Japan’s yen is backward, at least so far as its trading direction may be concerned. This is all the more confusing especially over the past few months when this rising yen has actually been aiding the dollar crash narrative while in reality moving the opposite way from how the dollar system would be behaving if it was really happening. A dollar crash, or even just a true reflationary dollar drop, would be JPY negative (like 2017). Ever since the last one, during Euro$ #4, the trend for Japan’s currency is toward the worrisome side, all the illiquidity and shortage stuff what leads the dollar to rise against everyone else. US / Japan, 2018-2020 - Click to enlarge The simple truth is that rising yen is bad. You need look no further than the history of the past

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, credit spreads, currencies, Dollar, economy, eurodollar system, Featured, Federal Reserve/Monetary Policy, global dollar shortage, Japan, Japanese Yen, JPY, Markets, newsletter, Oil, WTI, wti futures curve, Yen

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Japan’s yen is backward, at least so far as its trading direction may be concerned. This is all the more confusing especially over the past few months when this rising yen has actually been aiding the dollar crash narrative while in reality moving the opposite way from how the dollar system would be behaving if it was really happening.

A dollar crash, or even just a true reflationary dollar drop, would be JPY negative (like 2017). Ever since the last one, during Euro$ #4, the trend for Japan’s currency is toward the worrisome side, all the illiquidity and shortage stuff what leads the dollar to rise against everyone else. |

US / Japan, 2018-2020 - Click to enlarge |

| The simple truth is that rising yen is bad. You need look no further than the history of the past few years suffering the increasing burden of Euro$ #4. JPY’s signal may have faded a bit from the middle part of the last decade, but it still contains a lot of relevant information and details about what we want to know. |

NYMEX WTI Futures, 2018-2020 - Click to enlarge |

| So, you’ll notice that since GFC2 and the massive monetary “flood” we keep hearing about, the direction JPY has taken contradicts that view. Certainly not dollar crash, for the most part. And while that has, again, added to the euro’s pull in making it seem like the dollar was going down (how it affects DXY, in particular), underlying this contrary move in the yen must instead be all the bad stuff consistent with an ongoing global dollar shortage which makes up the more general rising dollar behavior.

And it only gets worse, or at least the upward move which corroborates the concerns being likewise traded in bonds and now oil. Notice also which two dates stick out on the JPY chart over the last few months. First, once more, June 5 shows up yet again as peak reflation. Then, perhaps more importantly, mid-July, the week of July 25, when the yen takes another leg higher – meaning caution against everything from dollar crash to generalized dollar liquidity/abundance. |

Dollar Correlations, 2020 - Click to enlarge |

| These are not the signals you want to see if you’re Jay Powell with mid-September now looming. It isn’t the worst case, either, more of a broad, non-specific sense of foreboding rather than anything which makes something awful seem imminent; slanted in the wrong direction, sure, rather than crashing headlong into the calendar bottleneck point.

One more thing; mid-July also shows up in credit spreads in pretty much that same way. Spreads have been improving, but they remain unusually elevated particularly given all the presumed “support” for these markets (and liquidity overall) extended by the Federal Reserve. The central bank has worked into overdrive in its real toolkit (the financial media) pushing the inflation idea despite it being rejected in widespread fashion. |

Credit Spreads, 2017-2020 - Click to enlarge |

| Not only are spreads about as high right now as they were during the worst of 2018’s pretty shocking and disruptive landmine, they stopped improving right around…July 22. Like June 5, that’s also a date which seems to be repeated for all the wrong reasons (no “V”). |

Credit Spreads, 2020 - Click to enlarge |

| In other words, from JPY to WTI to credit spreads and bond yields, there’s quite a lot not to like about how everything was positioned and moving as August turned into September. So, is that a good sign that it hasn’t been worse with one week left to go before the underlying ebb in liquidity? Or foreboding with some things now more actively moving the wrong way (including stocks)?

JPY and T-bills, the repo twins, those will tell the story over the next week. And, of course, well beyond it. |

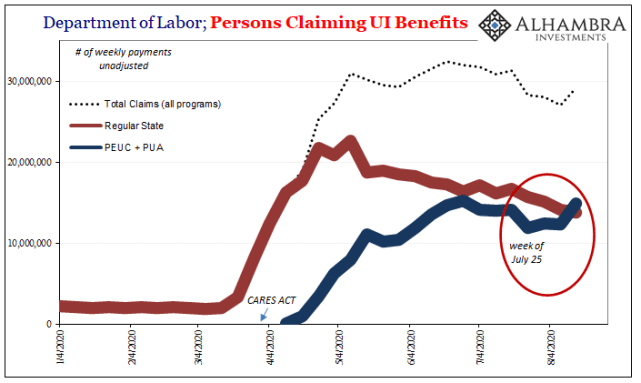

Personal Claiming UI Benefits, 2020 - Click to enlarge |

You Might Also Like

Part 2 of June TIC: The Dollar Why

Part 2 of June TIC: The Dollar Why

Before getting into the why of the dollar’s stubbornly high exchange value in the face of so much “money printing”, we need to first go back and undertake a decent enough review of the guts maybe even the central focus of the global (euro)dollar system.

COT Black: No Love For Super-Secret Models

COT Black: No Love For Super-Secret Models

As I’ve said, it is a threefold failure of statistical models. The first being those which showed the economy was in good to great shape at the start of this thing. Widely used and even more widely cited, thanks to Jay Powell and his 2019 rate cuts plus “repo” operations the calculations suggested the system was robust.

Fama 2: No Inflation For Old Central Banks

Fama 2: No Inflation For Old Central Banks

The Bureau of Labor Statistics reported that the core CPI in July 2020 jumped by the most (+0.62%) in almost thirty years. After having dropped month-over-month for three months in a row for the first time in its history, it has posted back to back gains the latest of which pushing the index back above its February level.

(No) Dollars And (No) Sense: Eighty Argentinas

(No) Dollars And (No) Sense: Eighty Argentinas

India like many emerging market countries around the world holds an enormous stockpile of foreign exchange reserves. According to the latest weekly calculation published by the Reserve Bank of India (RBI), the country’s central bank, that total was a bit less than half a trillion. While it sounds impressive, when the month began the balance was much closer to that mark.

The Global Engine Is Still Leaking

The Global Engine Is Still Leaking

An internal combustion engine that is leaking oil presents a difficult dilemma. In most cases, the leak itself is obscured if not completely hidden. You can only tell that there’s a problem because of secondary signs and observations.If you find dark stains underneath your car, for example, or if your engine smells of thick, bitter unpleasantness, you’d be wise to consider the possibility.

Second Wave Global Trade

Second Wave Global Trade

Unlike some sentiment indicators, the ISM Non-manufacturing, in particular, actual trade in goods continued to contract in May 2020. Both exports and imports fell further, though the rate of descent has improved. In fact, that’s all the other, more subdued PMI’s like Markit’s have been suggesting.

A Japanese Stall?

A Japanese Stall?

In sharp contrast to the sentimental deference towards central bank stimulus exhibited by Germany’s ZEW, for example, similar Japanese surveys are starting to describe potential trouble developing. Like Germany, Japan is a bellwether country and a pretty reliable indicator of global economy performance.

Meaning Mexico

Meaning Mexico

It took some doing, and some time, but Mexico has managed to bring its car production back up to more normal levels. For two months, there had been practically zero automaking in one of the biggest auto-producing nations. Getting back near where things left off, however, isn’t exactly a “V” shaped recovery; it’s only halfway.

Tags: $JPY,Bonds,credit spreads,currencies,dollar,economy,eurodollar system,Featured,Federal Reserve/Monetary Policy,global dollar shortage,Japan,Japanese yen,Markets,newsletter,OIL,WTI,wti futures curve,Yen