UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold – Value of Sterling and increased risks place pressure on pensioners both in UK and abroad – 500,000 British expats face ‘frozen’ pensions – 61% of UK Direct Benefit pension schemes have more money going out than coming in – OECD report finds ‘UK workers face the biggest retirement cliff edge in developed world’ – Combined pension deficit of FTSE 350 companies is at 70% of their profits – One in three wealth managers are holding cash for clients in anticipation of a market crash Source: Professionalpensions.com - Click to enlarge The UK’s future pensioners should not rely on their state pension or they may face a huge fall in earnings, says a new

Topics:

Jan Skoyles considers the following as important: Daily Market Update, Featured, GoldCore, newslettersent

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

| UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold

– Value of Sterling and increased risks place pressure on pensioners both in UK and abroad |

Source: Professionalpensions.com - Click to enlarge |

| The UK’s future pensioners should not rely on their state pension or they may face a huge fall in earnings, says a new report by the OECD.

Should Brits rely solely on their UK state pension then they will face the largest income drop of any OECD country. UK pensions represent on average 29% of in-work earnings, the OECD average is 63%. The OECD explains: ‘Retirees without such additional sources of revenue [i.e. private pensions] are left with few resources; this is reflected in the poverty rate and high income inequality in the United Kingdom for the over 65s. ‘Following the sharp rise of income disparities during the 1980s in the United Kingdom, inequalities in later life will rise further as generation X approaches retirement.’ Once private pensions are factored in then the UK does not fair so badly; ahead of Germany but behind France, Italy and Spain. But this is not something that should relax future retirees. There is a major pensions crisis in the UK, for both state and private funds. The OECD even refers to the UK’s defined benefit workplace pension plans (final salary schemes) as ‘persistently underfunded’. This, combined with a low contribution rate by individuals, is down to a number of factors. The conclusion of the OECD report reminds readers of the importance of saving and politicians of the need for long-term planning over short-term policy gains. There is little hope of politicians taking their attentions away from either Brexit or short-term economic results. We suggest the UK’s future pensioners, both at home and abroad, look to diversify their portfolios away from the risks currently facing the country. Discrimination of expat pensioners Expats living in the EU breathed a sigh of relief in September when a deal was confirmed regarding the ‘triple lock’ of their UK state pensions. The ‘triple lock’ means pensions increase by the highest of earnings, inflation or 2.5%. This means pensioners’ income keeps pace with the rising cost of living. The September deal confirmed that this would continue to happen for those British nationals living in both the EU and EEA, following Brexit. Sadly this is not the case for expats who have chosen to live abroad and outside of these economic zones. Of whom, there are more of than those living in either the EU or EEA. There is estimated to be over half a million Brits now highly exposed to weaknesses in the British pound and UK economy. These individuals will not see an increase in their pensions each year. Not only have these expats been suffering as a result of the falling value of the pound thanks to inflation, but their plight has been made worse since Brexit. Of the top ten most populated countries by ‘frozen’ pensioners, Nigeria is the only country where sterling has gained strength. |

Source: The Telegraph - Click to enlarge |

| There are arguments that the government’s approach to frozen pensions discriminates randomly between countries. Nigel Nelson, former president of the International Consortium of British Pensioners, explains:

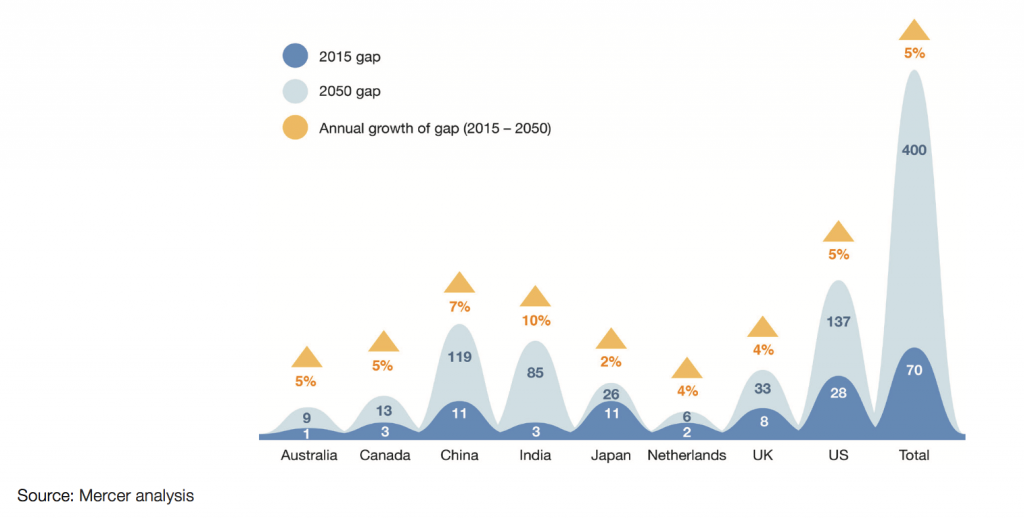

“One colleague of mine retired to Canada in 1998 and received a state pension of £64.70 a week and nearly 20 years later he is still getting £64.70. “As a result he’s received £27,945 less than his peers in Britain even though he has made the same level of National Insurance Contributions. This is just not right, it is immoral and discriminatory.” Sadly, even those who live within the EU and EEA cannot count their chickens too soon. By 2020 the Conservatives intend to remove the 2.5% underpin which currently forms part of the ‘triple-lock’. This means pensioners will no longer be protected from the onslaught of inflation. Responsible savers punished by irresponsible governments It is not just the onslaught of inflation that is going to prove to be a pensioner’s biggest nemesis. Whether relying on state or private pensions, retirees are facing huge risks in coming years. In May the OECD announced that it expected the UK’s pension deficit to increase by around 4 per cent per year, reaching more than £25 trillion by 2050. It seems that the black hole of retirement funds is much deeper and darker than any authority in the UK was prepared to admit. |

UK Pension Deficit, 2015 - 2050 - Click to enlarge |

| This black hole is something we have in common with many countries, for two reasons.

Firstly, record low interest rates and quantitative easing have inflated the present value of future liabilities. Nothing has been able to offset these. We now live in an era of low prospective returns, with little sign of let-up. One might have hoped that the surges in share prices around the world might have helped manage the above issue. It hasn’t and the record valuation levels have begun to make fund managers nervous. One in three are now building cash positions in their clients’ portfolios as they protect themselves against a sudden market crash. Secondly, the retirement of baby boomers has sent more schemes offering direct benefit pensions in to the red. This is happening on average to 35% of direct pension schemes in Europe, but to 61% in the UK. Unsurprisingly schemes are forced to raid their capital base. This places final salary pension schemes at risk as more companies look at pensions as a liability. In the UK the Pension Protection Fund works to support pensioners whose companies’ pension schemes need to be bailed out. In the year to March 2017 it paid out £661.3million to 129,661 pensioners. When the PPF launched in 2007 it paid out just up from £1.4million. The fund is sustained by charging a levy on those companies who have final pension salary schemes. Costs are expected to climb as the PPF faces bailing out the likes of BHS and Monarch. How will small firms cope with the pressures of covering this levy as well as their own employees’ schemes? |

- Click to enlarge |

| The chances are this rescue fund is not sustainable. Especially when one considers the increased costs to companies through employees taking early retirement for medical reasons (obesity related, very often). This is sad news given more people are set to rely on these pension schemes as others backfire on them, namely state pension and any opportunity they took by raiding their pension pots by the UK government’s ‘freedom and choice scheme’.

What are we left with? A broken pension system thanks to a series of bad policy decisions by governments looking for quick wins and approaching the economy like an ostrich. Do not rely on others for your pension: rebalance to cash and gold Sadly there is little to be done to save the pension schemes. It would take nothing short of a miracle to stave off the numerous risks facing them. The likes of inflation and market shocks are inevitable given the last decade of QE. In addition the UK has not helped itself with its irresponsible policies that encourage us to spend more, save less and raid whatever savings we still have. In short, ignore government advice. As we are now seeing, it comes too little too late and always with an agenda. Instead, look to diversify your assets with cash and gold. Dr. Constantin Gurdgiev, formerly an adviser to GoldCore, says the following about the importance of having gold in your pension:

Investors in the UK and Ireland, the US, the EU can invest in gold bullion in their pension, through self-administered pension funds. UK investors can invest in gold bullion through their Self-Invested Personal Pensions (SIPPs), Irish investors can invest in gold in Small Self Administered Schemes (SSAS) and US investors can invest in gold in their Individual Retirement Accounts (IRAs). The pension crisis is a multi-trillion dollar/pound crisis. It is not going to go away. Adding gold to your pension is a key way to protect your retirement from the pensions time bomb. Pension funds, throughout the West, have a distinct lack of diversification when it comes to assets. This has cost pension holders a huge amount of money and places their future livelihoods and risk. Gold has an important role to play over the long term in preserving and growing pension wealth. You can read our guide about how to invest in gold in a pension in the UK here. |

Source: Ctit Research - Click to enlarge |

Tags: Daily Market Update,Featured,newslettersent