Over the past two months we have witnessed historic turmoil followed by unprecedented intervention by policy makers and central banks in supporting the capital markets (and more). In many ways the 2020 COVID-19 pandemic is very different from the 2008 global financial crisis, but for some, certain old concerns still linger. In the face of short selling bans and worries about market liquidity, we discuss below how best to navigate some of the common objections and concerns related to securities lending and how to position your securities lending program in the current environment and beyond. Fees and performance remain top of mind Even more than before, investors in investment funds are increasingly aware of the relationship between fees and performance. Every

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, Featured, newsletter, Securities Lending

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Over the past two months we have witnessed historic turmoil followed by unprecedented intervention by policy makers and central banks in supporting the capital markets (and more). In many ways the 2020 COVID-19 pandemic is very different from the 2008 global financial crisis, but for some, certain old concerns still linger. In the face of short selling bans and worries about market liquidity, we discuss below how best to navigate some of the common objections and concerns related to securities lending and how to position your securities lending program in the current environment and beyond.

Fees and performance remain top of mind

Even more than before, investors in investment funds are increasingly aware of the relationship between fees and performance. Every asset manager faces greater fiduciary pressure to evaluate techniques that can add revenue to their funds and mitigate the impact of fees on performance, and many are incorporating a well-run securities lending program into their engagement policy. It’s therefore imperative to determine whether securities lending can help improve performance for a fund’s investors.

Historically, the decision whether to lend or not has been a philosophical one. But with the introduction of new tools and the availability of more data than ever before, the decision whether to lend is made easier through rigorous analysis paired with data specific to a fund’s circumstances. BBH has worked with some of the world’s most sophisticated asset managers to assess the value of securities lending using these new methods.

“Lending drives prices down by facilitating shorting”

The most common objection that we have heard from portfolio managers and chief investment officers is that securities lending facilitates short selling, which undermines their investment objectives. By using a sample loan portfolio, we can address this point with a few helpful data points. First, let’s look at the distribution of revenue versus short interest in equities. Our analysis reveals that in many cases, asset managers can earn 75% from stocks where short interest is less than 5% and 99% from stocks where short interest is 15% or less*. In other words, shorting is relatively low in these stocks and the holdings in these stocks would not likely be lent into an environment of high speculative interest or aggressive shorting. At this level of short interest, portfolio managers typically take the view that a program may “lend at will.”

Of course, the relationship between short interest and securities lending revenue will vary from security to security and portfolio to portfolio. However, analysing a portfolio in this way enables an objective discussion about the potential guardrails that limit securities loans to those securities the portfolio manager is comfortable lending. This would result in a more objective and thoughtful approach than what is typically a binary decision of to lend or not to lend.

“Lending will adversely impact my operations”

One of the most common questions regarding securities lending — and one that is highly relevant in today’s volatile environment — is the potential for securities lending to interfere with the investment process, specifically when a stock on loan is sold and a late returning recall causes the sale to fail.

Borrowers are contractually bound to return positions that are recalled from loan when the lender sells those shares. Typically, most securities loan agreements require the lender to inform the agent of its sale of a loaned security prior to the close of business in the relevant market on trade date (T+0). Sale notifications do not require a special process, simply a copy of the security settlement instruction that would usually be sent to the custodian.

Lenders who provide T+0 sale notifications should typically expect their shares to be returned within the settlement cycle of their share sale. If the borrower fails to return the securities in time, then either the stock exchange or the agent lender will “buy-in” the securities necessary to settle the lender’s sale, with any associated costs being borne by the borrower. Agent lenders may offer slightly differing terms and consequential damages coverage.

Beyond contractual remedies, it is important to consider the number of securities on loan. A “volume lender” may have a significant amount of a portfolio’s assets on loan at any time, while a “value lender” may have just a few high value securities out on loan during that same period. Data analysis can highlight how many securities are likely to be on loan at any given time, the markets in which they trade, and hence, their settlement windows.

A well-managed, value-based program with a limited number of securities on loan at any time should not typically generate settlement issues for the investment process. The level of automation and operational sophistication of agent lenders and custodians result in a highly efficient operational service.

Bottom line

For those asset managers who have decided not to engage in securities lending, the pressure on fees means there’s now more reason than ever to review that decision. In the past, this question might have been resolved at a philosophical level. Today, however, there are far more rigorous and precise methods available to establish the case for or against participating in a securities lending program. More importantly, once a review has been conducted, the asset manager will have fulfilled its responsibility to thoroughly assess the benefit to its fund investors.

To continue this conversation please contact your Securities Lending RM directly.

*BBH analysis 2020

You Might Also Like

Some Thoughts on Recent Foreign Exchange Intervention

Some Thoughts on Recent Foreign Exchange Intervention

Dollar softness this week will take some pressure off of the foreign currencies but it’s too early to sound the all clear. This piece focuses on how central banks around the world may be intervening to influence their currencies. Most of the world, particularly EM, is grappling with supporting weak currencies but a select few are dealing with stronger currencies. This is a very opaque process and so we are simply making our best guesses.

Negative News from Europe Helps Dollar Build on Gains

Negative News from Europe Helps Dollar Build on Gains

UK has been confirmed to have the highest death toll in Europe the dollar is getting more traction. Reports suggest Congress is resisting President Trump’s call for a payroll tax cut; ADP private sector jobs data is expected to come in at -21 mln. Brazil is expected to cut rates 50 bp; Fitch cut its outlook on Brazil to negative; Chile is expected to keep rates steady.

Dollar Mixed as Doves Fly

Dollar Mixed as Doves Fly

Measures of cross-market implied volatility have been stable for a few weeks now. Weekly jobless claims are expected at 3 mln; reports suggest House Democrats are pushing ahead with a possible vote next week on another relief package. Canada reports April Ivey PMI; Peru is expected to keep rates steady; Brazil COPOM delivered a dovish surprise last night.

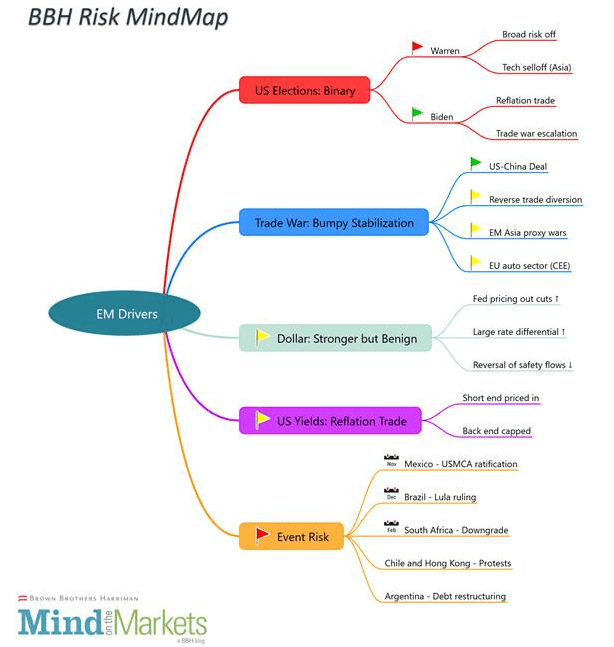

Emerging Market Risk Map

Emerging Market Risk Map

With year-end upon us, we review some of the key risks to EM assets and how we think they progress from here. In short, the two most significant downside risks would be a decisive improvement in Elizabeth Warren’s polling figures and an upset in the US-China trade negotiations.

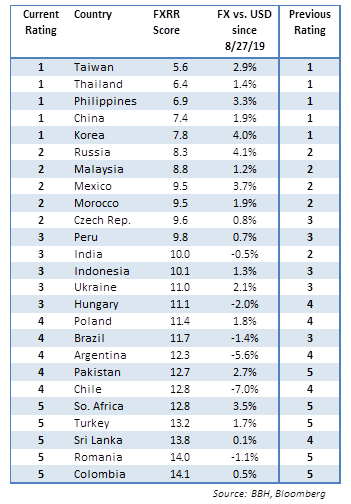

EM FX Model for Q4 2019

EM FX Model for Q4 2019

EM FX has rallied sharply in recent weeks, helped by growing optimism that we’ve seen the worst of the US-China trade war. Given our more constructive outlook on EM, we believe MSCI EM FX should eventually test the 1657.50 high from July. We see continued divergences within the asset class. Our 1-rated (strongest fundamentals) grouping for Q4 2019 consists of TWD, THB, PHP, CNY, and KRW.

Dollar Stabilizes as Markets Await Fresh Drivers

Dollar Stabilizes as Markets Await Fresh Drivers

Press reports suggest that the mood in Beijing is pessimistic after President Trump pushed back against tariff rollbacks. Fed Chair Powell met with President Trump and Treasury Secretary Mnuchin yesterday. Hungary is expected to keep rates steady; the deadline to form a government in Israel is fast approaching. RBA released dovish minutes from its November policy meeting.

Dollar and Equities Sink as Trade Pessimism Rises

Dollar and Equities Sink as Trade Pessimism Rises

Pessimism regarding a Phase One trade deal has intensified; further muddying the waters are recent US Congressional actions. FOMC minutes contained no surprises; regional Fed manufacturing surveys for November continue. South Africa is expected to cut rates by 25 bp to 6.25%. Korea reported trade data for the first twenty days of November; Indonesia kept rates steady at 5.0%, as expected.

The dollar was surprisingly resilient last week; we look for further dollar gains ahead. It is a holiday shortened week in the US, but there are still some major data releases. There is a fair amount of eurozone data this week; UK Prime Minister Johnson unveiled his Tory manifesto. Hong Kong held local elections this weekend; tensions between Japan and Korea appear to have eased, but questions remain.

Tags: Articles,Featured,newsletter,Securities Lending