The ECB meets tomorrow and is widely expected to stand pat. Macro forecasts may be tweaked modestly and there are some risks of jawboning against the stronger euro, but it should otherwise be an uneventful meeting. Looking ahead, a lot of room remains for further ECB actions. We expect the ECB to increase QE at the December 10 meeting. However, another rate cut seems very unlikely, as does activation of OMT. POSSIBLE NEXT STEPS 1. Jawbone the euro weaker – POSSIBLE NOW, LIKELY IN Q4. The strong euro is surely a topic of internal discussion, but MPC members are usually reluctant to address it publicly. ECB Chief Economist Lane recently signaled some concern about the strong euro, noting that it feeds into the bank’s forecasts and policy settings. Press reports

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, developed markets, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The ECB meets tomorrow and is widely expected to stand pat. Macro forecasts may be tweaked modestly and there are some risks of jawboning against the stronger euro, but it should otherwise be an uneventful meeting. Looking ahead, a lot of room remains for further ECB actions. We expect the ECB to increase QE at the December 10 meeting. However, another rate cut seems very unlikely, as does activation of OMT.

| POSSIBLE NEXT STEPS

1. Jawbone the euro weaker – POSSIBLE NOW, LIKELY IN Q4. The strong euro is surely a topic of internal discussion, but MPC members are usually reluctant to address it publicly. ECB Chief Economist Lane recently signaled some concern about the strong euro, noting that it feeds into the bank’s forecasts and policy settings. Press reports suggest other officials are also worried about the currency impact on exports and inflation. While the ECB professes not to target the exchange rate, that never prevented Trichet or Draghi from making comments that worked to weaken the euro. Of course, without any underlying shift in relative monetary policy stances or economic fundamentals, jawboning typically has limited impact. In any case, Madame Lagarde will surely get lots of questions about the euro this time around. 2. Tweak macro forecasts – POSSIBLE NOW, LIKELY IN Q4. The ECB updated its forecasts at the June 4 meeting, with baseline forecasts for 2020 and 2021 GDP revised to -8.7% and +5.2% from 0.8% and 1.3% in March, respectively, and baseline forecasts for 2020 and 2021 inflation revised to 0.3% and 0.8% from 1.1% and 1.4% in March, respectively. Press reports suggest that the ECB will modestly upgrade its 2020 GDP forecast tomorrow. If so, the ECB is signaling that the severe scenario presented this Spring (-12.8% GDP contraction this year followed by 3.3% growth next year) is seen as less likely. With uncertainty rising due to the recent resurgence in virus numbers, there is a case to be made for waiting until the December meeting to tweak the forecasts. 3. Further increase and extend Quantitative Easing (QE) – UNLIKELY NOW, LIKELY IN Q4. The ECB increased its PEPP at the June 4 meeting by EUR600 bln to EUR1.35 trln, slightly more than the expected EUR500 bln. In addition, PEPP was extended beyond December until at least June 2021. The ECB’s balance sheet stood around EUR6.44 trln ($7.7 trln) at the end of August, up from EUR4.7 trln ($5.17 trln) at the beginning of this year. This 37% increase pales in comparison to the nearly 70% increase in the Fed’s balance sheet this year. However, it continues to grow even as the Fed’s appears to have topped out near $7 trln. |

Balance Sheets, USD Trin, 2007-2019 - Click to enlarge |

| 4. Tweak Pandemic Emergency Longer-Term Refinancing Operations (PELTROs) or Targeted Longer-Term Refinancing Operations (TLTROs) – VERY UNLIKELY NOW, POSSIBLE IN Q4. The ECB introduced PELTROs at the April 30 meeting and the take-up to the first one on May 20 was disappointing, coming at only EUR851 mln. However, due to more favorable rates, the last TLTRO take-up June 18 was robust, with banks securing EUR1.3 trln of funding for three years. As evidenced by the record low -0.557% for the Euro Short-Term Rate (ESTR), the eurozone is awash in liquidity and so further measures to boost it seem unnecessary now.5. Cut rates – VERY UNLIKELY NOW, VERY UNLIKELY IN Q4. While the bank has left the door open to take rates more negative, it’s clearly reluctant to do so due to the potential for doing further harm to the banking sector.

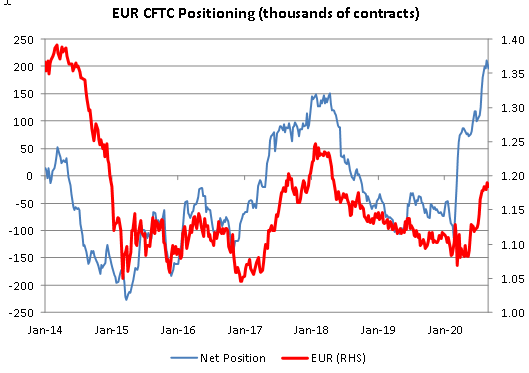

Many at the ECB (as well as the BOJ and SNB, it would seem) question the efficacy of negative rates and whether the costs of going more negative outweigh the benefits. WIRP suggests nearly 70% odds of another cut by April 2021. If it eventually does cut, however, we expect the ECB will increase so-called “tiering” that allows banks to avoid some of the increased interest charges on their deposits at the ECB. INVESTMENT OUTLOOK Our long-standing bearish dollar call was reinforced by Powell at Jackson Hole, and we still look for renewed euro strength. Once this bout of risk aversions settles down, we expect the dollar weakness trend to resume, leading to a clean break above the $1.20 area, with the April 2018 high near $1.24 seen as the next big target. However, positioning is getting extended. The latest CFTC data shows net euro longs for non-commercial accounts stand at 197k contracts for the week ended September 1, down slightly from the record high of 212k the previous week. As a result, we believe further gains will get tougher and tougher from a positioning standpoint. |

EUR CFTC Positioning, 2014-2020 - Click to enlarge |

|

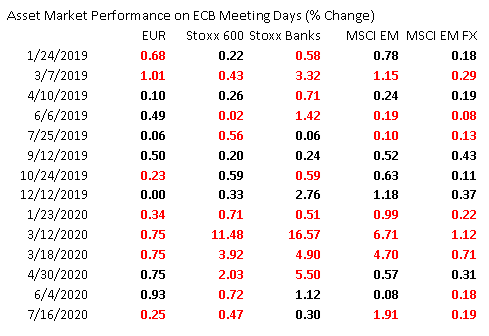

Since the July 16 meeting, the euro has gained 4% vs. the dollar and 3% vs. the yen. The move has been neither excessive nor “brutal” but eurozone policymakers will remain vigilant. Draghi often pushed back at euro strength during his tenure, let’s see how Lagarde approaches it going forward As noted above, this meeting may be too soon for serious jawboning but policymakers are likely watching it carefully. A significantly stronger euro is the last thing the eurozone needs as it flirts with deflation again, with CPI falling -0.2% y/y in August vs. an expected gain of 0.2% y/y.The euro has generally tended to weaken on ECB decision days. In 2018, the euro weakened on 7 of the 8 ECB meeting days. In 2019, the euro strengthened on 5 of the 8 ECB meeting days, though 3 of those days were less than 0.1%.

In 2020, the euro has weakened on 3 of the 5 scheduled ECB meeting days so far, and also weakened on the emergency meeting March 18, when the Pandemic Emergency Purchase Programme (PEPP) was introduced. Looking at other asset classes, the behavior on ECB meeting days this year has been very similar. STOXX Europe 600 has fallen on all of the 5 scheduled ECB meeting days so far, and also fell on the emergency meeting March 18, while STOXX Banks has fallen on 3 of the 5 scheduled meetings as well at the emergency meeting. Both MSCI EM and MSCI EM FX have fallen on 3 of the 5 scheduled meeting days as well as at the emergency meeting. |

Asset Market Performance on ECB Meeting Days - Click to enlarge |

You Might Also Like

Where Has All the Carry Gone?

Where Has All the Carry Gone?

Despite broad-based dollar weakness, EM currencies have not fully participated in the risk on environment that’s now in place. The good news is that fundamentals matter again. The bad news is that there are a lot of EM countries with bad fundamentals, and the secular decline in carry no longer gives these weaklings any cover.

The dollar is likely to remain under pressure after Powell’s dovish message at Jackson Hole. August jobs data Friday will be the data highlight of the week. The Fed releases its Beige Book report Wednesday; Powell will face many questions about the Framework Review that he unveiled at Jackson Hole.

ECB Approaching its Bazooka Moment

ECB Approaching its Bazooka Moment

The ECB appears to be moving closer to activating Outright Monetary Transactions (OMT). Despite being part of Draghi’s “whatever it takes” moment, OMT has never been used. If the Fed’s open-ended QE is seen as dollar-negative, then OMT should be seen as euro-negative.

Lessons from Singapore?

Lessons from Singapore?

Singapore has been hailed for its quick response to the coronavirus that limited initial infections, but the outlook is shifting. Despite their early success, they will have to revert to a lockdown. Can Singapore’s experience offer any lessons for European and the US policymakers?

There are some indexing events this week that could add to market volatility; the IMF will release updated global growth forecasts Wednesday. The regional Fed manufacturing surveys for June will continue to roll out; Fed speaking engagements are somewhat limited this week.

EM currencies took advantage of broad dollar weakness against the majors last week, with most gaining against the greenback. Yet the week ended on a bit of a risk-off note as concerns intensified about the resurgent virus and the impact on the still-weak global economy.

The dollar got some traction against the majors towards the end of last week. This weighed on EM FX, with the high best currencies TRY, BRL, CLP, and ZAR leading the losers. We downplay risk of contagion from Turkey, but we acknowledge it will keep investors wary of the countries with poor fundamentals.

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

Update September 7, 2020: SNB buying euros at high prices. Sight Deposits have risen by +1.3 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +1.3 bn. compared to last week.

Tags: Articles,developed markets,Featured,newsletter