Interview with Ronald Stöferle – Part I As we embark on this new decade, there are plenty of good reasons to be optimistic about gold’s prospects. The global economy and the financial system are already stretched to a breaking point and demand for precious metals is heating up. This, of course, is plain for all to see, even as mainstream investors and analysts still refuse to face facts and prefer to focus on naïve hopes of an eternal expansion. These facts, however, remain, and the more one looks into them in detail, the more obvious it seems that there are great risks going forward. To discuss these issues and to shed some more light on what investors might expect in the new year and beyond, I turned to my long-time friend Ronald Stöferle, who serves as the

Topics:

Claudio Grass considers the following as important: 11 trillion negative-yielding debt, 6a.) Claudio Grass, 6b) Austrian Economics, Crisis, Economics, Featured, Finance, Geopolitical Risk, Gold, gold all time highs, Monetary, newsletter, recession fears, Ronald Stöferle, Thoughts, Uncategorized

This could be interesting, too:

Claudio Grass writes The Case Against Fordism

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Interview with Ronald Stöferle – Part I

As we embark on this new decade, there are plenty of good reasons to be optimistic about gold’s prospects. The global economy and the financial system are already stretched to a breaking point and demand for precious metals is heating up. This, of course, is plain for all to see, even as mainstream investors and analysts still refuse to face facts and prefer to focus on naïve hopes of an eternal expansion. These facts, however, remain, and the more one looks into them in detail, the more obvious it seems that there are great risks going forward.

To discuss these issues and to shed some more light on what investors might expect in the new year and beyond, I turned to my long-time friend Ronald Stöferle, who serves as the managing partner and fund manager at Incrementum AG, based in the Principality of Liechtenstein. Ronald is perhaps already well known to many readers, due to the widely popular “In Gold We Trust” report, that has gathered a very loyal following over the years and is highly regarded for the amount and the quality of the research and analysis it provides. His latest book, “The Zero Interest Trap”, that he co-authored with Rahim Taghizadegan and Gregor Hochreiter, is also a must-read, outlining the risks, but also the actionable opportunities, that the current interest rate climate has created for investors.

Claudio Grass (CG): It’s been an exciting time for precious metals investors. Over the last few months, we’ve seen significant price gains in gold and silver, after a long almost dormant period. Why do you think this is happening now? What changed?

| Ronald-Peter Stöferle (RPS): The massive policy U-turn by the Fed certainly played a part, and so did the move by the ECB to resume its own easing policies and monthly asset buying spree. We have officially returned to loose monetary policies across the board, and not only did this provide a boost to precious metals until now, but I also think it will persist into 2020, along with balance sheet expansion. I think another important factor was the renewed interest in gold by institutional players, as demand from that side of the market also picked up significantly.

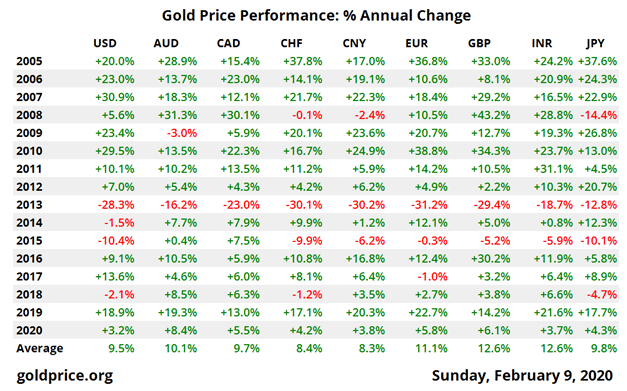

Nevertheless, let us not forget that what we’ve seen over the past few months is just a gold breakout in USD terms. It is, of course, very noteworthy, but it is important to remember that gold has already been in a bull market in other currencies for quite some time. This bull market has started much earlier, but went mostly unnoticed, because everybody is just staring at the USD price of gold. All the while, in EUR, AUD, CAD terms, gold has been trading at or near all-time highs. |

Gold Price Performance: percent Annual Change - Click to enlarge |

CG: In the last edition of the In Gold We Trust report, you predicted that the world’s central bankers would soon return to the easing path and relaunch QE. We saw that materialize at the ECB in November, while the Fed also started injecting cash in the repo market. And yet growth is slipping away, while their own inflation targets remain out of reach. Why is it that central bankers keep doing the same thing, but expect different results?

RPS: Well, perhaps they still believe that their “cure” is correct, but their dose was wrong, so they’ll just keep increasing it. Of course, all their theories are entirely based on purely hypothetical assumptions and deeply flawed models, using aggregates, complex formulas, inflation baskets and the like, that completely disregard human action and the actual facts on the ground.

Central banks – and the economic agents directly and indirectly connected to them, such as governments, banks and companies – have not yet realized that we live in a completely new monetary world since the breakdown of the interbanking market in August 2007. When the Fed “stepped in” the repo market, this was considered as an intervention, even though repo market operations were actually the way in which central banks enforced their monetary policy. So the old “normal” has become the new extraordinary, while the new normal has not been formalized and institutionalized yet.

CG: Recession fears appear to be on the rise, as more and more investors have doubts about both equity markets and the economy at large in the new year. What are your expectations for 2020?

RPS: I wouldn’t be surprised if we entered a recession in 2020. After all, we’ve had the longest expansion phase in history, which now seems increasingly strained and unsustainable, with slowdown signs everywhere. A recession has been in the pipeline for quite some time already.

And let’s not forget about the multitude of recession signals we’ve already seen over the last year. A good example is the yield curve inversion. Its importance has been largely downplayed by mainstream analysts and ignored by many complacent investors, but it is a very strong and historically reliable warning.

CG: How do you evaluate the current geopolitical risks against the deeper, structural vulnerabilities of most major economies, like huge debt burdens and overstretched monetary policies? What do you think would trigger the next recession?

RPS: It is notoriously hard to predict a black swan and especially in this overstretched phase, there are many different risk factors and potential events that could act as the trigger. The coronavirus crisis was a good example of that: it came out of nowhere and within just a few days it had taken a significant toll on the markets. The problem is that the entire system is already so extraordinarily fragile that anything can serve as an excuse to set off an avalanche. The scariest part is that most mainstream investors and everyday citizens aren’t even aware of the severity of the risks we face.

The financial press has been ignoring all these stressors for way too long. There has hardly been any debate over the policies enacted by the Fed and ECB to support the banking sector, like the tiering of the deposit rate, the extension of TLTROs and the Fed’s intervention in the repo market. These developments have gone underreported and their actual impact largely undiscussed.

CG: You’ve stated before that trust is broadly eroding, but isn’t the existence of some $11 trillion in negative-yielding debt a tacit expression of the highest confidence in paper money and the central bankers who manage it?

RPS: Trust is very asymmetrical. It takes years or even decades to build, and mere moments to destroy it. The issue here is really quite simple: there is a marked lack of appreciation for the potential return of inflation, while investors also seem convinced that the negative correlation between stocks and bonds will continue forever! Of course, inflation is the biggest pain trade for those bonds and the possibility of it coming back has been highly discounted and underestimated for years.

The USD has been the linchpin of the deflationary mindset. This means an environment of capped commodity prices, constrained growth in emerging markets and capital flows to the US. But this is now beginning to change.

Central banks are also very open about their desire to stimulate higher inflation rates. Fed Chair Powell’s own words were very clear: “When a central bank undershoots its inflation target, it can promise the public that it will OVERSHOOT in the future!” So, the big question here is: where will all this capital flow to, when inflation does become a concern?

END OF PART 1

Tags: 11 trillion negative-yielding debt,Crisis,Economics,Featured,Finance,Geopolitical Risk,Gold,gold all time highs,Monetary,newsletter,recession fears,Ronald Stöferle,Thoughts,Uncategorized