Back in February, Japan’s Cabinet Office reported that Real GDP in Japan had grown in Q4 2017 for the eighth consecutive quarter. It was the longest streak of non-negative GDP since the 1980’s. Predictably, this was hailed as some significant achievement, a true masterstroke of courage and perseverance. It was taken as a sign that Abenomics and QQE was finally working (never mind the four years). Those making that argument, however, advanced absurdity rather than rational analysis. Japan’s economy posted its longest continuous expansion since the 1980s boom as fourth quarter growth was boosted by consumer spending, moving Prime Minister Shinzo Abe’s revival plan a step closer to vanquishing decades of stagnation.

Topics:

Jeffrey P. Snider considers the following as important: 5) Global Macro, Bank of Japan, currencies, economy, Featured, Federal Reserve/Monetary Policy, GDP, Haruhiko Kuroda, Japan, Markets, Monetary Policy, newslettersent, Private Consumption, QE, QQE, they really don't know what they are doing, they really don't know what they are talking about, Yen

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Back in February, Japan’s Cabinet Office reported that Real GDP in Japan had grown in Q4 2017 for the eighth consecutive quarter. It was the longest streak of non-negative GDP since the 1980’s. Predictably, this was hailed as some significant achievement, a true masterstroke of courage and perseverance. It was taken as a sign that Abenomics and QQE was finally working (never mind the four years).

Those making that argument, however, advanced absurdity rather than rational analysis.

Japan’s economy posted its longest continuous expansion since the 1980s boom as fourth quarter growth was boosted by consumer spending, moving Prime Minister Shinzo Abe’s revival plan a step closer to vanquishing decades of stagnation.

This isn’t even conjecture, it is pure blind fantasy. To begin with, eight in a row hardly qualifies as proof of anything. By making it into something, conventional commentary showed instead just how far mainstream assessments have devolved. Pioneering the concept, if whatever in Japan is in any way positive that must be good; non-zero is now the standard.

But even among those eight quarters, growth never really mustered much heft. It was all very low-level stuff, the typical kind of upswing that doesn’t come close to qualifying as meaningful growth. The best quarter was Q1 2016 at 0.81% (Q/Q) and that was at the very beginning of the stretch. The average across all eight was merely 0.41%.

| Yesterday, the Cabinet Office reported that the streak has ended. Japan’s GDP in Q1 2018 was negative once again, falling 0.16%. In reality, that’s the second consecutive quarter of near-zero; though Q4 was positive it was barely (+0.14%), meaning that right now their economy is closer to the so-called technical definition of recession (that isn’t a technical definition) than it is to whatever Haruhiko Kuroda is rambling forward in extrapolations to the imaginary. |

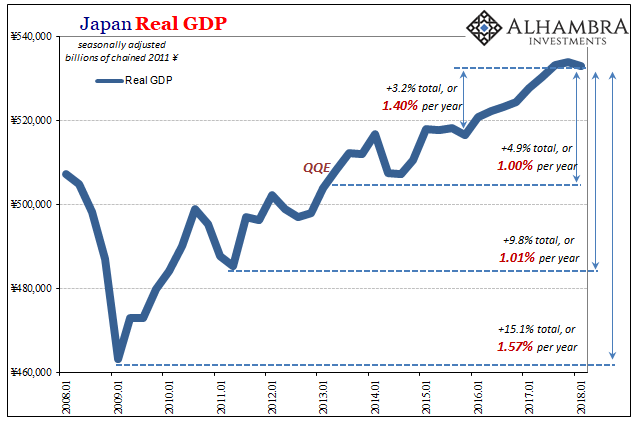

Japan Real Gross Domestic Product, Jan 2008 - 2018(see more posts on Japan Gross Domestic Product, ) - Click to enlarge |

| This, however, is normal for Japan’s economy. It is one beset by exactly this same pattern with or without QE’s or Abenomics. There are only small strings of low-level positive GDP almost regularly broken by technical recessions, near-technical recessions, or non-technical near-recessions; the ultimate result of which, Japan’s economy never, ever gets going (this should sound too familiar).

It never recovers and stays well outside the reach of true growth and health. This is actually the very definition of Japanification. As the term implies, it applies to Japan first and foremost. |

Japan Real Gross Domestic Product, Jan 2008 - 2018(see more posts on Japan Gross Domestic Product, ) - Click to enlarge |

| As you can see above, GDP performance is remarkably consistent – in a bad way. What should be clear, as well, is that it doesn’t matter what the Bank of Japan is doing, or not doing, or planning to not do in the future. Monetary policy is irrelevant because Japan also pioneered monetary policy divorced from money.

Trough to Peak, Japan’s economy since 2009 has managed only 15% growth. That’s horrendous, especially after nine years and following such a large contraction. It works out to about 1.57% on an annual basis. During this latest streak of eight quarters dating back to the “rising dollar”, GDP rose by 1.40% (annual basis) during them. |

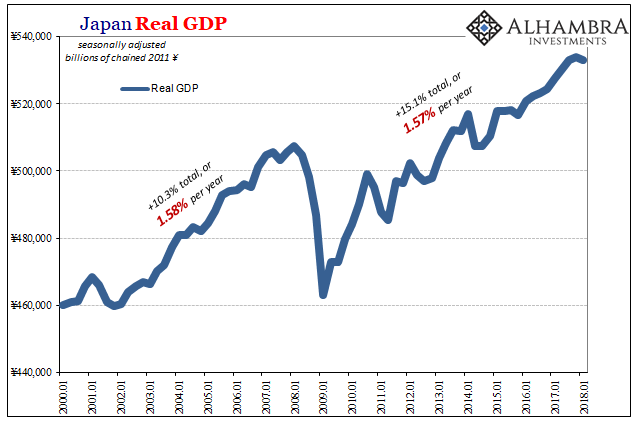

Japan Real Gross Domestic Product, Jan 2000 - 2018(see more posts on Japan Gross Domestic Product, ) - Click to enlarge |

| Not only that, during the prior worldwide “cycle” following the dot-com recession up until 2008 (for Japan, the peak was Q1 2008), Real GDP rose by 10.3%, which works out to an almost exact same 1.58% annual rate. What the Bank of Japan did during those years (ending the first two QE’s, actually raising rates twice) was very different from what it did during latter period, yet it all works out to the same lack of growth anyway.

And as demonstrably bad as it is for the overall economy, it is an order of magnitude worse for the Japanese people. |

. |

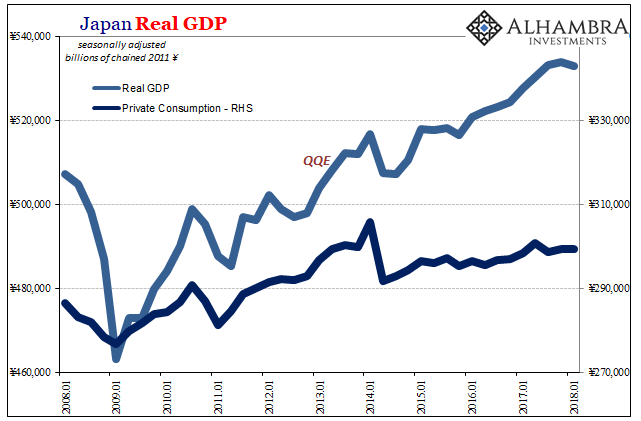

| Private consumption during this recent supposedly robust, dare I write, boom period was flat. Private consumption in 2018 is lower than it was at the end of 2013, and even down slightly from the quarter before QQE started.

This, too, is a constant feature of Japan’s economic landscape. Economic variability has little to do with the Japanese people, as they are left out of any small positives which means in non-linear terms they are getting less than nowhere. |

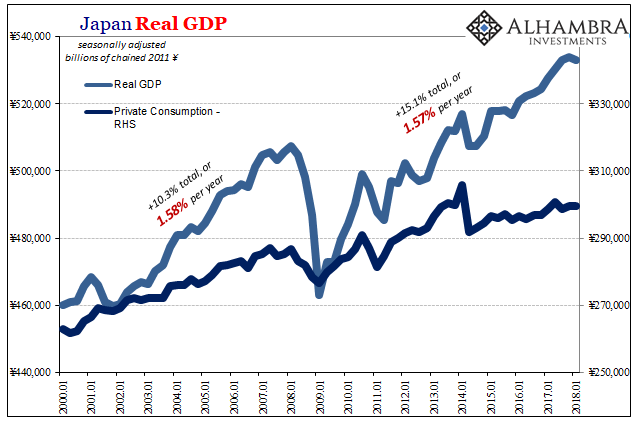

Japan Real Gross Domestic Product, Jan 2000 - 2018(see more posts on Japan Gross Domestic Product, ) - Click to enlarge |

To put some numbers on it, since modern GDP records began in Q1 1994, Real Private Consumption is up just 22% in 24 years. That’s 0.83% per year.

In other words, Japan is still Japan despite all the recent hoopla. That’s also a consistent piece of the puzzle, wherein whatever small and ultimately meaningless upswing the economy can manage the positive numbers lead to all sorts of hysterically absurd rhetoric and expectations. Every few years we hear about how Japan’s economy is about to break out of its multi-decade funk, usually because of the genius of Economists working at the Bank of Japan, only to find time and again that, no, nothing has changed at all.

The only thing that does is time.

For the rest of the global economy, the more immediate problem is Japan’s last two quarters. Since it isn’t the Japanese people (consumer spending) who are driving changes in GDP, what might that suggest about the state of globally synchronized growth as it late last year came into contact with renewed “dollar” uncertainty?

In very general terms, it would make sense for other countries to use Japan’s example as a warning of what not to do. Instead, everywhere else has followed the official Japanese response in detail. That has included dramatically overstating economic conditions at every single opportunity. Those eight quarters were not growth, and this ninth isn’t actually different from them. Japan is still Japan, bank reserves are still bank reserves, and it will all be called success no matter what.

Tags: Bank of Japan,currencies,economy,Featured,Federal Reserve/Monetary Policy,GDP,Haruhiko Kuroda,Japan,Markets,Monetary Policy,newslettersent,private consumption,QE,QQE,they really don't know what they are doing,they really don't know what they are talking about,Yen