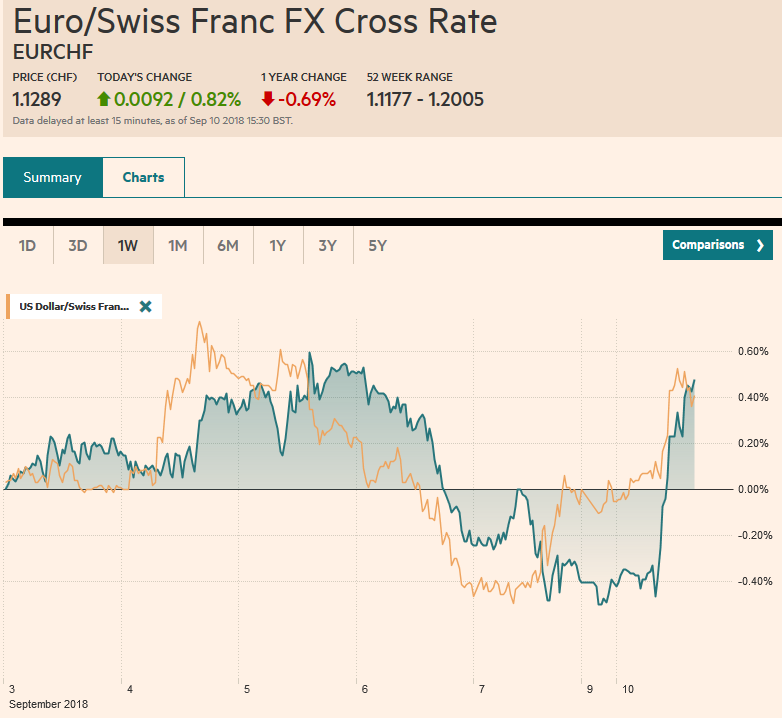

Swiss Franc The Euro has risen by 0.82% at 1.1289 EUR/CHF and USD/CHF, September 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates The US dollar’s pre-weekend gains were extended against most the major currencies, but the euro, sterling, and Australian dollar have recovered in the European morning. Emerging markets currencies are mixed. The euro fell to almost .1525 in following through selling. Today and tomorrow there are large options expiring at .15, which seen as solid support for the single currency. There are also about 640 mln euros struck at .1550 and 550 mln euros at .1650 that will be cut today. The intraday technical indicators suggest that the

Topics:

Marc Chandler considers the following as important: 4) FX Trends, CAD, CHF, EUR, Featured, GBP, JPY, newsletter, TLT, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.82% at 1.1289 |

EUR/CHF and USD/CHF, September 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar’s pre-weekend gains were extended against most the major currencies, but the euro, sterling, and Australian dollar have recovered in the European morning. Emerging markets currencies are mixed. The euro fell to almost $1.1525 in following through selling. Today and tomorrow there are large options expiring at $1.15, which seen as solid support for the single currency. There are also about 640 mln euros struck at $1.1550 and 550 mln euros at $1.1650 that will be cut today. The intraday technical indicators suggest that the $1.1600-$1.1610 may difficult to overcome. Before the weekend, the euro was sold against most of the crosses, including the Swiss franc, where the euro fell to its lowest level in a year. After holding last Friday’s low near CHF1.1185, the euro has risen above last Friday’s high, and a close above it (~CHF1.1245) would be a positive technical sign. Sterling briefly dipped below $1.29 in Asia, before recovering in Europe. There are two forces helping lift sterling today. First, there is a continuation of an emerging theme in which the fear of a Brexit with no deal eases and the EU appears to be softening its stance on the margins. Reports today suggest the EU may update to its mandate to the negotiators to strike a deal. |

FX Performance, September 10 - Click to enlarge |

The Indian rupee is the weakest(of the emerging market currencies (~-0.8%) following the widening of the Q2 current account deficit at the end of last week and ahead of the August trade deficit which is expected to show the impact of rising oil prices and the past currency depreciation. The Turkish lira is also weaker (-0.6%) after Q2 GDP was reported at 5.2% year-over-year (down from 7.4% in Q1). On the other hand, the South African range is about 0.75% stronger as it consolidates last week’s slide that saw the US dollar trade to almost ZAR1.570.

Sweden’s election has not led to a clear outcome. The center-left and the Alliance bloc got 144 and 143 seats respectively in the 349-seat parliament. The anti-immigration Democrats appear to have secured 62 seats, which is not as much as some polls projected, but better than 2014. The euro initially extended the pre-weekend sell-off and fell to SEK10.4255 (after closing ~ SEK10.4655), but has recovered in the European morning and appears set to test the SEK10.50SEK10.54 area. It marks retracement objectives of the pullback seen at the end of last week. The political uncertainty in Sweden encourages flows into Norway, and the krone is the strongest of the majors, up about 0.85% today.

Second, the UK’s data was mixed but mostly better than expected. This included a 0.3% rise in the new monthly GDP estimate (for July) and a three-month-over-three-month change of 0.6%. Services were stronger than expected, but the industrial sector lagged. Output rose 0.1% (vs. 0.2% expected) and manufacturing output fell 0.2% (vs +0.2% expected). On the other hand, construction output rose 0.5% (vs. -0.5% median forecast in the Bloomberg survey), and the trade deficit was considerably smaller than expected following a revision in the June series to show almost half the deficit that was initially estimated.

Sterling faces initial resistance in the $1.2960-$1.2980 area. The euro is consolidating its pre-weekend drop against sterling. Recall that early last week, the euro was near GBP0.9050. Last Friday’s low was near GBP0.8915. There are nearly 465 mln euros struck at GBP0.8955 that expire today.

The dollar has been confined to about 15 pips on either side of JPY111.00, which is the middle of the two-yen range that marks the near-term range. Japan revised its Q2 GDP upwards following the recent increase in capex, and the July current account surplus was a bit better than expected. The annualized Q2 GDP came in at 3% up from 1.9% of the initial estimate. Business spending increased by 3.1% rather than 1.3%, while consumption was unchanged at a 0.7% gain. The current account balance rose to JPY2.01 trillion (~$8.1 bln) from JPY1.176 trillion in June. Japan did report a minor (JPY1 bln) trade deficit. There is a JPY111 option for almost $395 mln that expires today. The greenback faces resistance near JPY111.40.

The US dollar continues to knock on the CAD1.3200 area. A convincing move above there will quickly target CAD1.33. NAFTA talks have reportedly stalled, and a new round of talks apparently has not been scheduled. However, the trade focus shifts today as the US and EU hold talks. Meanwhile, at any moment the US is expected to announce tariffs on $200 bln of Chinese goods.

Equities are mixed. he MSCI Asia Pacific Index fell 0.5% to extend its downdraft for an eighth consecutive session. It is at new lows since last September, slipping below chart support near 160.00. The retreat in China (-1.2% for the Shanghai Composite) and Taiwan (-1.1%) and India (-1.25%) offset the gains in Japan and Korea (the Nikkei and Kospi both up 0.3%). In Europe, the Dow Jones Stoxx 600 is up 0.3%, which is sustained would be the first back-to-back gain in a couple of weeks.

Of note, the recovery seen in Italian assets last week is continuing today. The equity market is up nearly 2% to lead European markets higher, helped by a 4.6% advance in bank shares after a nearly 6% rally last week, the most since January. Italian bonds are also recovering smartly. The 10-year yield is off 11 bp and slipping below 2.92%. It had finished August near 3.25%.

The US economic schedule includes CPI, PPI, and retail sales this week, but it is off to a slow start with only July consumer credit on tap for today. Also note that the US Treasury is set to sell $73 bln in 3, 10, and 30-year coupons this week, the second largest of these tenors since 2010. While supply increases note that September 15 is the last day that last year’s higher tax rate can be used to deduct contributions to corporate pension plans, which some have linked to increased demand for US Treasuries and starting next month, the Federal Reserve’s balance sheet unwind accelerates to $50 bln a month (from $40 bln).

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$CAD,$CHF,$EUR,$JPY,$TLT,Featured,newsletter