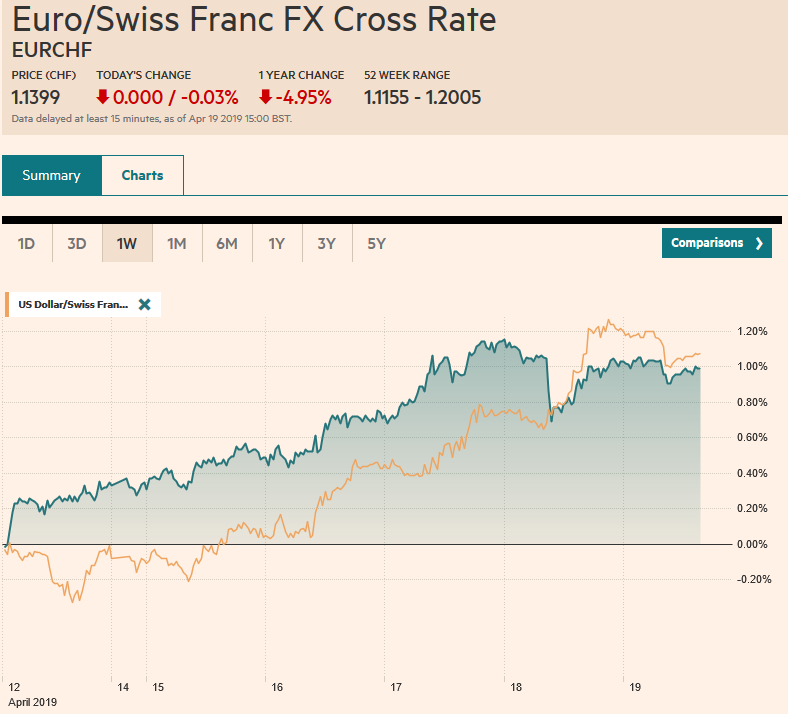

Swiss Franc The Euro has fallen by 0.03% at 1.1399 EUR/CHF and USD/CHF, April 19(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Many financial centers are closed today. These include Australia, India, most European markets, and the US. In Asia, equity markets that were open moved higher. The Nikkei, which gapped higher on Monday, rose 0.5% today for a 1.5% gain on the week. China’s Shanghai Composite rose 0.6%, lifting the weekly increase to 2.6%. The US dollar is confined to narrow ranges but has drifted lower against all the majors after yesterday’s gain on the back of strong retail sales, a new cyclical low in weekly jobless claims. Among emerging

Topics:

Marc Chandler considers the following as important: 4) FX Trends, EUR/CHF and USD/CHF, Featured, Japan, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.03% at 1.1399 |

EUR/CHF and USD/CHF, April 19(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Many financial centers are closed today. These include Australia, India, most European markets, and the US. In Asia, equity markets that were open moved higher. The Nikkei, which gapped higher on Monday, rose 0.5% today for a 1.5% gain on the week. China’s Shanghai Composite rose 0.6%, lifting the weekly increase to 2.6%. The US dollar is confined to narrow ranges but has drifted lower against all the majors after yesterday’s gain on the back of strong retail sales, a new cyclical low in weekly jobless claims. Among emerging market currencies, the Turkish lira and South African rand are a bit soggy, while several Asian currencies, including the Chinese yuan, have edged higher. |

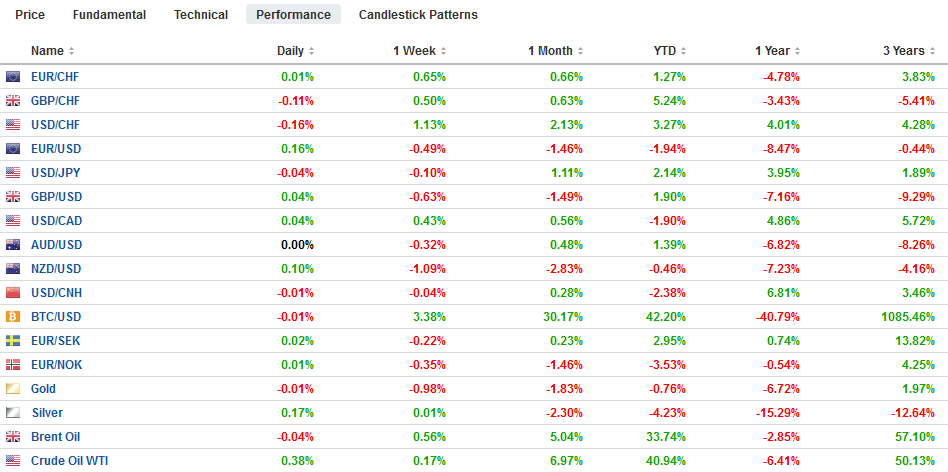

FX Performance, April 19 - Click to enlarge |

Japan

Three developments are noteworthy. First, Japan’s core measure of inflation, which excludes fresh food prices, and is the measure that the BOJ formally targets (at 2%) rose to 0.8% from 0.7%, where it had been expected to remain. Last October and November, core inflation peaked at 1% and fell back to 0.7%. Non-fresh food prices rose 0.8% from 0.6%, and energy prices accelerated to 5.1% from 4.5%. The headline CPI rose 0.5% after a 0.2% year-over-year increase in February. Excluding fresh food and energy, Japan’s consumer inflation was unchanged at 0.4%. Deflation in fresh food prices eased from -11% in February to -6% in March. The outlook is not particularly inspiring. Downward pressure on core inflation is expected for two sources in the coming months: free schooling for young children and cuts in mobile phone service. The former is a new government initiative. The largest mobile service provider is expected to cut prices by as much as 40%. These two developments could shave 0.2-0.3 percentage points off core CPI.

The second development was surprising. The Bank of Japan reduced the purchases of its long-dated bonds (both the 10-25 year and the 25-year-plus segments). It is the first tapering in two months. The timing was unexpected. It is days ahead of next week’s BOJ meeting, and more importantly, it is ahead of the unusually long 10-day holiday (April 27-May 6). Some observers see the tapering as a protest to the recent curve flattening. If this is the case, it is very subtle. Japan’s 10-year yield is virtually unchanged over the past two weeks at minus three basis points. The two-year yield is flat at minus 15 bp. The 30-year JGB yield had risen one basis point over the past two weeks coming into today and with the BOJ’s help, rose 3.5 bp to almost 60 bp, matching a high since early March.

The third development was not so much the suggestion by the Deputy Cabinet Secretary that the sales tax increase slated for October could be delayed for the third time, but how quickly senior officials came out to deny it. The bar to delaying it a third time is high. The government has already approved of measures aimed at offsetting the impact on consumption. Officials have suggested that only a major crisis would derail the process. Ahead of the tax increase, Japan holds upper house elections in July. Since Abe campaigned for his third term defending the tax, there is a thought that a delay would require new elections (for the lower house) too and, even if Abe was sympathetic, with responsibilities associated with being the G20 host, the bar is even higher.

United States

The divergence revealed yesterday, where the eurozone flash PMI disappointed, and the US retail sales surged, could hardly have been starker. The composite PMI slipped to 51.3 from 51.6. Both the German and French manufacturing PMI readings remained below the 50 boom/bust level. The US retail sales were better than we feared (due to the decline in tax refunds and the decline in household auto purchases) and better than the market expected. The 1.6% increase was the strongest in 18 months. The gains were widespread–12 of the 13 retail categories increased. The lone exception was sporting good and hobby stores. Excluding autos and gasoline, retail sales rose 0.9%, which recoups the 0.7% drop in February and a little more. The strength of the report prompted many economists to revise up their forecasts for Q1 GDP that will be released at the end of next week. We are not as optimistic as the Atlanta Fed, whose GDP tracker estimates a 2.8% annualized expansion. Nor are we as pessimistic as those economists forecasting around a 1.5% print. Our own back-of-the-envelope calculation puts it around 2%.

The response to the publication of a redacted Mueller report is the lead news in the US today. In trying to understand the drivers of the capital markets and exchange rates, in particular, it seems irrelevant. It does not impact the larger divergence theme that underpins our constructive dollar outlook. It has no bearing on our assessment of the trajectory of Fed policy. We would still not want to bet the monetary cycle is complete, no matter how pregnant of a pause is taken. It may distract on the domestic political scene, but the international agenda continues. The US trade representative returns to Beijing before China’s Vice Premier comes to Washington in early May. The last attempt to manage expectations suggest a meeting between the two presidents could come as early as the end of next month. After stopping in Europe and call on Tusk and Juncker (Japan and the EU free-trade agreement went into effect February 1), Abe will come to the US at the end of next week. Although trade talks are the ostensible reason, and Finance Minister Aso will join to talk about the currency component in the trade talks, some suspect this is Abe’s effort to also ingratiate himself with the Trump: It is the First Lady’s birthday on April 26.

Exchange Rates

The dollar’s losses today pare with week’s advance. It has risen against all the major currencies but the Japanese yen, which is virtually flat. The euro, unable to take out the previous week’s high near $1.1325 fell a cent on yesterday’s diverging news. Monday’s (April 15) close above $1.13 was the first close above the old floor this month. It looks as if in the options market, the dollar longs have been selling calls for protection. This has seen the put-call skew (risk-reversal) shrink while volatility continues to trend lower. Sterling closed below $1.30 yesterday for the first time since February 18. We suspect it is a false break. UK recent employment and retail sales data have been stronger than expected, but Brexit continues to suck up the oxygen. Parliament returns next week. The dollar continues to hover around JPY112.00. The closes for the last five sessions have been within a few ticks of it. A convincing break could spur a move toward JPY114.00. That said, the JPY112.00 area stemmed the March rally too and then the dollar was set back and briefly traded below JPY110 before finding bids again. The US dollar remains range bound between CAD1.33 and CAD1.34. Those playing for a breakout have had their fingers burned again. The problem is that making money in the range leaves one vulnerable to losing money when the real break comes. The Bank of Canada meets next week. The neutral stance is likely to be reinforced. The Australian dollar briefly poked above $0.7200 for the first time in two months. This saw fresh sales, despite the stronger Chinese data and many embrace the Aussie as a proxy. A soft Q1 CPI report next week may reinforce the cap.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,EUR/CHF and USD/CHF,Featured,Japan,newsletter