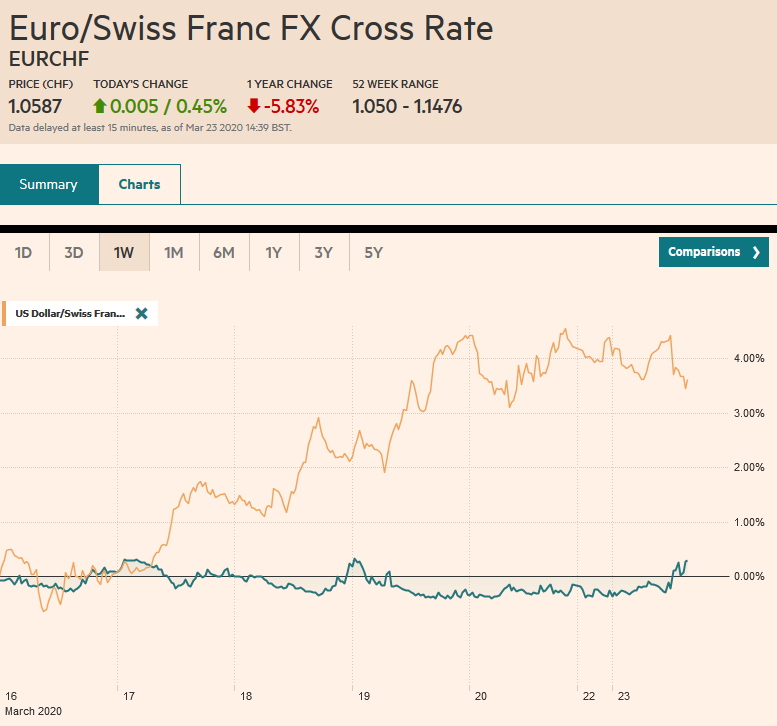

Swiss Franc The Euro has risen by 0.45% to 1.0587 EUR/CHF and USD/CHF, March 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: In HG Wells’ “War of the Worlds,” the common cold repelled a Martian invasion. Now, a novel coronavirus is disrupting everything and everywhere. Global equities continue to get hammered, though the apparent relative resilience of Japan may have spurred some buying of Japanese equities. Both the Nikkei and Topix posted gains, while equities in the regions tumbled after dropping more than 20% in the past two weeks. India’s main indices were off by more than 12% today. Europe’s Dow Jones Stoxx 600 gapped lower and is nursing a 4-5% loss on top of the roughly 35% markdown over the past

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Currency Movement, ECB, Featured, Federal Reserve, Germany, New Zealand, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.45% to 1.0587 |

EUR/CHF and USD/CHF, March 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: In HG Wells’ “War of the Worlds,” the common cold repelled a Martian invasion. Now, a novel coronavirus is disrupting everything and everywhere. Global equities continue to get hammered, though the apparent relative resilience of Japan may have spurred some buying of Japanese equities. Both the Nikkei and Topix posted gains, while equities in the regions tumbled after dropping more than 20% in the past two weeks. India’s main indices were off by more than 12% today. Europe’s Dow Jones Stoxx 600 gapped lower and is nursing a 4-5% loss on top of the roughly 35% markdown over the past five weeks. The S&P 500 has also lost around 35% over the same period, and it is trading off another 4% today. Yields are falling too, but seemingly more orderly than times last week. US and European yields are mostly 2-4 bp lower. Australian and New Zealand benchmark 10-year yields plummeted around 22 and 50 bp, respectively. New Zealand launched its first bond-buying program (QE). The dollar is firmer, with the dollar-bloc currencies and Scandis leading the downside, while the yen is the notable exception. Emerging market currencies continue to flounder. The JP Morgan Emerging Market Currency Index is off about 0.5% today and 11% during the past five-week slide. Gold and oil are lower. |

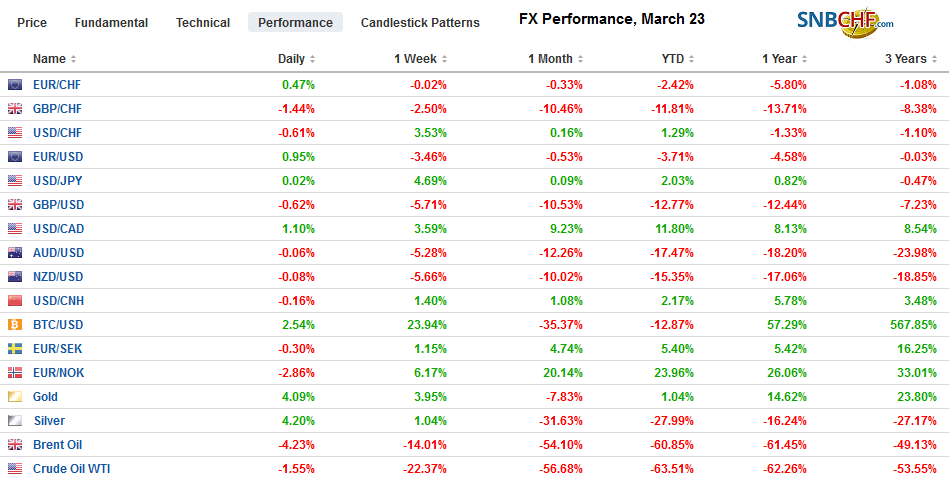

FX Performance, March 23 - Click to enlarge |

Asia Pacific

Japan’s officials gradually recognize that the Olympics will have to be postponed. It is partly a question of national pride, and also Prime Minister Abe’s grandfather as Prime Minister oversaw the 1964 Toyko Olympics. Given the athletic training necessary, some Olympic officials have warned of the difficulty in postponing and have discussed canceling the games. Separately, Japan was one of the first countries outside of China to be infected by the virus. However, Japan appears to be among the more resilient countries and some areas that had been locked down, are re-opening. Hypotheses range from the cultural emphasis on hygiene to the widespread use of masks (during allergy and cherry blossom season).

Australian Prime Minister Morrison announced a fiscal package before the weekend that brings its and the central bank’s efforts to an estimated 10% of GDP. A little more than half of it is assistance for small and medium-sized businesses. It also includes expanding the eligibility of collecting benefits and doubling the income support for jobseekers allowance. The second package of around A$66 bln (~$38 bln). The first package, announced March 12 was for about A$17.6 bln. Nearly 40% of the second package is to support businesses and charities. Unemployment benefits will be doubled, and some will be allowed to access pension savings without a penalty. The government will also offer A$40 bln of loan guarantees for small and medium-sized businesses. Last week, the RBA announced it would buy three-year bonds and target a 25 bp yield.

The Reserve Bank of New Zealand announced its first bond purchase program. It will buy NZ$30 bln of bonds over the next 12-months at a pace of about NZ$750 mln a week (though this week may be a bit less at ~NZ$500 mln). Last week, the central bank slashed the cash target rate 75 bp to 25 bp and reduced capital requirements. The government announced an NZ$12.1 bln support program that had seemed to spook the bond market. The RBNZ will exclude inflation-linked bonds from its purchases, which means it will buy a little more than half of the outstanding bonds, with allowances for the April maturities.

The dollar is trading within the pre-weekend range against the Japanese yen, but that does not imply narrow price action. Thus far, today’s range has been roughly JPY109.65-JPY111.25. There are two sets of expiring options that could be relevant today. The first is at JPY110 for almost $500 mln, and the other is for about $900 mln at JPY111.00-JPY111.10. The Australian dollar is continued to the lower end of its pre-weekend range, though here too, today’s range remains wide (~$0.5700-$0.5825). Last week’s low was near $0.5500, while the high was set at the start of the week near $0.6150. In the second half of last week, the US dollar moved into a new range against the Chinese yuan and (~CNY7.05-CNY7.1250) and remained in that range today. The PBOC set the dollar’s reference rate a bit weaker than most of the bank models implied. After falling sharply last week, money market rates stabilized today.

Europe

As German officials grasp the magnitude of the coming crisis, they have abandoned their fiscal restrictions, and the new debt issuance may help facilitate the ECB’s bond purchases. A decision to supplement this year’s budget with a 150 bln euros in new borrowings to support the economy is expected later today by the cabinet. The goal is to secure parliamentary approval by the end of the week. Some of the funds will be used for the short-term work subsidies (the government picks up 60% of wages stemming reduced hours as an effort to minimize unemployment). ECB President Lagarde indicated that the self-imposed constraints of central bank bond purchases, such as the 33% issuer limit, could be suspended if necessary. The new German issuance makes this less urgent. Separately, a 600 bln euro package that would include 400 bln euros of loan guarantees and 200 bln euros to fund corporate loans (through the KfW state development bank) and to equity stakes in German businesses if necessary. All told Germany is considering borrowing 350 bln euros.The Bundesbank’s Weidmann warned last week a recession is unavoidable, and the Finance Ministry warned of 5% contraction this year, which seems relatively mild. German Chancellor Merkel has entered self-quarantine after her doctor, who recently tested her, contracted the virus.

Ahead of the weekend, the UK presented its third fiscal initiative in less than two weeks. The first was for about GBP12 bln. The second was near GBP350 bln. The third is hard to put a price tag on, and Chancellor of the Exchequer Sunak declined to do so. The centerpiece is similar in some respects to Germany’s short-term work subsidies. For the first time, the UK, led by the Conservative Party, will pay for a portion (80%) of worker’s wages, whose jobs are at risk due to the virus, up to GBP2500 a month. The government will provide unlimited, 12-month interest-rate free loans to business. There are more funds for welfare support and assistance for renters and self-employed. The VAT will be suspended for three months at an estimated cost of GBP30 bln.

Nearly all Italy’s factories have been ordered to close for 15 days, as the country is besieged with the virus and rising fatalities. It is the worst hit outside of China. Spain’s formal national emergency has been extended for two more weeks. As the economic fallout mounts, there are more calls for joint European bonds. What is rejected in normal times, like German deficit spending, is more palatable in emergencies, and we discuss other examples below.

The Fed’s swap lines with the ECB may have taken the pressure off the cross-currency swaps, but the demand for dollars in Europe remains unsatiated. The attempt to buy the single currency faltered near $1.0770. Recall that low from late last month was about $1.0780. In early Asia, the euro made a marginal new low for the move (~$1.0635). The next important chart point is seen around $1.05. Sterling has ventured about a cent in both directions of the pre-weekend close near $1.1630. The pre-weekend low and also the lowest level in about 35 years was closer to $1.1410. Here too, the cross-currency swap basis has normalized without alleviating the pressure on sterling. The record low is about $1.0550.

America

With Senator Dr. Rand Paul testing positive for the coronavirus (after voting against two emergency bills to address the economic fallout) and interacting with several other senators in close quarters leading to two moving into self-quarantine, the Democrats had more sway in the upper chamber. They managed to block a large Senate bill that had swelled from $850 bln to more than $2 trillion in recent days. The dispute is unlikely to be resolved for at least a couple of days. Meanwhile, observers are pushing back and expressing concern about the inflationary nature of measures. In effect, the argument is that with the large parts of the economy shutting down, the extra spending will be more money chasing few goods–almost the textbook definition of inflation. President Trump seems to have been persuaded, and a president tweet indicated that more measures will be considered after a couple of weeks, and “we cannot let the cure be worse than the problem itself.” Meanwhile, St Louis Fed President Bullard warned that unemployment could reach 30% and the economy contract 50% in Q2, exceeding private-sector forecasts.

The Federal Reserve innovated at the end of last week, including short-dated municipal paper in its money market fund support facility. The Fed also bought more than half of the $500 bln Treasury purchases it announced last week and a little less than a third of the mortgage-back securities. The Fed will have to adjust the program. It could announce another $500 bln Treasury of purchases. But, it may be preferable to give volatile markets some regularity, as in announcing intentions to buy to X amount (e.g., $300 bln) for Y time-period (e.g., six-months). Alternatively, it could specify the amount but leaving it open-ended (e.g., until the economy is on the mend).

The Federal Reserve’s (likely) continued purchases of US Treasury’s come at a time when the supply will explode. The fiscal package that is being cobbled together may have grown as three-fold from the $850 bln price-tag discussed a week ago. Together this is very similar to what many proponents of the modern monetary theory have advocated and said was possible. However, the emergency is changing the political axis that only a crisis can. It is the conservative governments of Germany, the UK, and the US that are planning to take equity stakes in some large businesses. Corbyn in the UK and Sanders in the US were pilloried for such sentiments. The idea that the state should absorb some private-sector wage costs of the Social Democrat Chancellor of Germany has now been largely copied by the Tory government in the UK. A check from the federal government to every man, woman, and child in the US was dismissed by many in the Democrat debates, and now US politicians are tripping over themselves about the amount it should be.

At the end of last week, the US Trade Representative Office announced a three-month comment period on the removal of the punitive tariffs on medical supplies from China. While three months is not particularly useful in the current crisis, it has quietly removed tariffs and granted waivers on several medical items, including face masks, protective gowns, and exam gloves.

The US dollar had pulled back to CAD1.4150 ahead of the weekend after testing CAD1.4670 the day before. Pressure on the Loonie resumed today, and the greenback is knocking on CAD1.45 in the European morning. Initial support now is seen near CAD1.44. The Mexican peso’s slide is extending today after consolidating before the weekend. The dollar settled near MXN22.88 last Monday and now is near MXN24.83. Mexico and Brazil faced serious economic challenges before the coronavirus outbreak, and officials have been slow to respond. Highly urbanized (population density) reliant on public transportation leaves large swathes of the people are vulnerable.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Currency Movement,ECB,Featured,federal-reserve,Germany,New Zealand,newsletter