James Rickards holds a gold bar in a vault near Zurich, Switzerland. The bar is a so-called LBMA “good delivery” bar which weigh 400 ounces (over 99.9% purity), and is worth about 0,000 at current market prices. In 1971 it was worth ,000. ◆ WHY GOLD? That’s a question I’m asked frequently. It’s usually followed by a comment along the lines of, “I don’t get it. It’s just a shiny rock. People dig it out of the ground and then put it back in the ground. What’s the point?” I usually begin my reply by saying, “It’s not a rock, it’s a metal” and then go from there. I have a lot of sympathy in these conversations. The fact that people don’t know much about gold today is not exactly their fault. The economics establishment of policymakers, academics and central

Topics:

Mark O'Byrne considers the following as important: 6a.) GoldCore, 6a) Gold & Bitcoin, Daily Market Update, Featured, gold bug, gold nut, Good Delivery, Jim Rickards, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

James Rickards holds a gold bar in a vault near Zurich, Switzerland. The bar is a so-called LBMA “good delivery” bar which weigh 400 ounces (over 99.9% purity), and is worth about $700,000 at current market prices. In 1971 it was worth $14,000.

◆ WHY GOLD?

That’s a question I’m asked frequently. It’s usually followed by a comment along the lines of, “I don’t get it. It’s just a shiny rock. People dig it out of the ground and then put it back in the ground. What’s the point?”

I usually begin my reply by saying, “It’s not a rock, it’s a metal” and then go from there.

I have a lot of sympathy in these conversations. The fact that people don’t know much about gold today is not exactly their fault. The economics establishment of policymakers, academics and central bankers have closed ranks around the idea that gold is a taboo subject.

You can teach it in mining colleges, but don’t dare teach it in economics departments. If you have a kind word for gold in a monetary context, you are immediately labeled a “gold nut,” “gold bug,” “Neanderthal” or something worse. You are excluded from the conversation. Case closed.

It wasn’t always this way. I was a graduate student in international economics in 1973-1974. Many observers believe that the gold standard “ended” on August 15, 1971 when President Nixon suspended the redemption of dollars for gold by foreign trading partners. That’s not exactly what happened.

Nixon’s announcement was a big deal. But, he intended the suspension to be “temporary” and he said so in the announcement. The idea was to call a kind of “time out” on redemptions, hold a new international monetary conference similar to Bretton Woods in 1944, devalue the dollar against gold (and other currencies such as the German Deutschemark and Japanese Yen), and then return to the gold standard at the new exchange rates.

I was able to confirm this plan with two of Nixon’s advisors who were with him at Camp David in 1971 when he made the announcement. I spoke to Kenneth Dam (an executive branch lawyer) and Paul Volcker (at the time, the Deputy Secretary of the Treasury). They both confirmed that the suspension of gold redemptions was meant to be temporary, and the goal was to return to gold at new prices.

Some of what Nixon wanted did happen, and some did not. The international conference took place in Washington, DC in December 1971 and resulted in the Smithsonian Agreement. The dollar was devalued from $35 per ounce to $38 per ounce (it was later devalued again to $42.22 per ounce), and the dollar was devalued against the major currencies of Germany, Japan, the UK, France and Italy.

Yet, the return to a true gold standard never happened. This was a chaotic time in the history of international monetary policy. Germany and Japan moved to floating exchange rates under the misguided influence of Milton Friedman who did not really understand the role of currencies in international trade and direct foreign investment. France dug in her heels and insisted on a return to a true gold standard.

Also, Nixon got caught up in his 1972 reelection campaign to be followed closely by the Watergate scandal, so he lost focus on gold. In the end, the devaluation was on the books but official gold convertibility never returned.

All of this monetary wrangling took a few years to play out. It was not until 1974 that the IMF officially declared that gold was not a monetary asset (although the IMF carried thousands of gold on its books in the 1970s, and still has 2,814 tons of gold, the third largest holding in the world after the U.S. and Germany).

The result was that my Class of 1974 was the last class to be taught gold as a monetary asset. If you took economics after that, gold had been consigned to the history books. No one taught it and no one learned it. Gold was still a “commodity” and something that was taught in mining colleges, but not in economics.

No wonder most people today don’t understand gold.

Maybe gold was banned from the classroom, but it was not banned from the real world. In fact, there was another major development just one year after I graduated. In 1974, President Ford signed a law that reversed President Franklin Roosevelt’s notorious Executive Order 6102. FDR made ownership of gold bullion by American citizens illegal in 1933. Gold was contraband like heroin or machine guns.

President Ford legalized it again. For the first time in over 40 years, it was once again legal for Americans to own gold coins and bars. The official gold standard was dead, but a new “private gold standard” had just begun.

That’s when things got interesting.

Now that gold traded freely, we saw the beginning of bull and bear markets, something that doesn’t happen on a gold standard where the price is fixed.

The two great bull markets were 1971-1980 (gold up 2,200%) and 1999-2011 (gold up 760%). In between these bull markets were the two bear markets (1981-1998 and 2011-2015), but the long-term trend is undeniable. Since 1971, gold is up 5,000% even after the bear market setbacks.

Now the third great bull market is underway. It began on December 16, 2015 when gold bottomed at $1,050 per ounce at the end of the 2011-2015 bear market. Since then, gold is up over 65%. That’s a nice gain, but it’s small change compared to 2,200% and 760% gains in the last two bull markets.

When it comes to capital and commodity markets, nothing moves in a straight line, especially gold.

But this pattern suggests the biggest gains in gold prices are yet to come. And right now, my models are telling me that gold is poised for historic gains as the third great bull market gains steam.

Right now gold’s trading at over $1,700. What could push it firmly over $2,000 per ounce and headed higher? There are three main drivers:

The first is a loss of confidence in the U.S. dollar in response to massive money printing to bail out investors in the pandemic. If central banks have to use gold as a reference point to restore confidence, the price will have to be $10,000 per ounce or higher. Any lower price would force central banks to reduce their money supplies to maintain parity, which would be highly deflationary.

The second driver is a simple continuation of the bull market. Using the prior two bull markets as reference points, a simple average of those gains during those durations would put gold at $14,000 per ounce or higher by 2025.

The third driver is panic buying in response to a new disaster. This could take the form of a “second wave” of infections from the Wuhan Virus, a failure of a gold ETF or the COMEX exchange to honor physical delivery requirements, or a victory by Joe Biden in the presidential election.

The gold market is not priced for any of these outcomes right now. It won’t take all three events to drive gold higher. Any one would do just fine. But, none of the three can be ruled out.

These events (and others) would push gold well past $2,000 per ounce, on its way to $3,000 per ounce and ultimately much higher along the lines described above.

Full article and subscribe to the Daily Reckoning here

You Might Also Like

Global Silver Investment Demand To Surge While Supply Weak (World Silver Survey 2020)

Global Silver Investment Demand To Surge While Supply Weak (World Silver Survey 2020)

◆ WORLD SILVER SURVEY 2020 from the SILVER INSTITUTE GLOBAL SILVER DEMAND EDGED HIGHER IN 2019, WITH INVESTMENT DEMAND UP 12%, WHILE SILVER MINE SUPPLY FELL FOR THE FOURTH CONSECUTIVE YEAR Global silver demand was pushed higher in 2019, with a 12 percent increase in investment demand as retail and institutional investors focused their attention on the long-term investment appeal of the white metal.

Fed Is Monetizing 90 percent of U.S. Deficit to Keep Interest Rates from Rising and Crashing Markets

Fed Is Monetizing 90 percent of U.S. Deficit to Keep Interest Rates from Rising and Crashing Markets

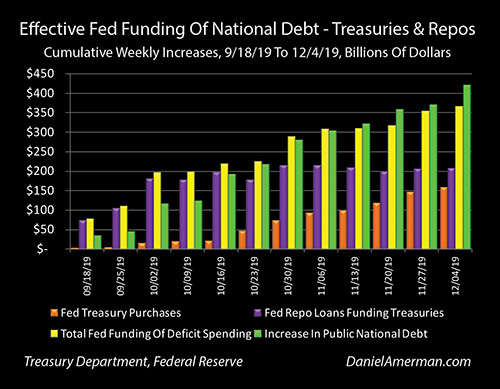

By Daniel R. Amerman, CFAAs can be seen in the graph above, for the last 12 weeks there has been a stunning visual correlation between the yellow bars of the total weekly funding of deficits by the Federal Reserve, and the green bars of the weekly deficit spending by the United States government.

Why Do Prudent Indians Diversify Into Gold?

Why Do Prudent Indians Diversify Into Gold?

◆ Indians diversify into gold coins, bars and jewellery because it never fails them in an emergency◆ Indians are simply very prudent and practical and believe in channeling some of their wealth and saving into physical gold ◆ “A woman’s gold is both her personal treasure and plays a functional role as the family’s financial buffer” – Richard Davies

“All You Need To Do Is Own Gold and Silver” To Make Money In 2020

“All You Need To Do Is Own Gold and Silver” To Make Money In 2020

If you want to make money from investing, it’s simple: find a bull market and go long. And in 2020 gold and silver are in a bull market. by Dominic Frisby via the UK’s best-selling financial magazine Money Week

I ran into Jim Mellon at a party at the weekend, and we soon got talking about markets. One of his comments – stated with surety and simplicity – has stuck in my mind.

Gold May Top $2,000 As “Prices Surge On Global Fear”

Gold May Top $2,000 As “Prices Surge On Global Fear”

Gold was one of the few investments heading higher Monday as worries about the coronavirus outbreak led to a steep market slide. Gold is now up more than 20% in the past year, and trading near $1,600 an ounce, its highest level since 2013. Other precious metals, such as silver and platinum, have rallied too. Meanwhile, the Dow was down nearly 350 points in midday trading.

Gold Consolidates Near Six Year Record Highs At $1574/oz; WHO’s ‘Tip of the Iceberg’ Virus Warning

Gold Consolidates Near Six Year Record Highs At $1574/oz; WHO’s ‘Tip of the Iceberg’ Virus Warning

Gold climbed for a fourth day as investors weighed the unfolding coronavirus crisis, including a stark warning from the head of the World Health Organization about the potential for more cases beyond China and signs the disease is spreading in the key Asian trading hub of Singapore.

Gold Coins Worth £80,000 Found In Retiree’s Drawers In Cottage: “It Was Mind-Blowing. I Felt Like a Pirate in a Grotto”

Gold Coins Worth £80,000 Found In Retiree’s Drawers In Cottage: “It Was Mind-Blowing. I Felt Like a Pirate in a Grotto”

Gold coins including gold sovereigns found in drawers of deceased retiree’s cottage sell at auction for £80,000. ◆ British gold coins including gold sovereigns from the Royal Mint found in drawers and cupboards of cottage fetch £80,000; one British gold sovereign found in a sugar bowl. ◆ Auctioneer John Rolfe expected little before he entered damp, rat-infested property near Stroud.

Tags: Daily Market Update,Featured,gold bug,gold nut,Good Delivery,Jim Rickards,newsletter