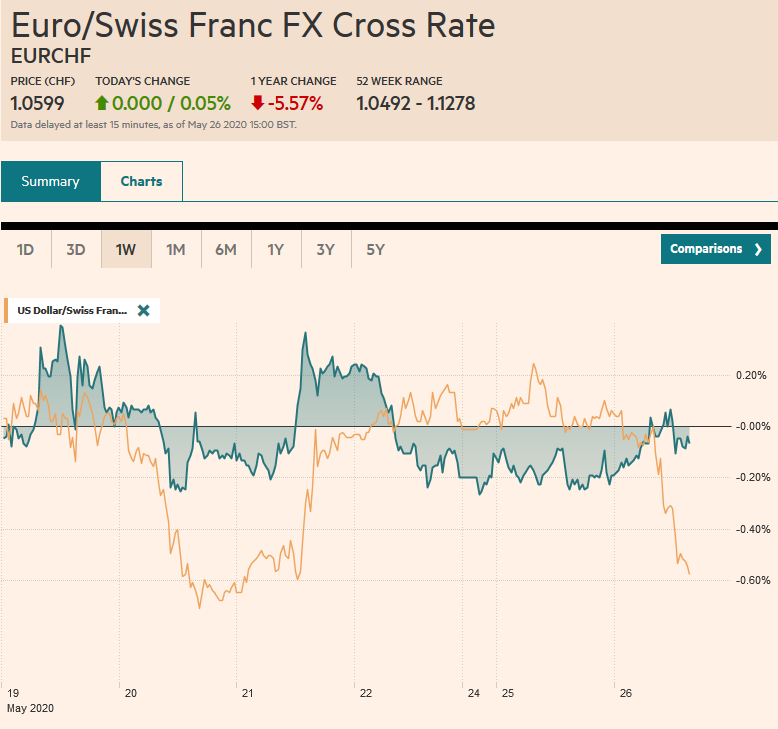

Swiss Franc The Euro has risen by 0.05% to 1.0599 EUR/CHF and USD/CHF, May 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The heightened tensions between the US and China sapped risk-appetites before the weekend, but appear to be missing in action today. Equity markets have rebounded strongly. Nearly all the equity markets in the Asia Pacific region rose (India was a laggard) led by an almost 3% rally in Australia, which was seen as particularly vulnerable to the Sino-American fissure. The Nikkei is approaching its 200-day moving average as it reached the best level since March 5. Europe’s Dow Jones Stoxx 600 is up around 1% after a 1.5% gain yesterday. It is at its best level since March 10. The S&P 500

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, Currency Movement, ECB, Featured, Hong Kong, Mexico, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.05% to 1.0599 |

EUR/CHF and USD/CHF, May 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The heightened tensions between the US and China sapped risk-appetites before the weekend, but appear to be missing in action today. Equity markets have rebounded strongly. Nearly all the equity markets in the Asia Pacific region rose (India was a laggard) led by an almost 3% rally in Australia, which was seen as particularly vulnerable to the Sino-American fissure. The Nikkei is approaching its 200-day moving average as it reached the best level since March 5. Europe’s Dow Jones Stoxx 600 is up around 1% after a 1.5% gain yesterday. It is at its best level since March 10. The S&P 500 is set to gap sharply higher, above 3000, and its 200-day moving average for the first time since March 5. Benchmark 10-year bond yields are mostly firmer (US ~70 bp), but peripheral yields in Europe are softer, which is also consistent with the risk-on mood. Germany sold a two-year bond today with a yield of minus 66 bp and saw the strongest bid-cover in 13 years. The dollar is heavy. Among the majors, the Antipodean and Norwegian krone lead the way. The yen is least favored and is struggling to gain in the softer dollar environment. Emerging market currencies are higher, led by more than 1% gains by the Mexican peso, South African rand, and Polish zloty. Gold is consolidating at softer levels (~$1725-$1735), while oil prices continue to recover. July WTI is probing the recent highs around $34 a barrel. |

FX Performance, May 26 - Click to enlarge |

Asia Pacific

The risk-on mood has not been sparked by any sign of a thaw in the US-Chinese tensions. Indeed, the PBOC set the dollar’s reference rate against the yuan a little higher than the bank models suggested (CNY7.1293 vs. CNY7.1277). It was the second successive fix that was the highest since 2008. Still, the yuan snapped a three-day decline and rose less than 0.1%.

Legislation that makes it easier to crack down on dissent pressured Hong Kong, where the stock market fell more than 5.5% before the weekend, and forward points for the Hong Kong dollar exploded. The Hang Seng stabilized yesterday and gained more than 1.8% today. The 3-month and 12-month forward points are more than double what they were a week ago, but have eased from the extreme readings before the weekend. The situation is far from resolved despite the market moves.

The focus in Japan is on the government’s second supplementary budget for nearly JPY1 trillion. It could be approved by the Cabinet as early as tomorrow and would nearly double the government’s efforts. Japan is lifting the national state of emergency.

The dollar is firm against the yen but held just short of JPY108.00 (last week’s high was ~JPY108.10). There is an option for a little more than $400 mln struck at JPY107.90 that expires today. The market looks poised to challenge the highs in North America today. Note that the 200-day moving average is found near JPY108.35, and the greenback has not traded above it since mid-April. The Australian dollar is punching above $0.6600 and is at its best level since March 9. Its 200-day moving average is found near $0.6660. The dollar peaked against the Chinese yuan at the end of last week near CNY7.1437. It rose against the offshore yuan on the same day near CNH7.1646, just below the high set on March 19.

Europe

The EU responded to Germany’s proposal to take at least a 20% equity stake (~9 bln euros) in Lufthansa by requiring it to give up some slots at airports in Frankfurt and Munich. Meanwhile, the larger focus is on the EC’s proposal for a recovery plan now that the German-French proposal has been countered by Austria, Denmark, Sweden, and the Netherlands. However, the basis for a compromise does appear to exist in the form of some combination of grants, loans, and guarantees and in terms of access. With the European Stabilization Mechanism and the European Investment Bank issuing bonds for which there is a collective responsibility, we are not convinced that an EU bond is a step toward mutualization of existing debt or a fiscal union. In fact, such claims do little more than antagonize the opposition.

The ECB’s Pandemic Emergency Purchase Program (PEPP) has spent a little more than a quarter of its 750 bln euro facility in the first two months. Hints from some officials suggest that this could be expanded as early as next week when the ECB meets. At the current pace, PEPP will be out of funds toward the end of Q3 or early Q4. Talk in the market is that a 250-500 bln euro expansion is possible.

The political controversy of UK’s Cummings violation of the lockdown seems to have little impact for investors. Sterling, the worst performing of the major currencies this month, is bouncing back smartly today, and while the UK stock market was closed yesterday, it is playing a little catch-up today. The benchmark 10-year Gilt yield is a few basis points higher, but faring better than German Bunds and French bonds (where the 10-year yield is now back into positive territory, albeit slightly).

The euro has bounced a full cent from yesterday’s low near $1.0875. The market has its sights on last week’s high just shy of $1.1010 and the 200-day moving average a little above there. The euro has not traded above its 200-day moving average since the end of March. Above there, the $1.1065 area corresponds to about the middle of this year’s range. Sterling is near its best level in a couple of weeks. After finding support near $1.2160 in the past two sessions, it bounced to about $1.2325 today to toy with the 20-day moving average (~$1.2315). The short-covering rally has stretched the intraday technical readings, and it may be difficult for the North American session to extend the gains very much before some consolidation.

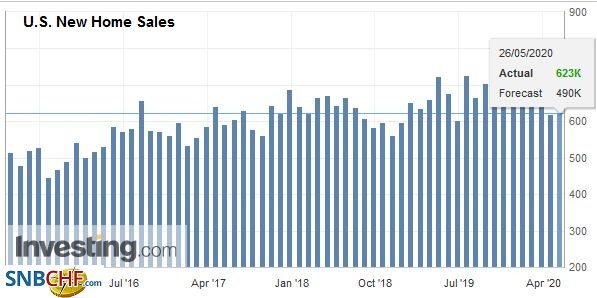

AmericaThe US reports some April data (Chicago Fed’s National Economic Activity Index) and new home sales. The reports typically are not market-movers even in the best of times. Moreover, it is fully taken on board that the economy was still imploding. May data is more interesting. The Dallas Fed’s manufacturing survey and the Conference Board’s consumer confidence surveys will attract more attention and are expected to be consistent with other survey data suggesting the pace of decline is moderating. This is thought to be setting the stage for a recovery in H2. |

U.S. New Home Sales, April 2020(see more posts on U.S. New Home Sales, ) Source: investing.com - Click to enlarge |

Canada’s economic diary is light today, and Mexico is expected to confirm that Q1 GDP contracted by 1.6%. Yesterday Mexico surprised by with a nearly $3.1 bln trade April deficit. The median forecast in the Bloomberg survey was for a $2 bln trade surplus. Apparently, none of the economists surveyed expected a deficit. Exports fell by nearly 41%, and imports tumbled by 30.5%. Many economists are revising forecast for Mexico’s GDP lower toward a double-digit contraction this year.

Nevertheless, the peso is flying. It is the strongest currency here in May. The 1.75% gain today brings the month’s advance to a dramatic 9%+ gain. The US dollar is near MXN22.10, giving back about half of this year’s appreciation. A break of the MXN22.00 area would target the MXN21.30 area. The intraday momentum indicators are stretched. The US dollar is heavy against the Canadian dollar as well. It is approaching the lower end of its two-month trading range near CAD1.3850. The next important chart point is around CAD1.3800. Here too, the greenback’s slide in Asia and Europe is leaving intraday technicals indicators stretched as North American dealers resume their posts.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, April 22: Investors Catch Collective Breath, but Sentiment remains Fragile

FX Daily, April 22: Investors Catch Collective Breath, but Sentiment remains Fragile

Overview: Risk-appetites appear to have stabilized for the moment. Most equity markets are higher. Japan and Malaysia were exceptions, but the MSCI Asia Pacific Index rose for the first time this week. In Europe, the Dow Jones Stoxx 600 is recouping about a third of yesterday’s loss.

FX Daily, May 18: Yuan Slumps as US-Chinese Tensions Rise

FX Daily, May 18: Yuan Slumps as US-Chinese Tensions Rise

Overview: Despite somber warnings that the US economic recovery can stretch to the end of next year, investors have begun the new week by taking on new risks. Most equity markets in the Asia Pacific region rose, with Australia leading the large bourses with a 1% gain. India was an outlier, suffering a 2.4% loss, and Taiwan’s semiconductor sector was hit, and the Taiex fell 0.6%.

FX Daily, May 19: Optimism Burns Eternal

FX Daily, May 19: Optimism Burns Eternal

Overview: Hopes for a vaccine and a German-French proposal to break the logjam at the EU for a joint recovery effort helped propel equities higher yesterday. There was strong follow-through in the Asia Pacific region, where most markets advanced by more than 1% today. However, the bloom came off the rose, so to speak, in Europe. After a higher opening, markets reversed lower, and the Dow Jones Stoxx 600 is off about 0.75% in late morning turnover.

FX Daily, May 22: US-China Escalation Sinks Hong Kong and Hits Risk Appetites

FX Daily, May 22: US-China Escalation Sinks Hong Kong and Hits Risk Appetites

Overview: The US has ratcheted up pressure on China on several fronts and has sapped risk appetites ahead of the weekend. Equity markets are lower across the world. Even in India, where the central bank unexpectedly cut the repo rate 40 bp, shares fell 0.7%. It was Hong Kong’s 5.5% that led the region lower. Europe’s Dow Jones Stoxx 600 is off around 1% in late morning turnover to pare this week’s gain to about 2.5%.

FX Daily, February 3: Inauspicious Start to the Year of the (Flying) Rat

FX Daily, February 3: Inauspicious Start to the Year of the (Flying) Rat

Overview: The Year of the Rat is off to an inauspicious start as apparently a fly rat (a bat) virus has jumped to humans. China’s markets re-opening amid much fanfare, and the Shanghai Composite dropped 7.7%, which is about what the futures in Singapore had anticipated. Several other markets in the region (Japan’s Nikkei, Australia, Singapore, Taiwan, and Thailand) fell by more than 1%.

FX Daily, February 13: Surprise? China Undercounts Afflictions and Fatalities, Curbs Risk Taking

FX Daily, February 13: Surprise? China Undercounts Afflictions and Fatalities, Curbs Risk Taking

Overview: There is one overriding driver today, and that is the incorporation of CAT scan diagnoses of the virus in Hubei, ground-zero. This follows the arrival of WHO officials into China a couple days ago. Not only have the cases jumped, but so did the number of deaths. It plays on fears that China’s figures are not reliable. But it is not just China.

FX Daily, April 16: Markets Brace for another Jump in US Weekly Jobless Claims

FX Daily, April 16: Markets Brace for another Jump in US Weekly Jobless Claims

Overview: Equity losses in the US appeared to drag most Asia Pacific markets lower today, with China and India the notable exceptions. European bourses are higher, and the only energy sector is a drag on the Dow Jones Stoxx 600, which is around 1% higher in late morning turnover, while US shares are also trading firmer. Asia Pacific 10-year benchmark yields eased.

FX Daily, April 21: Oil Drilled Below Zero, Equity Rally Stalls, Greenback Advances

FX Daily, April 21: Oil Drilled Below Zero, Equity Rally Stalls, Greenback Advances

Overview: Oil’s wild ride has been joined by two other developments that are keeping investors off-balance. First, reports suggest that North Korea’s Kim Jong-Un maybe in critical condition after surgery. He apparently was absent from last week’s events celebrating his grandfather.

Tags: #USD,$CNY,Currency Movement,ECB,Featured,Hong Kong,Mexico,newsletter