US Banks are seeing a larger number of new entrants into the industry. Chime, a mobile-only bank, has opened two million online checking accounts and is adding more customers each month than Wells Fargo or Citibank. Firms from outside traditional consumer banking including Square, Goldman Sachs (Marcus), and Robinhood are entering the industry as well. The consulting firm CG42 said in a recent report on the vulnerability of retail banking that it expects the ten largest banks to lose 4 billion in deposits over the next year. Applications for and approvals of FDIC deposit insurance are at a recent high, with fifteen approvals in 2018 and eight so far this year, shown in the chart below. Despite banking’s 20 year decline in the number of banks, the

Topics:

Josh Reini considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| US Banks are seeing a larger number of new entrants into the industry. Chime, a mobile-only bank, has opened two million online checking accounts and is adding more customers each month than Wells Fargo or Citibank. Firms from outside traditional consumer banking including Square, Goldman Sachs (Marcus), and Robinhood are entering the industry as well. The consulting firm CG42 said in a recent report on the vulnerability of retail banking that it expects the ten largest banks to lose $344 billion in deposits over the next year.

Applications for and approvals of FDIC deposit insurance are at a recent high, with fifteen approvals in 2018 and eight so far this year, shown in the chart below. Despite banking’s 20 year decline in the number of banks, the floodgates are seeming to be open for a new wave of digital-first banks to pursue new licenses. While the new banks may not outnumber the 1,500 banks that have closed since 2009 – their appeal to a new wave of consumers represents a substantial threat to the 0.2% of megabanks that hold more than two-thirds of industry assets . |

Recent Spike in FDIC Approvals, 2009-2019 Source: FDIC - Click to enlarge |

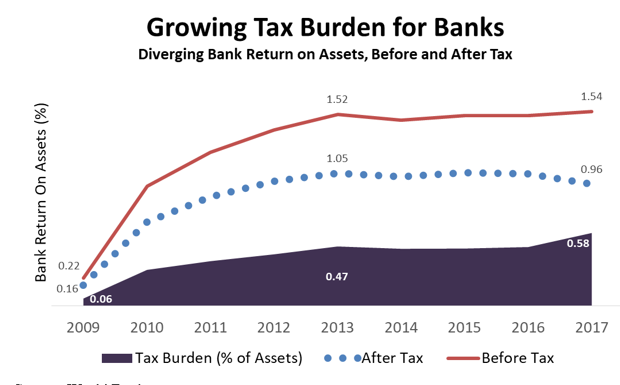

Paving the Way for New BanksAs the demographic of the United States shifts younger, customers have started to move away from reliance on traditional brick and mortar branches and instead prefer app-based services with lower fees . This has led to an erosion of entrance and exit costs as the need to build buildings and pay tellers is eliminated. Additionally, venture capitalists are setting records with funding of “neo-banks” , investing $2.5 billion through the second quarter of 2019 – for reference, the previous high was only $2.3 Billion in all of 2018. Both the shift in preferences away from physical branches and the availability of funding have paved the way for new banks to enter the market. A paper entitled Competition in Banking by Carol Ann Northcott published in 2004 lists the ways that banks differ to include reputation, product offerings, and the extensiveness and location of their branch networks. Scandals such as Wells Fargo’s “Eight is Great” phony account scandal and the Financial Crisis of 2008 have tarnished the reputation of big banks and, along with the disappearing significance of branches, removed the mystique of the incumbent banks. Disappearing Tax Advantage for Incumbent BanksUnder Section 172 of the Internal Revenue Code, corporations are able to carry forward Net Operating Losses (NOLs) indefinitely, minimizing tax liability. In the chart below using data from the World Bank, before-tax (red line) and after-tax (blue dots) return on assets are diverging and the tax burden (purple, calculated as the difference between before and after-tax ROA) is growing since the Great Recession in 2008. Furthermore, in 2017 the Tax Cuts and Jobs Act (TJCA) put additional limitations on NOL deductions, serving to increase the tax liability for banks. With Net Operating Loss (NOL) tax exemptions rolling off for incumbent banks, their cost advantage is reduced – putting them on a more even playing field with new entrants. While the rules surrounding NOLs exist to provide protection from “excessive hardships from tax based upon an arbitrary annual accounting,” they can artificially prop up inefficient firms and stifle competition. As banks become profitable again following the Great Recession and lose their tax advantage over new banks, opportunity for new entrants grows. |

Growing Tax Burden for Banks, 2009-2017 Source: World Bank - Click to enlarge |

Implications for Consumers

Banks contribute greatly to growth by facilitating production in other industries and promoting capital accumulation through the supply of credit. As competition for customers grows, banks are forced to often lower their profit margin or lose their market share to rival banks. In this situation, a larger quantity of credit will be supplied at the lower price. A paper by Besanko and Thakor examines loan and deposit markets and finds that loan rates decrease and deposit rates increase as more banks are added to the market. These findings support the theoretical prediction that a more competitive environment results in the larger quantity of credit is supplied at a lower price.

As more banks enter the market and capture market share, incumbent firms lose their power in the market. Shining the light on a potential pitfall of a more competitive market, Northcott finds that a banking system that exhibits some degree of market power may improve credit availability of certain firms and provide incentives for banks to screen loans which aids the efficient allocation of resources. In addition, she finds that market power may contribute to stability by providing incentives that mitigate risk-taking behavior and providing incentives to screen and monitor loans. Guzman also finds that the problems of the loan-borrower relationship may be exacerbated by more competitive market structures where information is not costlessly obtainable by the bank. Northcott finds no consensus in the literature on the optimal competitive structure, but it is clear that, for the moment, entry costs for retail banks are falling and competition is growing in the digital age.

Tags: Featured,newsletter