 1% but has offered the greenback little support. Yesterday, the dollar-bloc currencies rose to highs since early Q2 2018 and are extending those gains today.

FX Daily, January 04: Rising Equities and Slumping Dollar Greet the New Year

FX Daily, January 04: Rising Equities and Slumping Dollar Greet the New Year

2021-01-04

Overview: The first day of the New Year, but it feels a lot like last year. The dollar is under pressure, and equities are higher. Outside of Japan and Malaysia, The MSCI Asia Pacific Index extended last week’s 3.6% gain. It has not rallied for seven consecutive sessions.

FX Daily, November 4: Indecision Keeps Investors on Edge, but the Dollar Rides High

FX Daily, November 4: Indecision Keeps Investors on Edge, but the Dollar Rides High

2020-11-04

Initially, the markets built on Tuesday’s price action, but as soon as a few counties in Florida indicated that it was not going to be the "blue wave," risk came off, and it was most evident in the bond and currency markets. Equities rallied in the Asia Pacific area, and all but Hong Kong, Australia, and Indonesia advanced.

FX Daily, October 05: Monday’s Dollar Blues

FX Daily, October 05: Monday’s Dollar Blues

2020-10-05

New actions to contain the virus are being taken in the US and Europe, but investors are looking past it and taking equities and risk assets, in general, higher to start the new week. MSCI Asia Pacific recouped most of last week’s 0.7% loss with gains of move than 1% in Japan, Hong Kong, South Korea, and Australia.

FX Daily, September 23: Trying to Find Solid Ground

FX Daily, September 23: Trying to Find Solid Ground

2020-09-23

A more stable tone is evident in the capital markets after the S&P 500, and NASDAQ rose more than one percent yesterday. Japan returned from a two-day holiday, and local shares slipped fractionally, while China, Hong Kong, South Korea, and Australian shares rallied. India and Taiwan fell.

Tags: #USD,Currency Movement,Featured,newsletter,PMI