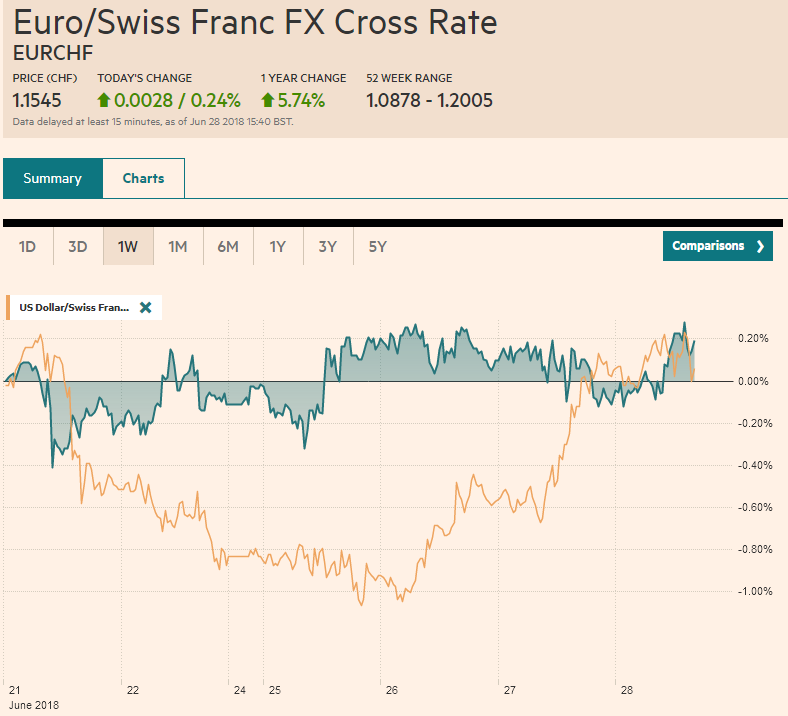

Swiss Franc The Euro has risen by 0.24% to 1.1545 CHF. EUR/CHF and USD/CHF, June 28(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates The US dollar is consolidating its gains against most of the major currencies, but the underlying strength remains evident. Several major and emerging market currencies are at new lows for the year, including sterling and the New Zealand dollar, but also the yuan, rupee, and the rupiah. Indonesia’s central bank meets later this week, and a 25 bp rate hike that had been expected may not be enough to deter additional losses. The Chinese yuan extended its losing streak. The offshore yuan (CNH) has fallen for 11 consecutive sessions. The

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, CAD, EUR, Featured, GBP, JPY, newslettersent, Oil, SPY, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Swiss FrancThe Euro has risen by 0.24% to 1.1545 CHF. |

EUR/CHF and USD/CHF, June 28(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is consolidating its gains against most of the major currencies, but the underlying strength remains evident. Several major and emerging market currencies are at new lows for the year, including sterling and the New Zealand dollar, but also the yuan, rupee, and the rupiah. Indonesia’s central bank meets later this week, and a 25 bp rate hike that had been expected may not be enough to deter additional losses. The Chinese yuan extended its losing streak. The offshore yuan (CNH) has fallen for 11 consecutive sessions. The slide is on roughly the same pace as seen in the 2015 devaluation. Just as the US equity market saw initial gains reversed by the close yesterday, the Shanghai Composite, and Chinese shares more generally, failed to hold on to initial gains and finished lower (~1%) for the fourth consecutive session. Chinese officials do appear increasingly concerned about the risk of a vicious cycle. One step being considered is to ban the issuance of short-term dollar bonds, which previously did not need pre-approval by regulators. This has been one of the favorite tools in the property developments space. Foreign selling pressure continues in Asia shares. The MSCI Asia Pacific Index fell for a fourth straight session and is off around 2.8% this week. Foreign investors. Since June 6, foreign investors have been net sellers of Korean shares in all but two sessions, and have only bought Taiwanese shares once. |

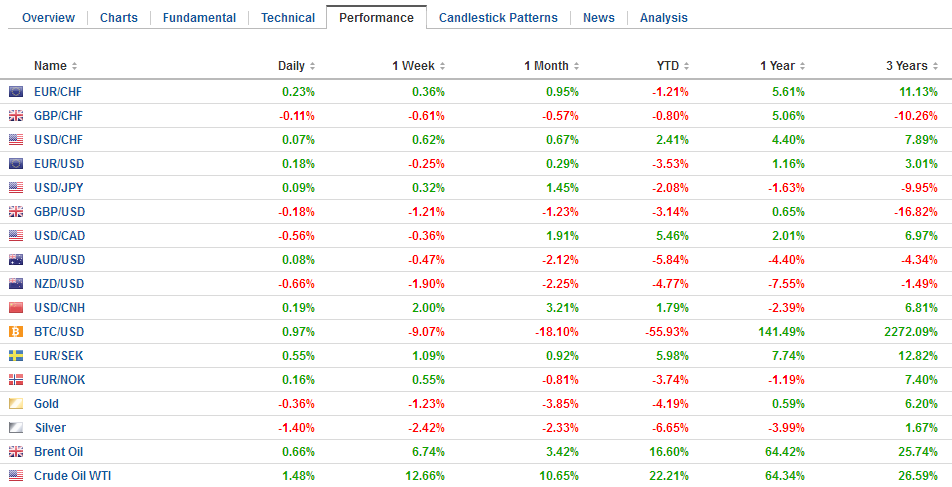

FX Performance, June 28 - Click to enlarge |

Among the major currencies, the New Zealand dollar is the weakest. It is off roughly 0.5% (~$0.6760). It has only advanced in two sessions since June 6 and over the three weeks has depreciated by about 4%. Today’s driver was the dovish hold by the central bank. Governor Orr warned that rates would remain low for some time and that the next move could be a cut or a hike.

Selling pressure on the euro eased as it approached the lower end of its recent range just above $1.1500. Today’s low was a little below $1.1530. A nearly billion euro option struck at $1.15 expires today. There is a 645 mln euro option at $1.1585 that will also be cut today. The dollar is steady against the yen and spent most of the Asian session and European morning above JPY110. A trend line drawn off the recent highs intersects today near JPY110.70. Only a break above it lifts the technical tone.

Sterling traded heavily, having fallen to $1.3065 and was not helped by BOE’s Cunliffe’s concern about how highly indebted households will cope with an economic downturn. He did not sound as if he was prepared to hike rates as early as August. Sterling is likely to find support ahead of the $1.30 psychologically important level.

The Canadian dollar is consolidating yesterday’s losses. Many investors heard a dovish Poloz yesterday. He did reiterate the uncertainty over trade and the impact of new mortgage lending rules, but at the same time, he noted that the market understood its May statement in which it seemed to signal the likelihood of a rate hike. US dollar support is seen in the CAD1.3265-CAD1.3280 area.

Italy and Spain have reported preliminary June inflation figures, and German states are releasing their estimates ahead of the national figures out later today. Spanish and Italian consumer pressures rose. In Spain, CPI rose 0.2% on the month for a 2.3% year-over-year pace. This is up from 2.1% in May. Italy reported a 0.3% increase for a 1.5% year-over-year pace, up from 1.0% in May. German states suggest the headline pace for the nation may slip to 2.1% from 2.2%. While most states do not break out the core rate, Saxony does, and it slipped to 1.4% from 1.6%, which could blunt the impact of the headline staying above 2.0%.

However, with the ECB rates on hold for another year, the high-frequency economic data in the near-term may not have much impact beyond the headline reaction. The focus shifts to the EU Summit that begins today. Immigration and EU economic reforms are high on the agenda, but the UK’s May is expected to be chastised by the EU for the slow progress on Brexit. The Irish border, as we have suggested, remains an intractable situation. The next window of opportunity may be the July 6 UK cabinet meeting.

Oil prices are consolidating yesterday’s surge. The US reported a much larger drawdown of crude inventories, which came as the US pressures others to stop buying any oil from Iran starting in November. Also, the largest tar sands field in Canada had some outages and supply from Libya is weaker than expected. The EIA reported a 9.9 mln barrel draw of US inventories. US crude stocks were expected to have fallen by six mln barrel decline. In the past three weeks, US inventories have fallen by nearly 20 mln barrels, which appears to be the largest in years. Meanwhile, US oil exports spiked to 3 mln barrels a day.

Trade tensions have not gone away, but they have eased slightly. Chinese officials seem to be playing down the “Made in China 2025” rhetoric as it antagonizes the US. At the same time, Trump rejected the war-camp’s advocacy of a new procedure to scrutinize Chinese purchases of US companies. Trump has agreed to strengthen the existing Committee on Foreign Investment in the US (CFIUS). However, reports indicate that that Chinese direct investment in the US has fallen sharply in H1 18 to less than $2 bln from around $46 bln in H1 17.

The US session features weekly initial jobless claims, the KC Fed survey (June) and another look at Q1 GDP. These are not market movers. Investors will be interested in the second part of the Fed’s stress tests and today’s announcement involves how much the banks can pay out to investors in the form of dividend and stock buybacks. Some banks want to return more than they made. Tomorrow the US reports May personal income and consumption figures, which will inform Q2 GDP forecasts. The core PCE deflator, for which the Fed aims for 2%, is expected to tick up to 1.9% from 1.8%.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$CAD,$CNY,$EUR,$JPY,Featured,newslettersent,OIL,SPY