Swiss Franc The Euro has risen by 0.23% to 1.0822 EUR/CHF and USD/CHF, September 28 Source: markets.ft.com - Click to enlarge FX Rates Overview: Following the strong finish in the US before the weekend, global equities are paring last week’s slide. The MSCI Asia Pacific Index rose to for a second session. Markets in Japan, Taiwan, South Korea, and India rose by more than 1%. China and Australia were notable exceptions. Europe’s Dow Jones Stoxx 600 is gapped slightly higher and hasn’t looked back. Its 1.85% gain in the morning, if sustained, would be the largest advance since early August. US shares are also trading more than 1% better, pointing to a gap higher opening. Interest has been drained from the debt market, where the US 10-year is hovering around 67

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, China, Currency Movement, Featured, newsletter, Switzerland, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

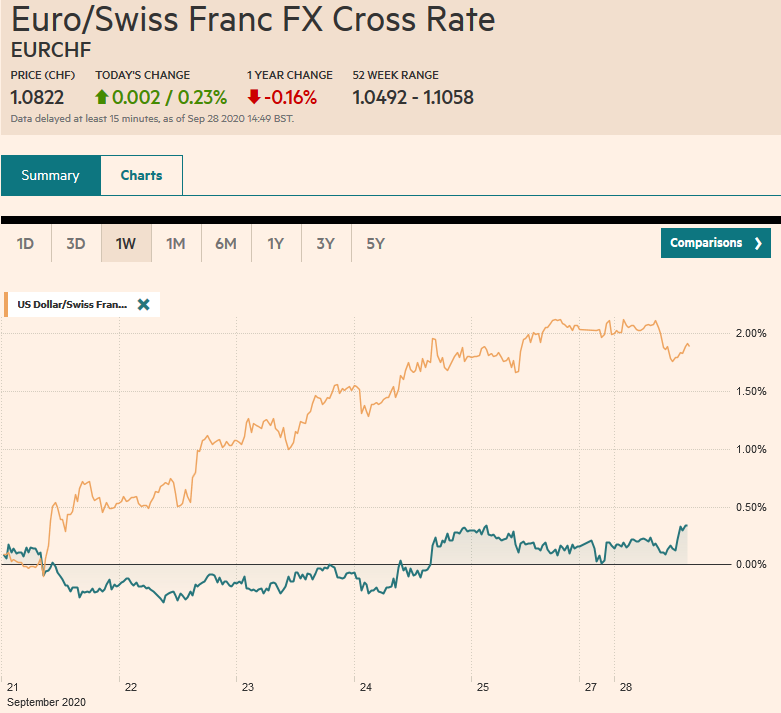

Swiss FrancThe Euro has risen by 0.23% to 1.0822 |

EUR/CHF and USD/CHF, September 28 Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Following the strong finish in the US before the weekend, global equities are paring last week’s slide. The MSCI Asia Pacific Index rose to for a second session. Markets in Japan, Taiwan, South Korea, and India rose by more than 1%. China and Australia were notable exceptions. Europe’s Dow Jones Stoxx 600 is gapped slightly higher and hasn’t looked back. Its 1.85% gain in the morning, if sustained, would be the largest advance since early August. US shares are also trading more than 1% better, pointing to a gap higher opening. Interest has been drained from the debt market, where the US 10-year is hovering around 67 bp, and European bond markets are narrowing mixed. The dollar is mostly softer against the majors. Sterling, which closed firmly end the end of last week, leads today’s move, rising more than a cent to test the $1.29 area. Emerging market currencies are mostly softer, and the JP Morgan Emerging Market Currency Index is off about 0.2% in what would be the sixth decline over the past seven sessions. Gold remains pinned near its recent lows near $1850, while November WTI is straddling the $40 a barrel level in quiet trading. |

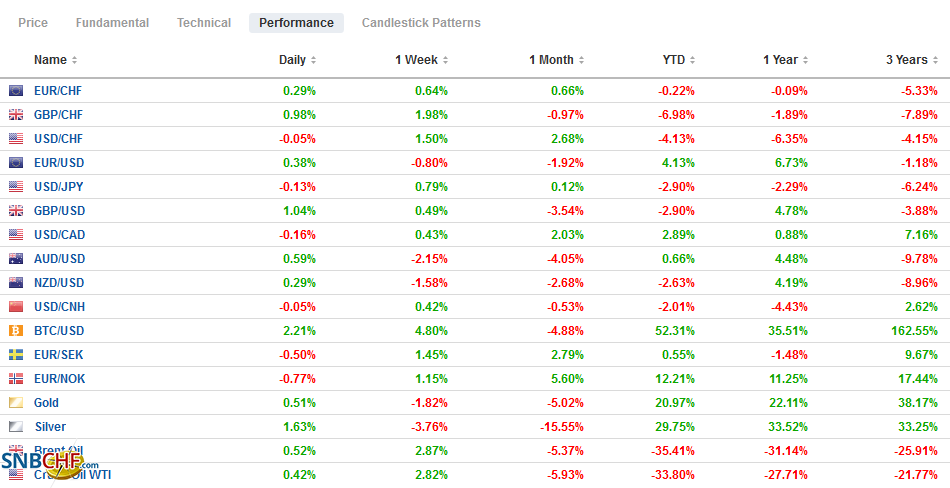

FX Performance, September 28 - Click to enlarge |

Asia Pacific

While US courts are stymying the Trump administration’s efforts to force a sale of TikTok and shut WeChat, it has taken a new step to undermine Beijing’s economic push. It is imposed export restrictions on its largest semiconductor fabrication company SMIC. It has been discussed for several weeks and is not a surprise. The US claims that there is an unacceptable risk that the chip military-end use, though the company denies it. Reports suggest Huawei bought a fifth of SMIC semiconductors, and Qualcomm uses SMIC fabrication for some of its chips. It impacts European producers such as ASML, which has been unable to obtain a license to exports to SMIC. There appears to be some discretion in the implementation, but this represents a new escalation in the US-China confrontation.

Separately, over the weekend, China’s reported that industrial profits in August rose 19% after a 19.1% gain in July. Through the first eight months of 2002, industrial profits in China are about 4.4% lower than a year ago. Mining and equipment manufacturing sectors stand out. The September PMIs are due out of the next couple of days. Note that Chinese markets are closed for about a week starting October 1.

There is some speculation that Japan’s Prime Minister Suga is considering calling an extraordinary Diet session at the end of October. This could delay earlier fiscal efforts. Suga’s strategy is still not clear. Some observers see an early election and then a supplemental budget. Japan reports August industrial production and retail sales this week ahead of the Tankan Survey.

The dollar has traded between about JPY105.25 and JPY105.70 so far today, which is just inside the range seen before the weekend. The intraday technicals suggest the consolidative tone may persist through the North American session. The Australian dollar is also confined to the pre-weekend range (~$0.7005-$0.7080). Some attribute the Aussie’s slightly firmer tone today to a local bank’s shift of its rate cut call from October to November. A quiet session today could see a little range extension higher. The PBOC set the dollar’s reference rate at CNY6.8252, a little lower than the bank models implied. As the quarter-end and the Golden Week holiday approaches, it threatens to inject volatility into Chinese money markets.

Europe

In yesterday’s referendum, Swiss voters soundly rejected the proposal to end the existing freedom of movement arrangements with the EU. Many other arrangements with the EU are linked to it, including some trade privileges. In 2014, a slight majority voted in favor of a similar proposal, and a compromise in the Swiss parliament was found that kept the freedom of movement intact. While a major disruption has been avoided, the focus will quickly shift back to the “institutional framework agreement” with the EU. Essentially it would mean that Switzerland automatically adopts EU rules unless it has specific objections. The Swiss often adopt EU rules to preserve market access. It is not so much about extraterritoriality (applying one’s laws outside of one’s country) as it is in the tragedy of being a small country next to a larger (by magnitudes) economic entity. Brexit represents an opposite strategy. Although the institutional framework agreement has been struck, it has not been validated by parliament, in which a majority seemed elusive. The question is whether the referendum changes the dynamics. We suspect not.

The last formal round of UK-EU trade talks ahead of next month’s summit is launched today. Some progress has been reported but trying to craft the text of an agreement still seems like a stretch. Meanwhile, domestic issues are prominent. First, parliament may seek to wrestle more power from the government over the pandemic. Second, BOE member Tenreyro seemed to play up negative rates even though Governor Bailey had appeared to play it down last week. The latest polls put Labour ahead of the Conservatives for the first time since Labour picked a new leader (Starmer) almost six months ago.

The euro has held the important $1.1600 area but has failed to inspire on the upside. It recorded the session highs so far in the European morning near $1.1650. The highs from the past two sessions are nearer $1.1685. The euro’s recent pullback has not deterred the speculators in the futures markets, where the net and gross long euro positions increased in the week through September 22. The gross long speculative position peaked in mid-August near 266k contracts. After the 16k contract increase in the last reporting period, it stood near 247k contracts. Sterling remains bid through the European morning. It is at a five-day high near $1.2900 and the next resistance is seen about $1.2930 and then $1.30. Part of this reflects sterling’s recovery against the euro. The single currency is at its lowest level in about three weeks, near GBP0.9045.

America

What is an eventful week in the US begins off slowly. The main feature today is the Dallas Fed’s manufacturing survey and the Fed’s Mester speaking at a webinar on economic equality. The highlight of the week is the September employment report at the end of the week. The presidential debate tomorrow night will draw attention even though the number of voters who declare they are undecided and the number who say they could be swayed by the debate are near historic lows, according to some surveys. On the fiscal front, some observers hold out the possibility that Treasury Secretary Mnuchin and House Speaker Pelosi can strike a last-minute agreement. Still, the odds seem to favor a move after the election. Meanwhile, PredictIt.Org participants collectively see about an 85% chance that the Supreme Court nominee Barrett will be confirmed before the election.

The highlight for Canada this week may be the July GDP report on Wednesday. While the US and Canada often report the job data on the same day, this week is not one of them. Canada will issue its September employment report next week. A vote on the government’s budget could happen as early as this week. Mexico’s data highlight for the week is today with the August trade and employment reports. Mexico enjoyed a record trade surplus in July, and while the August surplus may be smaller, it will remain near the record. The surplus appears to be more a function of a compression of imports than a surge of exports. Economists forecast Mexico’s unemployment rate to reach a new cyclical high near 5.6% (5.4% in July) from 2.9% at the end of last year and 2.94% in March.

The US dollar traded between about CAD1.3325 and CAD1.3420 on September 24 and remained within that range ahead of the weekend. It is still in that range today. Initial support now is near CAD1.3360, and a break would signal a test on the lower end of the recent range and possibly bolster confidence that a high is in place. The US dollar rose in four of last week’s five sessions against the Mexican peso for a 5.7% advance. Support is seen near MXN22.20 and then MXN22.00. Once spot stabilizes, we expect the 4.25%-4.30% yield on bills (cetes) to renew its pull. The stabilization of US equities may also ease the selling pressure on both the Canadian dollar and Mexican peso.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, July 6: New Record Number of Covid Cases Doesn’t Curtail Appetite for Risk

FX Daily, July 6: New Record Number of Covid Cases Doesn’t Curtail Appetite for Risk

Overview: A new daily high number of contagions globally has been reported, but the risk-appetites have been stoked. Chinese stocks have been on a tear. The Shanghai Composite rallied 5.7% today to bring the five-day advance to 13.6%. Most other regional markets, including Hong Kong, rallied as well (3.8%). Australia was the main exception, and it pulled back by 0.7%. It is still up a solid 3.4% over the past five sessions.

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

The optimism among investors appears to have evaporated in the face of new US-Chinese tensions, possible delays in the next US fiscal stimulus, and new record virus infections in Australia and Hong Kong. US stocks had pared early gains yesterday, and the high-flying NASDAQ finished lower after setting new record highs.

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, September 8: US Threats to Decouple from China and the Greenback Strengthens

FX Daily, September 8: US Threats to Decouple from China and the Greenback Strengthens

The markets remain on edge. US-China tensions are escalating. Strained Brexit talks are set to resume today. Profit-taking in the tech space has continued. The ECB meeting is around the corner. The MSCI Asia Pacific Index snapped a three-day slide today with most markets moving higher, led by a 1% gain in Australia.

FX Daily, September 09: Investor Anxiety Continues to Run High Despite Some Stability in the Capital Markets

FX Daily, September 09: Investor Anxiety Continues to Run High Despite Some Stability in the Capital Markets

News that the AstraZeneca Phase 3 test had to be stopped to study the adverse reaction of one subject added to the uncertainty of investors amid one of the more significant reversals of risk appetites since March. Equities continued to slump in the Asia Pacific region, with many large markets off more than 1%, led by Australia’s more than 2% decline.

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

A flurry of deals, including the still-evolving Oracle-TikTok tie-up, helped lift equity markets in the Asia Pacific region. South Korea’s Kospi, and Indonesia, which had been battered last week, led the advance. The MSCI Asia Pacific Index rose for the third consecutive sessions. European bourses are little changed while US stocks are firmer.

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

The capital markets are relatively quiet so far today as the FOMC meeting gets underway. Equity markets in the Asia Pacific region, but Japan and Australia advanced, and the regional benchmark rose for the fourth consecutive session. European stocks are a little firmer.

FX Daily, September 16: Dollar Eases Ahead of the FOMC

FX Daily, September 16: Dollar Eases Ahead of the FOMC

Overview: The dollar has been sold against nearly all the world’s currencies ahead of what is expected to be a dovish Federal Reserve, even if no fresh action is taken. The Scandis and Antipodean currencies are leading the majors.

Tags: #USD,Brexit,China,Currency Movement,Featured,newsletter,Switzerland