Swiss Franc The Euro has risen by 0.08% to 1.0828 EUR/CHF and USD/CHF, July 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The rally in US shares yesterday, ostensibly fueled by strong earnings reports, is helping to encourage risk appetites today. The MSCI Asia Pacific Index is posting its biggest gain in around two weeks, though Japan’s markets are closed today and tomorrow. The Dow Jones Stoxx 600 is building on yesterday’s rally, and with today’s ~0.8% gain, it is up on the week. US equities are also trading with a firmer bias. The 10-year US yield that spiked to nearly 1.125% on Tuesday is knocking on 1.30% today. European bond yields are mostly softer, and Italy’s benchmark yield has slipped to a

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, China, commodities, Currency Movement, ECB, Featured, infrastructure, newsletter, U.K., USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.08% to 1.0828 |

EUR/CHF and USD/CHF, July 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The rally in US shares yesterday, ostensibly fueled by strong earnings reports, is helping to encourage risk appetites today. The MSCI Asia Pacific Index is posting its biggest gain in around two weeks, though Japan’s markets are closed today and tomorrow. The Dow Jones Stoxx 600 is building on yesterday’s rally, and with today’s ~0.8% gain, it is up on the week. US equities are also trading with a firmer bias. The 10-year US yield that spiked to nearly 1.125% on Tuesday is knocking on 1.30% today. European bond yields are mostly softer, and Italy’s benchmark yield has slipped to a new three-month low (~67 bp). The foreign exchange market is quiet. The Norwegian krone and Australian dollar lead the majors today, while the euro and Canadian dollar are little changed. The JP Morgan Emerging Market Currency Index is advancing for the third consecutive session, though it is still about 0.3% lower for the week. Gold is finding support ahead of the two-week low near $1791. Oil is firm, and the September WTI contract is building on yesterday’s 4.6% rally. Around $70.70, it is still about 1.2% lower on the week. Copper is rising for the third day. The wildfires in Canada are raising new concerns about lumber supply, and the possible impact on sawmills sent the September lumber up 7.75% yesterday, the most in a year. |

FX Performance, July 22 - Click to enlarge |

Asia Pacific

SWIFT reported that China’s yuan share rose to 2.46% in June (1.90% in May), just shy of the March high of 2.49%. It puts the yuan in fifth place overall, the same as last year. The highest share accounted for by the yuan was 2.79% in August 2015. The US dollar’s share rose to about 40.6%, the highest in a year. The euro’s share slipped to 37.9%. It is not clear that a digital yuan will bolster the use of the yuan. Separately, we note that the Institute for International Finance estimates that foreign central banks accumulated yuan reserves accounted for nearly a third of the inflows last year and as much as 60% of China’s inflows in Q1 21.

China is stepping up its efforts to ease the pressure on commodities. It is planning on increasing the sales for copper, aluminum, and zinc from its strategic reserves. In addition, Beijing has announced plans to sell a quarter of its coal reserves or around 10 mln tons. It has also announced intentions to sell 22 mln barrels of oil to its refiners. The US reported its first oil build since May as inventories rose by about two million barrels, though storage at Cushing slipped to its lowest level since January 2020. Gasoline imports are rising and stand at their highest level in a decade, with Saudi and Spanish shipments reported.

The rise in US yields is helping the greenback recovery against the yen. The dollar had traded to almost JPY109 at the start of the week and is now flirting with the JPY110.30 area. The 20-day moving average is near JPY110.40, and the US dollar has not closed above this average for two weeks. Initial support is seen around JPY110. The Australian dollar is firm and appears to be working through option-related offers. There are options for almost A$1.6 bln in the $0.7370-$0.7375 area. Support may be found in the $0.7340-$0.7360 band. The Chinese yuan has edged higher for the third consecutive session. The dollar remains in the CNY6.45-CNY6.50 range that has dominated for several weeks. The reference rate continues to be set tightly in line with expectations (CNY6.4651 vs. CNY6.4648). Its steady performance against the dollar should not obscure the fact that the yuan is trading at five-year highs against the trade-weighted basket (CEFTS).

Europe

The ECB is center stage today. The new symmetrical 2% inflation target requires an adjustment in the forward guidance in a somewhat more dovish direction. Still, this has been well-telegraphed, and the decision on the pace of bond-buying, which, as we have noted, does not seem to be the key to interest rate or exchange rate developments, will be made in September. Officials have the better part of the next six months to forge a strategy of what will follow the Pandemic Emergency Purchase Program. The ECB was buying bonds before the pandemic struck and most likely will buy them after the PEPP winds down, currently in March 2022. The change of the inflation target was said to be a unanimous decision, but the devil is in the details (of implementation), and this is likely to prove more contested terrain.

There are three areas in which the UK and EU are wrestling. First, the UK is proposing not just a change in how the Northern Ireland protocol is enforced, but even its chief negotiator Frost has acknowledged it seeks changes to the protocol itself. It now appears that Johnson’s strategy was to secure Brexit at any cost and renegotiate the agreement later. He ran a campaign that was partly predicated on the Northern Ireland configuration (remaining part of the EU common market). Second, the UK is seeking to eliminate many of the checks of goods shipped from the rest of the UK into Northern Ireland. The UK’s behavior put the EU in a poor mood for the second issue, and that is the post-Brexit relationship with Gibraltar, which it has controlled for more than two centuries. The EC is seeking a negotiating mandate to formally begin talks. Thirdly, the British are seeking more help from the French to control the migration over the Channel. It is paying France around GBP54 mln to hire more enforcement officers, but it does not appear a sufficient check.

The euro has not traded above $1.1805 since Monday. It has found support today near $1.1780 after testing the $1.1750-level yesterday and Tuesday. The market seems prepared for a dovish tone from the ECB. The week’s high was set on Monday near $1.1825. Above there, offers in the $1.1850-$1.1875 may cap it. The single currency has not traded with a $1.19-handle so far this month. Sterling snapped a four-day slide yesterday with a 0.6% gain, the most in almost two weeks. It has marginally extended those gains today and is trying to reestablish the foothold above the 200-day moving average (~$1.3710). Resistance is pegged near $1.3775.

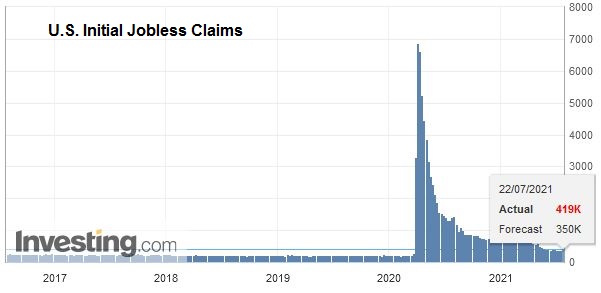

AmericaThe surge in US housing starts (6.3% vs. a median forecast for a 1.2% gain) may bode well for today’s existing-home sales report. Existing home sales have softened since January and fell for the four months through May. Still, the 5.8 mln seasonally adjusted annual pace represents an elevated pace, which is above all but the most recent pace since 2007. Weekly jobless claims are expected to have slipped to a new pandemic-era low near 350k. It would be the fourth consecutive week below 400k. Leading indicators and the KC Fed manufacturing survey tend not to attract much market attention. Meanwhile, there may be another attempt to proceed with a bipartisan infrastructure bill early next week, according to press reports. We also note that more industry reports suggest that the used car market, which has been accounting for around a third of the monthly increase in CPI, is normalizing. Previously, the wholesale market seemed to have peaked, and the most recent reports estimate that inventories have returned to pre-pandemic levels. |

U.S. Initial Jobless Claims, July 22, 2021(see more posts on U.S. Initial Jobless Claims, ) Source: investing.com - Click to enlarge |

Canada’s economic diary remains light ahead of tomorrow’s May retail sales report. A sharp decline (3% after the 5.7% decline in April) is forecast in the Bloomberg survey. Partly, this needs to be understood in the contact of more than a 10% increase in February and March. Also, the news seems somewhat dated and, outside of headline reaction, is unlikely to have policy implications. Next week, Canada reports June CPI and May GDP.

Mexico reports biweekly CPI figures today. The year-over-year increase may ease slightly from 5.74% previously. It would still leave expectations biased toward another rate hike as early as the August 12 Banxico meeting. Mexico reports May retail sales tomorrow. A 0.5% increase is expected after a 0.4% decline in April (which followed a bit more than a 6% increase in February and March). Next week’s highlights include unemployment, trade, and Q2 GDP.

The US dollar fell by nearly 1% against the Canadian dollar yesterday, the most since June 2020. There has been no follow-through selling so far today as the market appears to be waiting for the North American session. Key support is seen near CAD1.2500. A break of it will boost confidence that a top is in place and set the initial sights on CAD1.2400. Resistance may be encountered in the CAD1.2600-CAD1.2620 area. The greenback flirted with the 200-day moving average against the Mexican peso yesterday (~MXN20.21) but settled below it and is also confined to a narrow range today (~MXN20.1120-MXN20.1760). Initial support may be found near MXN20.08 and then MXN20.04. A break of MXN20.00 would encourage ideas that a top has been recorded. The greenback settled on its lowes against Brazil’s real yesterday (BRL5.1880). Look for a test on the gap from earlier this week between Monday’s high near BRL5.1270 and Tuesday’s low close to BRL5.1530.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, July 21: Did Japan Deliver a Fait Accompli to the US?

FX Daily, July 21: Did Japan Deliver a Fait Accompli to the US?

2021-07-21

Overview: The biggest rally in US equities in four months has helped stabilize global shares today. In the Asia Pacific region, Japan, China, and Australian markets advanced. Led by information technology and consumer discretionary sectors, Europe’s Dow Jones Stoxx 600 is up around 1.35% near the middle of the session.

SNB Sight Deposits: Inflation is there, CHF must Rise

SNB Sight Deposits: Inflation is there, CHF must Rise

2021-07-19

Sight Deposits have risen by +0.2 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

FX Daily, June 16: Will the Fed Talk the Talk?

FX Daily, June 16: Will the Fed Talk the Talk?

2021-06-16

With the outcome of the FOMC meeting awaited, the dollar is narrowly mixed in quiet turnover. The Scandis are the weakest (~-0.3%) among the majors, while the Antipodeans are the strongest (~+0.25%). JP Morgan’s Emerging Market Currency Index is snapping a three-day decline

FX Daily, June 11: US Yields Stabilize After Falling to Three-Month Lows

FX Daily, June 11: US Yields Stabilize After Falling to Three-Month Lows

2021-06-11

The 10-year US Treasury yield steadied after reaching a three-month low near 1.43%, despite the US CPI rising more than expected to 5% year-over-year. On the week, the decline of around a dozen basis points would be the largest in a year. Australia, New Zealand, and Italy benchmark yields have seen a bigger decline this week.

FX Daily, June 10: ECB Meeting and US CPI: Transitory Impact

FX Daily, June 10: ECB Meeting and US CPI: Transitory Impact

2021-06-10

The ECB meeting and the US May CPI report is at hand. The US dollar is consolidating at a higher level against most of the major currencies. Softer than expected, inflation readings are weighing on the Scandis, which are bearing the brunt. The US 10-year yield closed below 1.50% for the first time in three months yesterday, and this may have helped underpin the Japanese yen.

FX Daily, June 08: Marking Time ahead of the Week’s Big Events

FX Daily, June 08: Marking Time ahead of the Week’s Big Events

2021-06-08

The capital markets appear to be in a holding pattern ahead of this week’s big events, including the US CPI and the ECB meeting. Equities are little changed but with a heavier bias evident. Most of the large bourses in the Asia Pacific region were lower, except Australia, which eked out a small gain.

FX Daily, May 28: The Yuan Extends Gains, While Sterling’s First Close above $1.42 in Three Years Goes for Nought

FX Daily, May 28: The Yuan Extends Gains, While Sterling’s First Close above $1.42 in Three Years Goes for Nought

2021-05-28

The recovery of the US 10-year yield, so it is flat on the week near 1.61% coupled with month-end demand, is helping the US dollar firm. While the yen is bearing the burden on the week, with a 0.8% loss, the Antipodeans are leading the downside on the day.

FX Daily, May 26: RBNZ Joins the Queue, while Yuan’s Advance Continues

FX Daily, May 26: RBNZ Joins the Queue, while Yuan’s Advance Continues

2021-05-26

The decline in US rates and the doves at the ECB pushing back against the need to reduce bond purchases next month have seen European bond yields unwind most of this month’s gain. The inability of US shares to hold on to early gains yesterday did not deter the Asia Pacific and European equities from trading higher.

Tags: #USD,Brexit,China,commodities,Currency Movement,ECB,Featured,infrastructure,newsletter,U.K.