FX Rates The US dollar is higher against the major currencies but the Japanese yen and the New Zealand dollar. The dollar fell to new two-year lows against the yen to JPY103.55 before bouncing in the European morning back to JPY104.40. The Kiwi was helped by better than expected Q1 GDP. The euro and sterling are within yesterday’s ranges. The euro has been able to resurface above .13 since Monday. Bids have been found a little below .12. UK reported better than expected retail sales, but the referendum keeps a lid on the pound. Soft employment data weighs on the Aussie. click to enlarge Global equities are lower. MSCI’s Asia-Pacific Index is off 1.1%, its third loss this week. European markets are lower as well, nursing a 0.8% loss near midday in London. Financials are the weakest sector, with a 1.7% drag. Core bond yields are little changed, while peripheral European benchmark 10-year rates are higher (2-3 bp in Spain and Italy, 8 in Portugal). A hawkish Fed was to be negative for emerging markets, but dovish dot plot has not helped. The MSCI Emerging Market equities are off 1%. The dollar is firmer against most of the emerging market currencies. The South Korean won and Taiwanese dollar edged slightly higher. East and Central European currencies have done the poorest.

Topics:

Marc Chandler considers the following as important: AUD, Featured, FX Trends, GBP, JPY, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

FX RatesThe US dollar is higher against the major currencies but the Japanese yen and the New Zealand dollar. The dollar fell to new two-year lows against the yen to JPY103.55 before bouncing in the European morning back to JPY104.40. The Kiwi was helped by better than expected Q1 GDP. The euro and sterling are within yesterday’s ranges. The euro has been able to resurface above $1.13 since Monday. Bids have been found a little below $1.12. UK reported better than expected retail sales, but the referendum keeps a lid on the pound. Soft employment data weighs on the Aussie. |

click to enlarge |

| Global equities are lower. MSCI’s Asia-Pacific Index is off 1.1%, its third loss this week. European markets are lower as well, nursing a 0.8% loss near midday in London. Financials are the weakest sector, with a 1.7% drag. Core bond yields are little changed, while peripheral European benchmark 10-year rates are higher (2-3 bp in Spain and Italy, 8 in Portugal). A hawkish Fed was to be negative for emerging markets, but dovish dot plot has not helped. The MSCI Emerging Market equities are off 1%. The dollar is firmer against most of the emerging market currencies. The South Korean won and Taiwanese dollar edged slightly higher. East and Central European currencies have done the poorest. The continued slide in oil prices and industrial metal prices weighs on Russia and South Africa. |

click to enlarge |

Officials and events have conspired to shake the already fragile market confidence. The Federal Reserve noted yesterday, its widely anticipated decision not to lift its rate target, which the long-term equilibrium target rate is likely lower than previously thought. In her press conference, Yellen recognized that some of the headwinds the economy faces, like demographics, may last a long time.

The Bank of Japan also stood pat, but despite acknowledging the deterioration of inflation and inflation expectations, it retained its forecast that inflation will hit its target in the fiscal year that begins next April. The markets’ response was similar to its reaction to the BOJ’s late-April decision to stand pat as well. The yen strengthened from already elevated levels, and Japanese shares sold off hard. The 3% loss today in the Nikkei brings its losses this week to a little more than 7%.

Despite the softening of the Fed’s outlook, the dollar finished little changed against the yen yesterday. On Tuesday, Bloomberg has the greenback closing the North American session at JPY106.11 and on Wednesday at JPY106.01. The dollar was sold to JPY103.55 in Asia before stabilizing in the European morning. Although Japanese officials, including Kuroda and Cabinet Secretary Suga, indicated they were watching the currency, there was no intervention.

The break of JPY105 without intervention strengthens our understanding that intervention will not be aimed at defending a certain level as if a line has been drawn…in sand. The intervention needs to be in a specific context of disorderliness. Given the FOMC’s decision and guidance, the BOJ’s decision, the looming UK referendum, the slump in equities, are the fundamental drivers of the yen’s strength.

That said, this is the fifth consecutive session the dollar has fallen against the yen. The dollar has fallen every session this month but two. In this period, the yen has gained 6.2% against the dollar (6% against the Chinese yuan), 5.1% against the euro and 8.3% against sterling.

Australia contributed to the downbeat economic news with a disappointing May jobs report. The headline job growth of 17.9k (expectations for ~15k) masked that these were all part-time jobs, and that last month’s 9.3k loss of full-time jobs was really twice as large (18.2k). Separately, Australia reported the second consecutive month of falling vehicle sales. The 1.1% fall in May follows a 2.8% fall in April. Sales in Q1 were up about 2.3%.

The disappointing data and weaker commodity prices saw the Australian dollar move back from yesterday’s highs near $0.7440 toward the lows. Today’s low of $0.7345 is just ahead of the low from the previous two sessions around $0.7335. New Zealand, on the other hand, reported better Q1 GDP of 0.7% (rather than 0.5%), lifting the year-over-year pace to 2.8% from 2.3%. The Australian dollar was also sold against its Tasmanian cousin.

United KingdomSterling is also trading within yesterday’s range, though is about a third of a cent lower on the day as North American markets prepare to open. News that May retail sales jumped 0.9%, well more than the market expected failed to offset the anxiety over next week’s referendum. The Evening Standard poll captured the spirit of what many sense. Excluding the “don’t know”, the survey found 53% favor leaving and 47% favor remaining in the EU. This is nearly a complete reversal of the results of the survey conducted in April. |

click to enlarge |

SwitzerlandThe Bank of England meets, but like the Swiss National Bank meeting earlier, is unlikely to be much of a market factor. There is no doubt that it is on hold. Carney may say something about contingency planning. However, his Mansion House speech is tipped to be on crypto-currencies. Osborne is expected to take up the referendum in his talk. |

click to enlarge |

United StatesThe US data are unlikely to spur a strong market response as investors continue to digest the FOMC meeting and keep on eye on the latest polls and odds of the UK referendum. The data, for the most part, is not the stuff the will sway Fed officials one way or the other. |

click to enlarge |

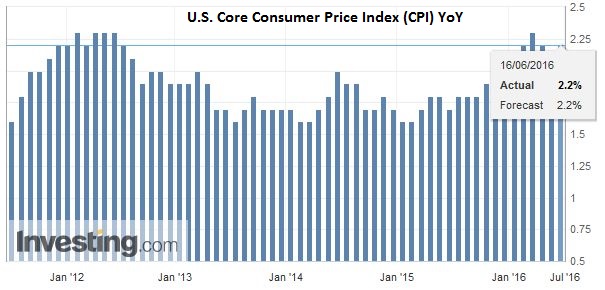

| Then there is CPI. The core rate may tick up to 2.2% year-over-year from 2.1%. There has been a gradual increase in core CPI. The 24-month average is 1.9%. The 12-month average is 2.0%. The 6-month average is 2.2% (as is the three-month average). |

click to enlarge |

|

Weekly jobless claims are expected to be near their four week average (269k) during the week that the national survey was conducted. The June Philadelphia Fed Business Outlook survey is expected to improve from a depress May level. |

click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.