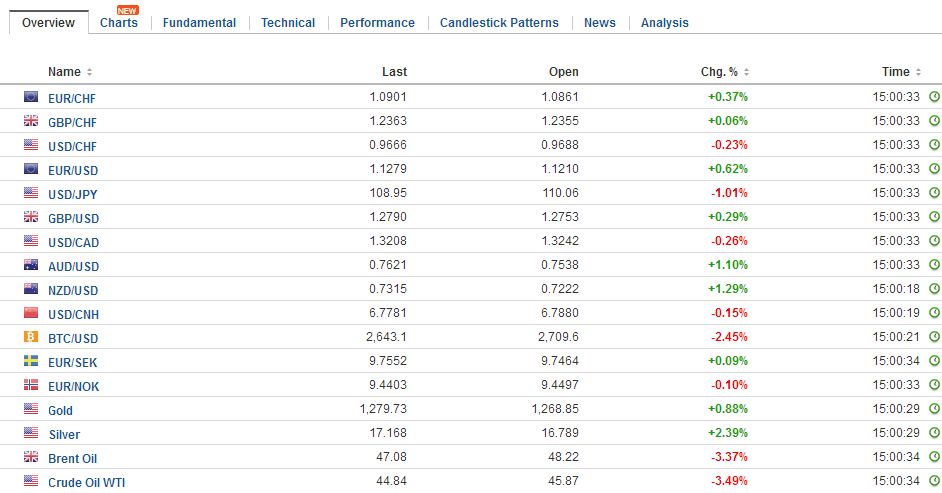

Swiss Franc The Euro has risen by 0.37% to 1.0901 CHF. This is a typical movement ahead of the SNB meeting tomorrow. This movement is probably unrelated to the Fed rate hike, given that the USD/JPY has fallen. It makes sense to go long CHF against JPY, if you bet on an inactive SNB. Inactive SNB would mean that the central bank will not speak about stronger FX Interventions or about lower rates. EUR/CHF - Euro Swiss Franc, June 14(see more posts on EUR/CHF, ) - Click to enlarge FX Rates The US dollar is narrowly mixed ahead of the FOMC meeting, where a dovish hike seems widely expected. The Australian dollar is leading the dollar bloc and Scandis higher. The Aussie had to shrug off soft consumer confidence a

Topics:

Marc Chandler considers the following as important: $CNY, China Fixed Asset Investment, China Industrial Production, China Retail Sales, EUR/CHF, Eurozone Employment Change, Eurozone Industrial Production, Featured, FX Daily, FX Trends, Germany Consumer Price Index, JPY, newslettersent, U.K. Average Earnings Index, U.K. Unemployment Rate, U.S. Consumer Price index, U.S. Core Consumer Price Index, U.S. Crude Oil Inventories, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Swiss FrancThe Euro has risen by 0.37% to 1.0901 CHF. This is a typical movement ahead of the SNB meeting tomorrow. This movement is probably unrelated to the Fed rate hike, given that the USD/JPY has fallen. It makes sense to go long CHF against JPY, if you bet on an inactive SNB. Inactive SNB would mean that the central bank will not speak about stronger FX Interventions or about lower rates. |

EUR/CHF - Euro Swiss Franc, June 14(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesThe US dollar is narrowly mixed ahead of the FOMC meeting, where a dovish hike seems widely expected. The Australian dollar is leading the dollar bloc and Scandis higher. The Aussie had to shrug off soft consumer confidence a day before the monthly employment report and perhaps was encouraged by the recovery in iron ore prices after initial weakness. For their parts, the euro and yen have barely changed. The euro has been confined to less than a quarter of a cent as it continues to consolidate. Support is seen in the $1.1165-$1.1185. The euro has not been above $1.1240 since June 8. Meanwhile, the dollar continues to straddle the JPY110 area. Today is the fifth consecutive session it has traded on both sides of JPY110. Note that the Bank of Japan (the Bank of England and the Swiss National Bank) meet tomorrow. |

FX Daily Rates, June 14 - Click to enlarge |

| It was not enough for Chinese shares. The Shanghai Composite cut this year’s gains nearly in half was a 0.75% decline, and the 1.3% loss by the CSI 300 is the largest this year. Despite these losses and a small decline in Tokyo and Taiwan, the MSCI Asia Pacific Index rose for a second session (~0.12%).

Investors are also looking for more details about the Fed’s balance sheet strategy. Such information is more likely to be found during Yellen’s press conference rather than the FOMC statement. The general thrust of the Fed’s strategy is beginning slowly to cap the reinvestment of maturing funds and gradually ratchet it up. The Fed funds rate will remain the primary tool of monetary policy. The inclination is to include both Treasuries and MBS in the program. The program may begin before the Fed decides the terminal size of the balance sheet. Separately, China’s lending increased, but the deleveraging, which officials saw is behind the slowing of M2 (to 9.6% from 10.5%), is seen in the shadow banking. New yuan loans increased by CNY1.11 trillion, a little more than April and an 11% more than expected. However, aggregate financing rose a little less (CNY1.06 trillion); the difference being a small contraction in non-banking lending. |

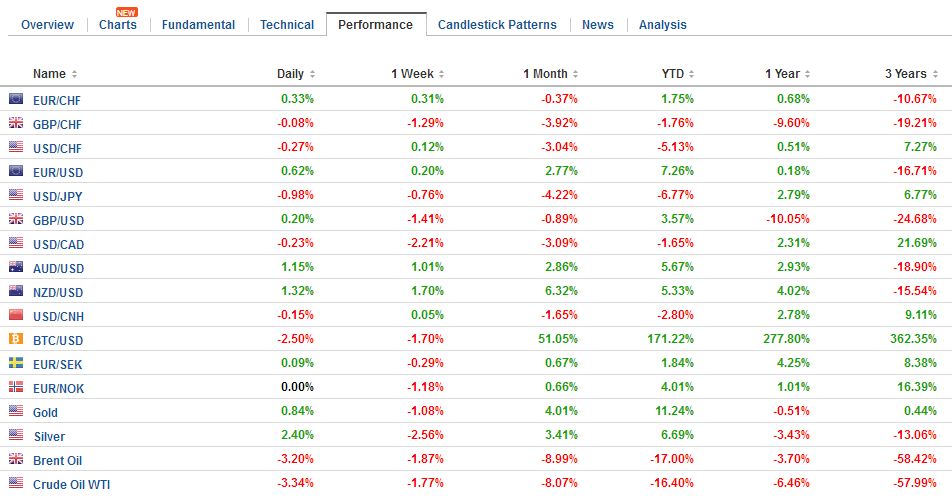

FX Performance, June 14 - Click to enlarge |

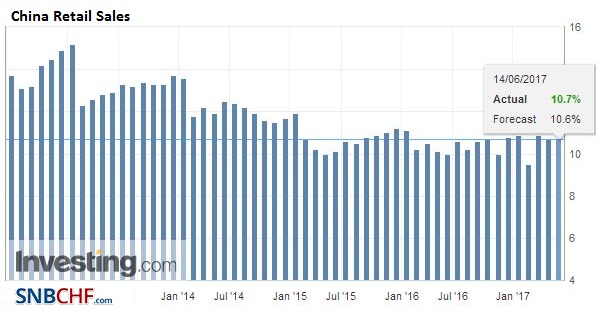

ChinaChina’s data may have also been supportive. Chinese consumers continue to shop. Retail sales rose 10.7% year-over-year in May, and the year-to-date pace of 10.3% is the highest this year. |

China Retail Sales YoY, May 2017(see more posts on China Retail Sales, ) Source: Investing.com - Click to enlarge |

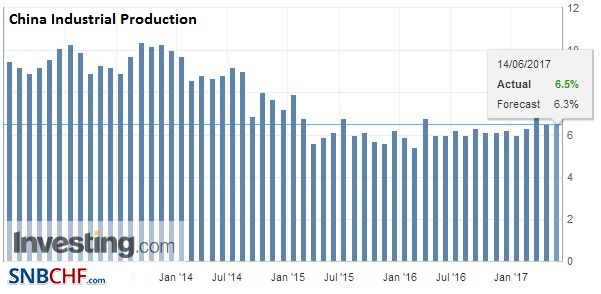

| Industrial output rose 6.5%, the same as in April, and a little more than expected. |

China Industrial Production, May 2017(see more posts on China Industrial Production, ) Source: Investing.com - Click to enlarge |

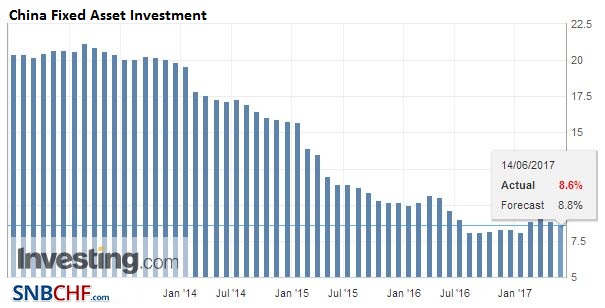

| Fixed asset investment slowed to 8.6% from 8.9%. While a slowing in investment in China is seen a healthy development, reducing a significant imbalance, the details are a bit worrisome. Investment growth in the primary sector increased more than investment in manufacturing and services. |

China Fixed Asset Investment, May 2017(see more posts on China Fixed Asset Investment, ) Source: Investing.com - Click to enlarge |

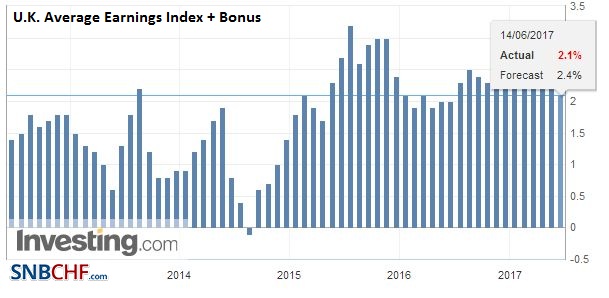

United KingdomSterling had extended yesterday’s recovery and traded to almost $1.28 before poor weekly earnings data stopped it in its tracks. Average weekly earnings, excluding bonus payment, rose 1.7% in the three months through April from a year ago. The slowing actually took place in March, which was revised from 2.1% to 1.8%. The fifth consecutive slowing brings the pace to its lowest level in more than two years. Whatever difficulty one may have thought the slightly firmer than expected CPI would have on the BOE deliberations, the weakness in the earnings data offsets it, and more. The higher inflation coupled with weaker nominal earnings suggest a squeeze on real income, which in turn may weigh on consumption. A break of $1.27 warns of a retest of sterling’s recent lows. |

U.K. Average Earnings Index +Bonus, April 2017(see more posts on U.K. Average Earnings Index, ) Source: Investing.com - Click to enlarge |

U.K. Unemployment Rate, April 2017(see more posts on U.K. Unemployment Rate, ) Source: Investing.com - Click to enlarge |

|

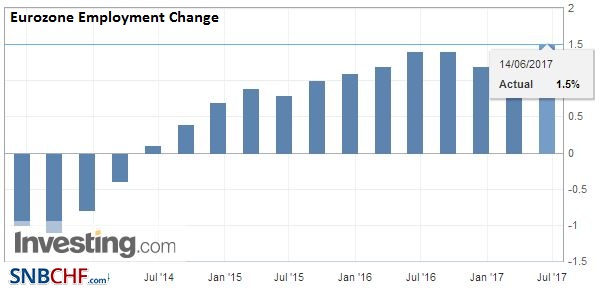

EurozoneEuropean shares are also higher; led by a recovery in the information technology space. Perhaps aided by the 0.5% rise in the eurozone’s April industrial output, and an upward revision to the March series (0.2% rather than -0.1%), is helping the industrial equities. |

Eurozone Industrial Production YoY, April 2017(see more posts on Eurozone Industrial Production, ) Source: Investing.com - Click to enlarge |

Eurozone Employment Change YoY, Q1 2017(see more posts on Eurozone Employment Change, ) Source: Investing.com - Click to enlarge |

|

Germany |

Germany Consumer Price Index (CPI) YoY, May 2017(see more posts on Germany Consumer Price Index, ) Source: Investing.com - Click to enlarge |

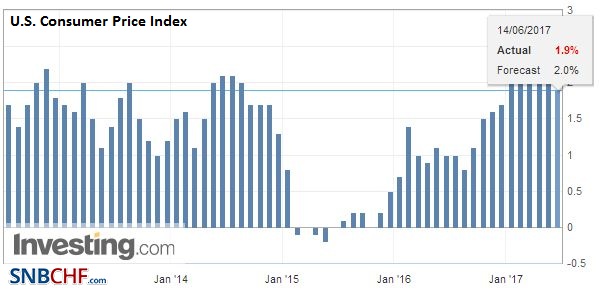

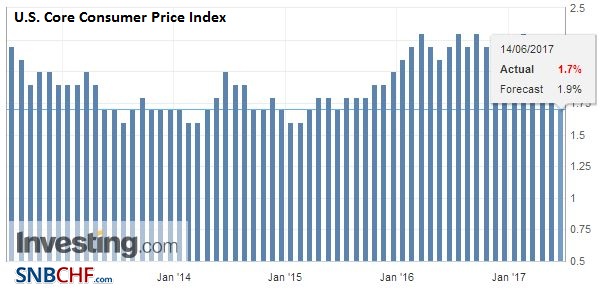

United StatesAhead of the FOMC meeting, the US reports May CPI and retail sales. The year-over-year headline pace of CPI may slow, however, the core rate is expected to be steady at 1.9%. It has declined for three consecutive months, like the core PCE deflator, and this has begun being concerning to investors and policymakers. The market may be particularly sensitive to downside surprises, and will also focus on the Fed’s comments and inflation forecasts. |

U.S. Consumer Price Index (CPI) YoY, May 2017(see more posts on U.S. Consumer Price Index, ) Source: Investing.com - Click to enlarge |

U.S. Core Consumer Price Index (CPI) YoY, May 2017(see more posts on U.S. Core Consumer Price Index, ) Source: Investing.com - Click to enlarge |

|

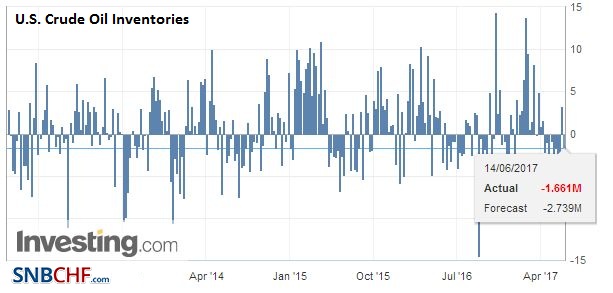

| Some of the factors that may slow headline CPI may also act as a drag on retail sales, as the drop in gasoline prices. We already know that auto sales disappointed. Headline retail sales are expected to be flat, but the components used for GDP may rise 0.3% after a 0.2% rise in April. |

U.S. Crude Oil Inventories, May 2017(see more posts on U.S. Crude Oil Inventories, ) Source: Investing.com - Click to enlarge |

The market has practically fully discounted a 25 bp hike in the Fed funds target range today. Investors are more interested in the forward guidance rather the rate move itself. In some ways, Governor Brainard framed the issue recently. Economic growth and prices may be disappointing, and this may make officials cautious about continuing to normalize policy. On the other hand, financial conditions are looser than the Fed deems appropriate. They have wanted to remove accommodation, but a wide range of rates are lower, the stock market is higher, and the dollar is weaker.

However, before reaching the conclusion that monetary policy is not effective, investors and policymakers will likely keep in mind that such policy acts with unpredictable and variable lags. It was slow to take effect in the depths of the crisis, and it is slow to take effect on the other side. Yellen will likely stress the data dependency of the FOMC. It seems that the potential need for a tactical adjustment is possible precisely because Fed policy is not dictated by some rule-based system. Bloomberg and the CME calculations show a little less than a 40% chance of another hike this year.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$CNY,$JPY,China Fixed Asset Investment,China Industrial Production,China Retail Sales,EUR/CHF,Eurozone Employment Change,Eurozone Industrial Production,Featured,FX Daily,Germany Consumer Price Index,newslettersent,U.K. Average Earnings Index,U.K. Unemployment Rate,U.S. Consumer Price Index,U.S. Core Consumer Price Index,U.S. Crude Oil Inventories