After last week’s flurry of events, market activity is set to slow over the next three weeks. But what a flurry of events it was. A new NAFTA apparently has been agreed, and it is set to be approved by the US House of Representatives next week and the Senate early next year. The US and China struck an agreement that will get rid of the immediate tariff threat and unwind half of the punitive tariffs in exchange for a commitment to buy twice the amount of agriculture good next year than it at its peak a couple years ago. China also promises to be more protective of property rights and has already taken some formal steps in that direction. The precise details appear less important to investors than the broad idea that there is a de-escalation of the trade conflict

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Bank of England, Bank of Japan, Boris Johnson, Featured, Federal Reserve, newsletter, PRC, Riksbank

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

After last week’s flurry of events, market activity is set to slow over the next three weeks. But what a flurry of events it was. A new NAFTA apparently has been agreed, and it is set to be approved by the US House of Representatives next week and the Senate early next year. The US and China struck an agreement that will get rid of the immediate tariff threat and unwind half of the punitive tariffs in exchange for a commitment to buy twice the amount of agriculture good next year than it at its peak a couple years ago. China also promises to be more protective of property rights and has already taken some formal steps in that direction. The precise details appear less important to investors than the broad idea that there is a de-escalation of the trade conflict between the two largest economies. Boris Johnson led the UK Tories to a smashing victory, and their majority is the largest since Thatcher’s 30-years ago. The Federal Reserve recognized that the short-term funding market was still at risk and increased the funds it will make available to cover to the turn (of the year) to nearly $500 bln. A more investor-friendly set of outcomes is difficult to imagine.

This week’s highlights include the flash PMIs and several central bank meetings. On balance, however, not much will be added to our information set. Sweden’s Riksbank may be an exception. The Bank of Japan, the Bank of England, Norway’s Norges Bank and the Riksbank hold policy meetings on December 19. Sweden’s central bank is the only one that is likely to do something, and that something is probably a 25 bp rate hike that would bring the repo rate by to zero. It has been negative since early 2015. Ever since the hike in January, it has seemed the central bank was looking for an opportunity to hike again.

Value is seemingly being destroyed by Swedish industry. Value-added has fallen by 3% in October year-over-year. This year’s average is about 1.2%, a third of 2018’s 3.6% average. Other indicators, like the PMI, warn of downside risks, as well. Nevertheless, the Riksbank appears willing to seize on the slight uptick in the key inflation measure (CPI-adjusted for fixed income mortgages) to 1.7% in November from 1.5%.

The euro had trended higher to reach a decade-old high against the Swedish krona in the first half of October near SEK10.9350. Since then, it has slumped in eight of the last nine weeks, in which time, it has met the (61.8%) retracement objective of this year’s rally. The technical indicators are stretched, suggesting the krona’s strength begin moderating.

Norway’s monetary tightening cycle began August last year with a 25 bp hike in the deposit rate to 75 bp. Since March, Norges Bank has followed a pattern. Hike by 25 at one meeting and pause, raising rates at every other meeting. There have been three through September, and the pause came in October. For the pattern to remain intact, it would need to hike rates this week, but expectations for such a move are practically non-existent. Nevertheless, the tightening cycle does not appear over, and the market seems to be discounting a hike in Q1 20.

The election and Brexit have overshadowed an economy that has been losing momentum. The November composite PMI matched its cyclical low of 49.3. Both the manufacturing and service components were below the 50 boom/bust level in November (48.9 and 49.3, respectively). The labor market is stalling. The claimant count is rising. It rose to 33k in October, the highest in two and a half years. Earnings growth for employees appears to have peaked in July (3.9%) and fell back in August and September, reaching 3.6%. It is expected to have slipped lower in October.

On the other hand, retail sales should bounce back from the decline in October, when the headline fell by 0.3% and excluding petrol, eased by 0.1%. However, because last November’s surge (1.1% on the headline and 1.3% respectively) will be dropped, the year-over-year pace will likely continue decelerating. Lastly, prices consumer prices are expected to be little changed on a year-over-year basis at 1.5% on both the headline measure (CPI) and preferred measure that incorporates owner-occupied housing costs. The core rate, which excludes food and energy, may slip ease from 1.7% in October.

The market sees only a slight chance of a rate cut from the Bank of England. There were two dissents at the last meeting favoring an immediate, but they appear to have been unsuccessful in convincing others on the monetary policy committee. The calendar also works against a cut in the coming. After this week’s meeting, Carney will hold one more meeting on January 30, the day before he steps down. It seems kind of awkward to arrange a cut as he walks out the door.

But it may be equally awkward for his successor to cut rates at his first meeting (March 26). Draghi engineered a rate cut quicker, unwinding Trichet’s (arguably a faux pas) hike within days of being in office, and it was the first of many reasons he is no longer called a Prussian Roman. Perhaps, in the current period, the anti-inflation credentials of a central banker may mean less than, say, before the Great Financial Crisis, but it does not make for good optics.

Lagarde provided a sober but optimistic framing at her first press conference as President of the ECB. It is not that the economic condition is good or warrants anything less than extraordinary monetary policy, but rather on the margins, things have gotten less bad. This is likely to be reflected in the flash PMI on December 16. The manufacturing PMI for the EMU has risen for the past two months, but at 46.9 in November, it remains well below the 50. A small rise could lift it to its highest level in H2. The service PMI wobbled recently. It rose in October but slipped back in November. A slight increase is anticipated in December to close the year. These developments should translate into a small gain for the composite, which has been stuck at 50.6 for two months.

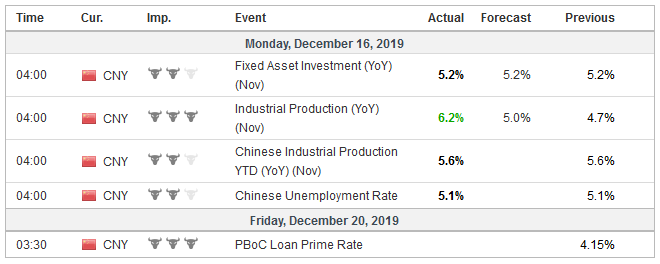

ChinaWhile China’s economic and financial challenges are well represented in the popular press, there seems to a sense about country specialists, rather than the generalists, that conditions are stabilizing. It should be reflected in the November industrial production and retail sales reports. The year-over-year growth of industrial output slowed below 5% for the first time since 2002 in recent months and stood at 4.7% in October. At 7.2% year-over-year, October retail sales matched the slowest pace since 2003. A small rebound after slowing from 7.8% in September is expected. However, without dramatic structural reforms, it is difficult to imagine a strong re-acceleration of the economy. Beijing seems to recognize that slower growth may be necessary to accept if the imbalances in the economy can be ameliorated. Neither monetary nor fiscal policy has been deployed aggressively. The PBOC has another opportunity when it set the Loan Prime Rate on December 20 (one-year at 4.15%). It has been cut twice since the facility was introduced, and each time it was by five basis points. |

Economic Events: China, Week December 16 - Click to enlarge |

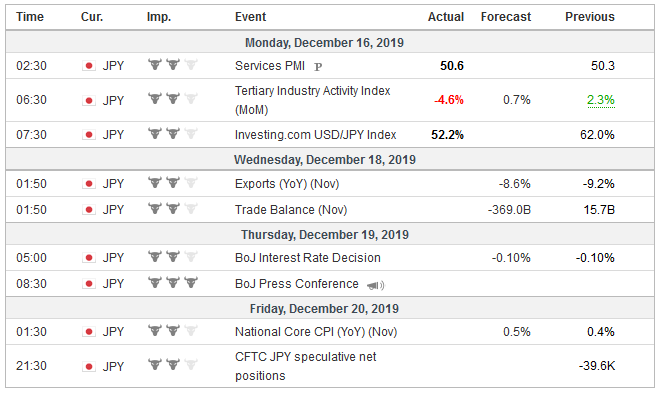

JapanThe Bank of Japan meets on December 19, and the world’s third-largest economy appears to be suffering from a relatively deep contraction this quarter (-0.6%-0.7% quarter-over-quarter). This is partly a result of the tax hike that brought forward consumption and the disruptive typhoon. Trade is also a drag, and exports have not risen on a year-over-year basis since November 2018. Sentiment among large businesses weakened and by more than expected in the December Tankan survey. Prime Minister Abe’s government is drafting a large supplemental budget, and this may also take the pressure off the BOJ. |

Economic Events: Japan, Week December 16 - Click to enlarge |

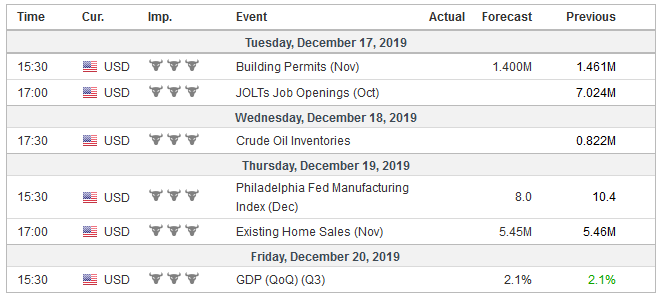

United StatesThirteen of the 17 Fed officials expect the economic data to be such that the target rate can be left at its present 1.50%-1.75% for all of 2020. The other four see one hike as likely being appropriate. The market leans the other way. The implied yield of December 2020 fed funds futures rose a single basis point last week to 1.32%. Currently, the fed funds effective average (which is what determines the settlement of the futures contracts) is 1.55%. The market has mostly priced in a cut. We have seen this before. At the end of last year, the implied yield of the December 2020 contract about 2.20%. At the December 2018 FOMC meeting, the median forecast was for the fed funds target to be 3.00%-3.25%. The economic data in the coming days, and really for the rest of the year, simply does not have the heft to change understandings of the US economy. One of the most striking features currently is the divergence in views. Recall that the PMI and ISM pointed in different directions. The Atlanta and NY Fed’s GDP trackers have sustained a stark contrast. The Atlanta Fed says Q4 is tracking 2%, and the NY Fed says it is on a path for a 0.7% annualized rate. The Atlanta Fed suggested that the disappointing retail sales offset some positive developments government spending, inventories, and exports leaving the tracker unchanged on the week. The NY Fed’s estimate ticked ever so slightly higher and noted that the “positive surprise from retail sales” was the main driver. Ultimately we suspect the Fed will look through soft Q4 GDP but a weak Q1 20 GDP, which the NY Fed’s model projects could reach the “material” threshold of which Powell spoke. US data is not only second-tier but will also likely be divided. For example, housing starts are expected to have increased in November, but permits probably fell. December’s Empire State Manufacturing survey is forecast to edge higher, but the Philly Fed survey is expected to have slipped after ending a three-month decline in November. Industrial output is likely to bounce back from the 0.8% decline in October, but this is about the end of the GM strike and not portending a cyclical upturn. Revisions to Q3 GDP will be too historic to matter to what will likely be holiday-thinned markets. However, two reports may have greater than usual significance. First, weekly jobless claims unexpectedly jumped last week by 49k to 252k, This is a two-year high. For at least the past two years, there have been spikes, and they were quickly unwound. The December 19 report will also cover the week that the monthly nonfarm payroll survey is conducted. Second is the Leading Economic Indicator. It fell three consecutive months through October, which was a recessionary warning in the past (~80% accuracy). It may have increased in November for the first time since July. |

Economic Events: United States, Week December 16 - Click to enlarge |

Last week, Brazil, Turkey, and Russia cut interest rates. The moves were as expected, with the exception of Turkey, where the central bank delivered a larger than expected 200 bp cut. Among emerging market central banks that meet next week, Mexico’s Banxico is the only one expected to move. The recent strength of the Mexican peso, reaching five-month highs against the dollar ahead of the weekend, can only bolster conviction that the central bank will respond to the soft growth and the first year-over-year CPI print below 3% in three years. It will be the fourth 25 bp rate cut this year and brings the target rate to 7.25%, completely unwinding last year’s hikes.

Tags: Bank of England,Bank of Japan,Boris Johnson,Featured,federal-reserve,newsletter,PRC,Riksbank