Let’s revisit a point that came up in passing, in the Silver Doctors’ interview of Keith. At around 35:45, he begins a question about weights and measures, and references the Coinage Act of 1792. This raises an interesting set of issues, and we have encountered much confusion (including from one PhD economist whose dissertation committee was headed by Milton Friedman himself). Gold, Paper, and Redeemability Back in the 18th century, three facts were obvious and not questioned. One, gold and silver are money. Two, the paper receipt evidencing the deposit of money is not, itself, money. And three, depositors had the right to get their money back plus interest. So many steps of adulteration of money—and mainstream thinking about it—have occurred since then, that

Topics:

Keith Weiner considers the following as important: 6a.) Keith Weiner on Monetary Metals, 6a) Gold & Bitcoin, Basic Reports, basket of commodities, dollar price, Featured, gold basis, Gold co-basis, irredeemability, newsletter, numeraire, price fixing, redeemability, silver basis, Silver co-basis, unit of measure

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Let’s revisit a point that came up in passing, in the Silver Doctors’ interview of Keith. At around 35:45, he begins a question about weights and measures, and references the Coinage Act of 1792. This raises an interesting set of issues, and we have encountered much confusion (including from one PhD economist whose dissertation committee was headed by Milton Friedman himself).

Gold, Paper, and Redeemability

Back in the 18th century, three facts were obvious and not questioned. One, gold and silver are money. Two, the paper receipt evidencing the deposit of money is not, itself, money. And three, depositors had the right to get their money back plus interest.

So many steps of adulteration of money—and mainstream thinking about it—have occurred since then, that these points are as clear as mud today. Just ask any economist what money is, or ask Google for pictures of money. It will give you only green pieces of paper. There is no right to redeem paper notes today. If you have a dollar bill, that’s the buck and it stops at itself.

We have addressed number one many times. Money is a commodity because only a physical good is final payment. Anything else (yes, including bitcoin) is pending the delivery of something physical. Gold and silver are money, whereas other commodities are not, because of their stocks to flows and bid-ask spreads.

Number two is confusing, because the dollar is not redeemable today. The paper note is no longer any kind of receipt. Back when it was redeemable, it was clear that the paper receipt was not the thing for which it redeemed. Like a coat check ticket is not a coat. Now that the paper receipt is treated as an end in itself, there is no longer a distinction between a receipt for money vs. money itself. So people understandably—if wrongly—think of the paper as the money itself.

And that segues into number three, the note does not represent a deposit of gold and therefore does not entitle you to get gold back. So most people tend to reify it. The government’s act of looting the gold of the savers, and making the paper receipts into irredeemable credit, would seem to have worked beyond President Roosevelt’s wildest dreams. It has had the benefit of creating a sort of NewThink. It has actually made people unable to conceive of a difference between a debt vs. the money used to pay said debt.

The Price of GoldWe have written a lot about this too. So we want to move on to the focus of this article. It is simple to say, but harder to wrap your mind around. Back in 1792, the Coinage Act did not fix the price of gold at $20 (approximately) per ounce. The very concept of price implies a unit of measure, a numeraire. In the late 18th century, that was gold or silver. Prices were therefore expressed in gold. The dollar was merely a defined weight of gold. One does not ask, “How much does the ounce weigh?” Similarly one did not ask, “What is the price of gold?” OK, OK, let’s ask and answer that. Here is a 5000 year chart of the price of gold. Unfortunately the 1792 Act contributes to this confusion. It defined the dollar also as a fixed weight of silver. Rather than contemplate two numeraires, it easy for us today to look back retrospectively and think of $20 an ounce of gold or $1.10 (approximate) an ounce of silver as their respective prices. |

Gold Price(see more posts on gold price, ) - Click to enlarge |

The Numeraire of Gold

In 1792, there was not such a thing as a dollar which existed independently from gold and silver. The unit dollar was nothing more than a weight of gold or silver. At the time, the question of a price of gold in terms of a separate currency (other than silver) would have been meaningless.

Today, the dollar is the irredeemable credit paper issued by the Federal Reserve. So of course there is an exchange rate of dollar to gold and to silver. This exchange rate changes over time, like any other price (and any attempt to fix it would be doomed to fail).

The conceptual problem comes from trying to superimpose this present reality anachronistically onto the context of 1792. Thus, the confusion exhibited by that pedigreed PhD monetary economist. He thinks that in 1792, the government fixed the price of gold. Or, expressed differently, that the government fixed the value of the dollar in terms of gold. He sees no problem with doing the same today (and wants to include other commodities, in the basket with gold).

The Standard of Gold

In 1792, the US government was acting like a Bureau of Weights and Measures (yes, we know the actual Bureau of this name was created nearly a century later). Everyone was clear that you could deposit gold and silver at a bank. And then the bank had to give it back to you under the terms of the deposit contract. The law merely standardized the units of money deposits.

For example, Mike Moneybags brings his sacks of gold coins to the bank. He then negotiates with Walter Workingman to do a job. Both have the same understanding of what $20 means (i.e. roughly one ounce of gold).

This is analogous to connecting your phone to a Wi-Fi hotspot. Everyone (well, the engineers who design these products) has a common understanding of what Wi-Fi means in terms of frequency, protocol, number of bytes in a packet, etc.

A standard unit for money or computer networking allows for compatibility, interoperation, and ultimately for the development of a large market. No one has to puzzle out if their phone is using the 1,500-byte version of Wi-Fi, but it’s not working because the hotspot is using the 1,501-byte Wi-Fi.

And, after 1792, no one had to wonder if the other party’s bank was going to pay a different weight of gold for a $20 debt. Also, when reading a company’s balance sheet, no one had to wonder how much was $2,000—i.e. how much gold. The benefit of standardization cannot be overstated.

In our opinion, there is no need for the government to mandate such a standard (which, like all decrees is ultimately backed by a gun). Computer standards are not forced on unwilling companies and consumers. It just makes sense for the affected groups to form a standards body and come to agreement.

However, making a standard such as the 1792 Act did is basically benign (other than that it fixed the ratio of gold to silver, which had far-reaching and long-term consequences that ultimately culminated in the creation of the Fed in 1913, which story will have to wait for another day).

Today, of course, there are already two perfectly adequate ways to measure an amount of gold. We can use troy ounces or grams (Monetary Metals prints account statements in ounces). There does not seem to be a compelling need for a new monetary unit of weight of gold.

What would not be benign is a law to fix the exchange rate between the dollar and gold (or the Fed to try to fix or manage it). Or a basket of commodities, including gold. Everywhere and always (to appropriate Friedman’s phrase for a proper context), price-fixing schemes fail. Even when the central bank has a printing press, and would seemingly have the power to print an unlimited quantity of its currency to keep it down. Here’s looking at you, Swiss National Bank. Whatever form the new gold standard will take, a price-fixing scheme to the failing paper currencies will not be that form.

Money Is a Moral Institution

Anyways, this leads us to frame the issue in moral terms. Yes, at root, the questions of money and credit are moral questions: what is honest, what has integrity, and what serves justice.

The quantity of the stuff we call “money”, the ratio of a bank’s vaulted gold to its deposit liabilities, the right rate of interest, etc. are all to be determined honestly and fairly in an open and free market. People should have the right, but not the obligation, to deposit their gold and earn interest on it. Or hoard it under the mattress. Or pay a vault to store it and keep it safe. Companies who borrow it—and the financial intermediaries who make borrowing efficient—owe a duty of care including full and transparent disclosure as to the use of proceeds.

We propose four criteria for honest credit: (1) the lender knows he is lending his money, (2) the lender agrees to lend, (2) the borrower has the means to repay, and (4) the borrower has the intention. Honest defaults can happen, if there is a mistake in execution or the market changes. But it is an act of counterfeiting to take gold from savers, to spend it, and expect more to service the original debt. This is not a proper loan.

Generally, a borrower should be financing a productive asset, such as a factory.

In other words, nearly the opposite of what we have today. The saver does not know he is lending, thus insists that if he holds a paper dollar bill he has money. Few savers would agree to fund to the welfare state, if they did know. And of course, the government issues this ever-increasing pile of irredeemable paper currency in order to feed its ever-growing appetite for welfare programs, and subsidies by other names.

We will close with a quote from Ayn Rand:

“He [man] is free to make the wrong choice, but not free to succeed with it. He is free to evade reality… but not free to avoid the abyss he refuses to see.”

Supply and Demand

The price of gold dropped, but not calamitously. From $1514 to $1459, or -$55. The price of silver dropped. Calamitously. From $18.08 to $16.75, or -$1.33. -3.6% vs 7.4%. Once again, silver proves to be volatile relative to gold.

In standard vernacular, the metals lost purchasing power this week. Purchasing power can be thought of as the amount of groceries you could buy, if you liquidated an asset. If you think of an asset as a store of purchasing power, then there is some amount of groceries contained therein. And this week, some of groceries leaked out of gold. An alarming amount poured out of silver.

As an aside, such market moves are offered as proof that gold is not money, that the dollar cannot be measured in gold. To which, we say, “Hah! The dollar rose this week from 20.5 to 21.3 grams of gold.” Either way, there is volatility. One can say this proves that gold is volatile, or that the dollar is. But either way, one is not making an argument as to which is the objective measure of value. That argument comes from stocks to flows and marginal utility.

We will look at what happened this week, below under the respective sections for gold and silver.

Groceries (i.e. purchasing power) also dropped out of Treasury bonds. They even leaked slowly out that value store-celèbre: bitcoin. Some of them spilled into US equities. But even the euro lost some purchasing power relative to the dollar.

As an aside, in physics there is a law that says there must be conservation of energy in a closed system. Energy can be transferred from one body to another. Or change in form from kinetic to potential. But it does not go come into, or go out of existence.

In purchasing power, unlike in physics, there is not conservation of groceries. Groceries, it seems, can come into existence if all or most assets go up. And can go out of existence if they go down. Everyone loves when groceries are created (seemingly) ex nihilo, and hates when they (appear to) disappear into the aether from which they (apparently) sprang.

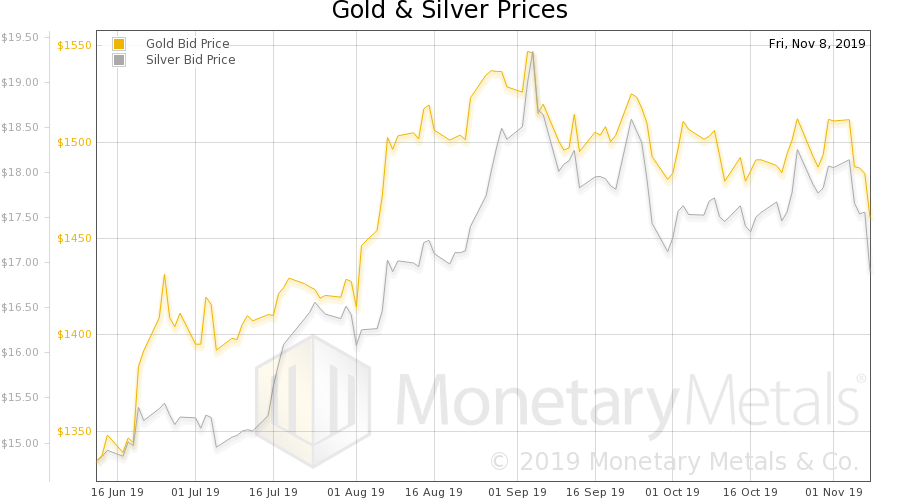

Gold and Silver PricesAnyways, something unusual happened this week. We will look at that the only true picture of the supply and demand fundamentals of gold and silver. But, first, here is the chart of the prices of gold and silver. |

Gold and Silver Prices(see more posts on gold price, silver price, ) - Click to enlarge |

Gold to Silver RatioNext, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio (see here for an explanation of bid and offer prices for the ratio). The ratio rose sharply this week. |

Gold to Silver Ratio(see more posts on gold silver ratio, ) - Click to enlarge |

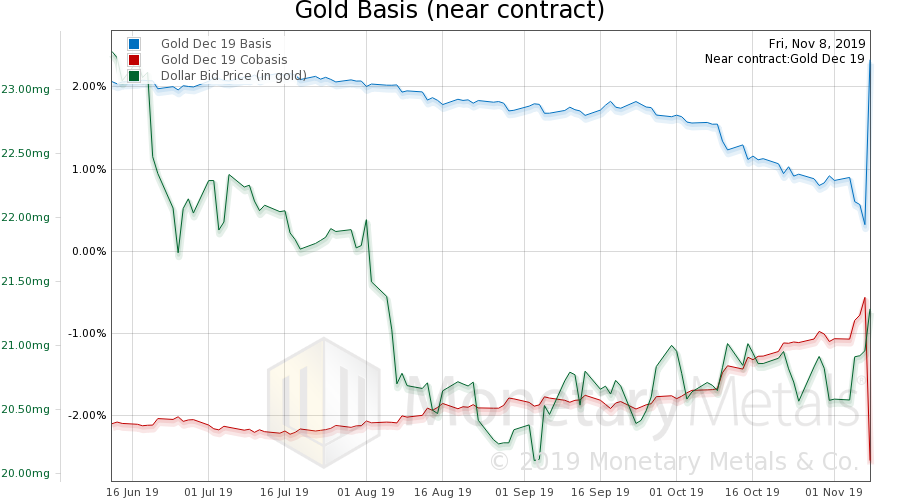

Gold Basis and Co-basis and the Dollar PriceHere is the gold graph showing gold basis, cobasis and the price of the dollar in terms of gold price. It rose this week. With the rise in the price of the dollar (i.e. fall in the price of gold) Monday through Thursday, there is a clear increase in scarcity (i.e. rise in cobasis). Friday, is something else. We see a massive jump in the basis, and drop in the cobasis. Remember, basis is a spread. It is the difference between future and spot prices. A rising basis means the price of the future is higher, relative to spot. Basis is how we measure abundance, and cobasis is how we measure scarcity. The reason is that a high-enough basis means there is enough of the commodity that the warehousemen can buy it, to carry it in the warehouse. That is buy spot and simultaneously sell a futures contract. They pocket this spread, minus the cost of storage and insurance, and interest. If this spread is too small (or negative), then the commodity is too scarce and the market is signaling the warehousemen not to carry it (or even to decarry it, in the case of a positive cobasis). So on Friday, it appears that the basis abruptly jumped. That would mean gold suddenly became more abundant to the market. Since the price, fell that would mean lots of physical metal was dumped on the market. |

Gold Basis and Co-basis and the Dollar Price(see more posts on dollar price, gold basis, Gold co-basis, ) - Click to enlarge |

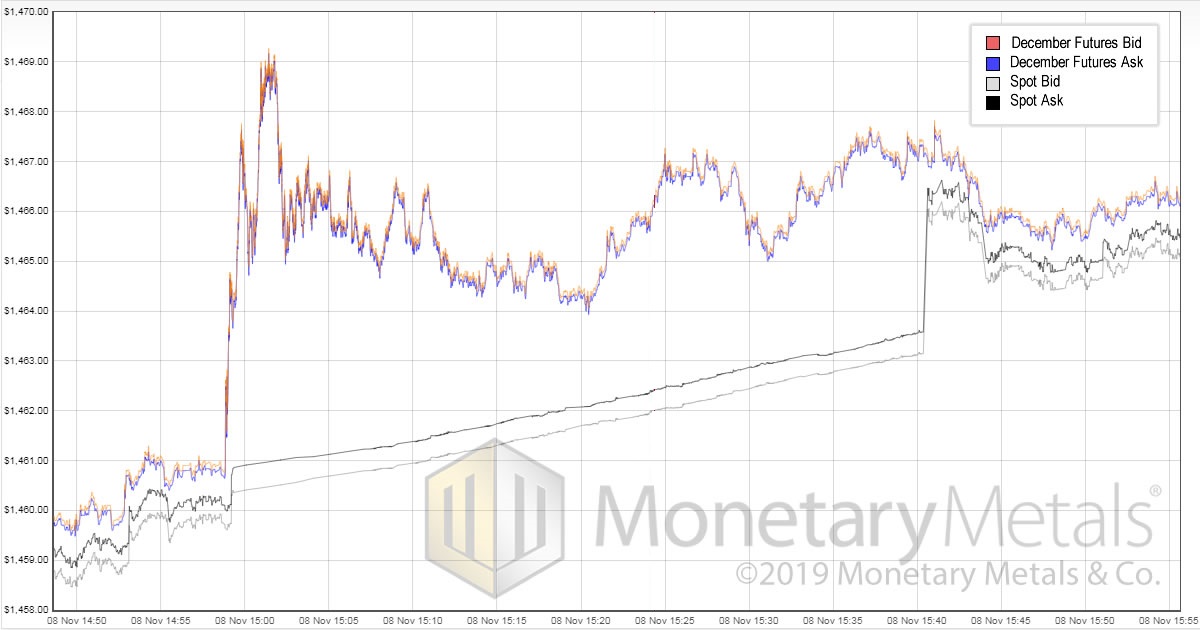

| Let’s take a look at the actual bids and offers for an hour period on Friday. The period of interest is from just before 3:00pm until just after 3:40.

There are two take-aways form this. One, always drill down until you have a clear picture. And do not assume from high level or macroeconomic aggregate data that you know what is the cause, and what is the effect. Especially if something which normally moves smoothly as the basis does, changes behavior, and most especially if it moves in the opposite direct expected. Two, this is either a data or networking glitch. Either the data is wrong, or the network somehow delayed or otherwise corrupted it. The spot price looks unnatural, and clearly is not in sync with the futures price the way it normally is. Note that this period includes the PM gold fix. We must reject this data. The Monetary Metals Gold Fundamental Price, was down $4 this week (to Thursday, which we will treat as the end of the gold week due to the above data problem), to $1,481. |

Monetary Metals Gold Fundamental Price - Click to enlarge |

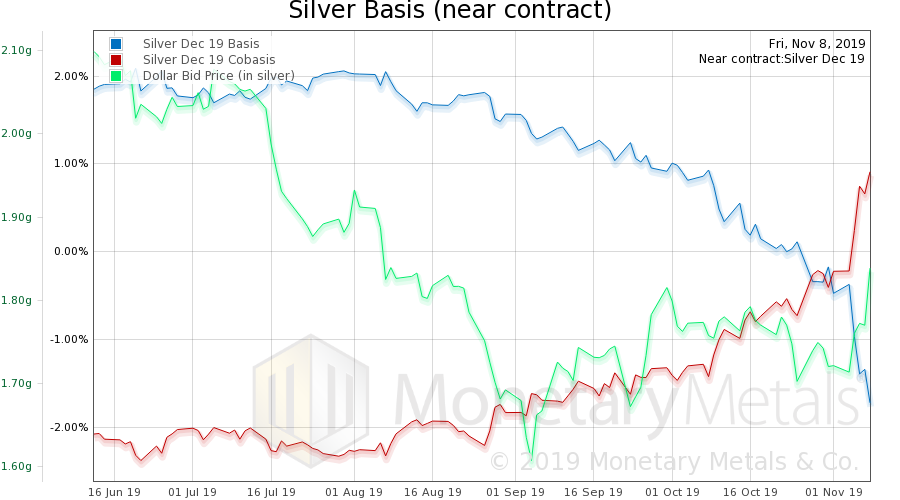

Silver Basis and Co-basis and the Dollar PriceNow let’s look at silver. The problem we saw in gold did not show up in silver. The silver data is fine. The December cobasis rose very sharply again this week, though the silver basis continuous rose a much more modest amount. This is the temporary backwardation of the expiring contract, not a strong signal of market fundamentals. The Monetary Metals Silver Fundamental Price fell by just 18 cents, a little move in a big price move week, to $16.47. What happened is that the market price (mostly) caught down to the fundamentals. |

Silver Basis and Co-basis and the Dollar Price(see more posts on dollar price, silver basis, Silver co-basis, ) - Click to enlarge |

© 2019 Monetary Metals

Tags: Basic Reports,basket of commodities,dollar price,Featured,gold basis,Gold co-basis,irredeemability,newsletter,numeraire,price fixing,redeemability,silver basis,Silver co-basis,unit of measure