Summary: The technical and fundamental case for the euro has weakened. Rate differentials have begun moving back in the US favor. France’s Macron and Japan’s Abe have sunk in the polls lower than Trump. The release of the US employment data before the weekend ushers in a three-week period before the Jackson Hole confab at the end of the month that will start the new phase. In September, the FOMC is likely to announce that it will begin not fully rolling over the maturing proceeds of its swollen balance sheet. The ECB will probably announce that it will continue to expand its balance sheet in the first half of 2018 albeit at a reduced pace. Perhaps the fundamental case for the euro was more compelling than we

Topics:

Marc Chandler considers the following as important: EUR, Featured, Federal Reserve, FX Trends, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Summary:

The technical and fundamental case for the euro has weakened.

Rate differentials have begun moving back in the US favor.

France’s Macron and Japan’s Abe have sunk in the polls lower than Trump.

The release of the US employment data before the weekend ushers in a three-week period before the Jackson Hole confab at the end of the month that will start the new phase. In September, the FOMC is likely to announce that it will begin not fully rolling over the maturing proceeds of its swollen balance sheet. The ECB will probably announce that it will continue to expand its balance sheet in the first half of 2018 albeit at a reduced pace.

Perhaps the fundamental case for the euro was more compelling than we appreciated in Q2. As we anticipated, the populist-nationalist assault would not secure a beachhead in Europe. When combined with the continued above trend growth and a spike in inflation, it forced investors who had become underweight European exposure to scramble. After selling about 100 bln euros of European equities in 2016, foreign investors returned around a third in H1 17.

At the same time, skepticism increased that the Trump Administration can deliver its economic agenda. At the same time, US data consistently underwhelmed expectations, and core inflation fell. There were a couple of jobs reports that in hindsight proved to be quirks rather than signs of a dramatic weakening of trend, but at the time, contributed to skepticism over the trajectory of monetary policy.

Neither the technical nor macro economic considerations are as compelling. It is true that the political climate in the US leaves much to be desired. This does not seem likely to change anytime soon. However, what is changing in European politics. Just like the consensus was slow to recognize and appreciate that the fragmented multiparty political systems act as a bulwark against populist-nationalism, it is slow to see the underlying contradictions within Europe are unresolved and could re-emerge quickly.

JapanThere is a small possibility that the Bank of Japan raises its target for 10-year JGB yield from zero to 10 bp. UK Prime Minister May is expected to deliver an important address on Brexit. Germans are expected to give Merkel a fourth term as Chancellor. Electoral considerations seemed to limit the EU issues that the German government was willing to entertain. When the election is out of the way, Merkel may perceive having greater flexibility to address EU issues. |

. |

GermanyThe wave of optimism in Europe and among investors in response to the French elections was not simply about the turning back the National Front, but it was also the possibility of renewed Franco-German cooperation, which had seemed to wither on the vine in recent years. This project was recognized as all the more important given the UK’s decision to leave the EU and seeming unilateralist (not isolationist) thrust of the US. The necessary precondition is that the France had to regain the authority to do so by getting its own economic and fiscal house in order. |

. |

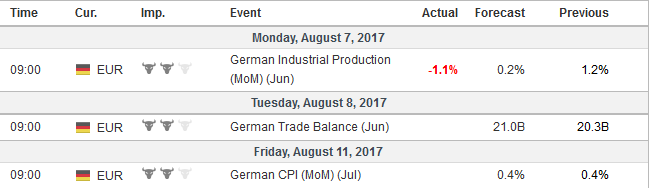

United KingdomRecall that, Fillon, the center-right candidate in the French presidential election, campaigned in part as if to bring to France what Thatcher brought to the UK. Although Fillon did not end up winning, of course, the thrust of his program appears have been adopted by Macron. Labor reforms made to increase the flexibility of hiring, firing and wage settlement, tax cuts wealthy and dramatic spending cuts is the neoliberal agenda. Macron’s honeymoon in France is over. His support has fallen to levels below Trump’s in the US. Consider Japan’s government too. There is no populist-nationalist challenge to Abe, who articulates a stronger nationalist vision, but the government’s support had fallen to 24% before the recent cabinet reshuffle, according to a poll conducted for the Mainichi newspaper. UK Prime Minister’s May’s support does not look much better either. Italy as a technocrat government, and although an election must be held next spring, the electoral rules have not been decided. Nonetheless, it is notable that polls suggest a loose coalition of the EMU-skeptical center-right is polling ahead of the governing center-left. Meanwhile, the July composite eurozone PMI fell to 55.7, the lowest the level since January. It is the second consecutive decline. The Q2 average was 56.6. The region’s economic momentum appears to have peaked. This week’s industrial production reports will support this hypothesis, but with the initial look at Q2 GDP recently reported, June data may not have the heft to move the market. Spain has already reported a decline, and output in France also likely fall. German industrial output has been very strong this year but appears poised to slow. |

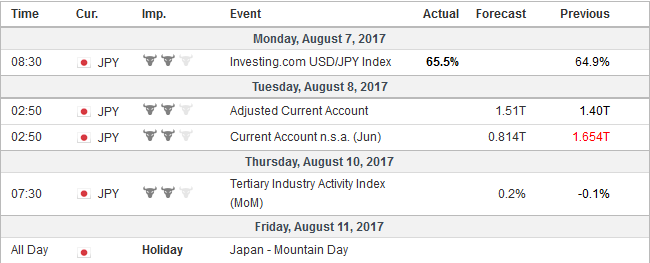

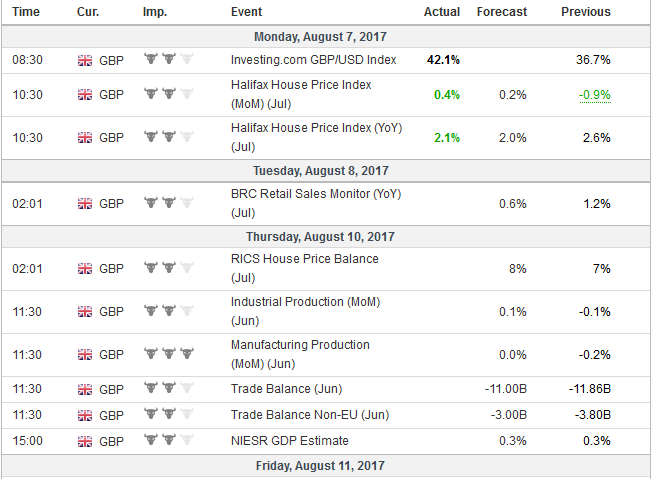

Economic Events: United Kingdom, Week August 07 - Click to enlarge |

United StatesThe dollar’s decline corresponded with a decline in the premium the US offered over Germany. This consideration is also changing. The two-year premium stands at 2.04%. It had fallen from nearly 2.23% in early March to about 1.92%, where it had bottomed previously. It is about the 50 and 100-day moving averages that converged near 2.0%. The 10-year interest rate differential fell from 2.35% at the end of last year to 1.70% on July 18. It has edged higher since, rising in 10 of the 13 sessions since hitting the low. It stands finished last week at 1.79%, in between the 20-day moving average (1.75%) and the 50-day moving average (1.83%). Although we first suggested that the Fed would announce the beginning of its balance sheet operations at the September FOMC meeting, our confidence has grown. A survey of prime dealers found they too have shifted to this view. Comments by officials have also been encouraging, and we expect Dudley’s speech in the week ahead to be consistent with this. FOMC members may find comfort in this week’s CPI report. July core prices likely rose 0.2%, which would be the fastest monthly pace since February. A 0.2% rise in the headline would bring it to 1.8% (from 1.6%). The slowdown in auto sales and cuts in production and employment announced is worrisome, but manufacturing employment is doing considerably better than last year. Through July, 12k new manufacturing jobs have been added each month on average. Last year, manufacturing employment fell by an average of one thousand a month. In July 16k new manufacturing jobs were created, and June’s one thousand gain was revised to 12k, which fully accounted for the upward revision in the national estimate The broader jobs report also will probably be to the Fed’s likely. The unemployment rate returned to its cyclical and multi-year low of 4.3%. The participation rate increased to 62.9% in July from 62.7% in May. Average hourly earnings rose 0.343% and were rounded down to 0.3%, but it is the strongest since last October. Jobs growth this year has averaged 184k, which is essentially unchanged from last year’s 187k average. The diffusion index rose to 63.2 from 62.5, nearly nine index points above the recent low. The concerns from some corners that the Fed’s tightening is premature rings hollow. Financial conditions have eased. The Chicago Fed’s Financial Conditions measure fell to new cyclical lows at the end of July (-0.94) and is approaching the modern extreme recorded July 1993 (-1.02). |

. |

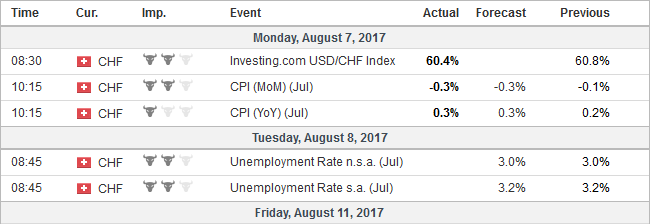

Switzerland |

Economic Events: Switzerland, Week August 07 - Click to enlarge |

Some are critical that the Fed should not be considering tightening given that inflation is below target and the robust jobs growth signals the existence of more slack than full employment would suggest. Full employment is not a directly observable phenomenon, and its importance is in the medium and long-term. Why shouldn’t it be able to be overshot in what is turning into one of the longest expansions on record? There is little evidence that the Fed’s tightening has had a material impact.

The argument sketched here is that many of the key fundamental considerations that have has fallen and the implications for EMU are under-appreciated. The July PMI is another yellow light, and if it were to fall for a third month here in August, it may be difficult for the ECB to ignore it when it meets next month. In the US, monetary policy remains very much in play, even if the odds of fiscal stimulus (tax cuts, infrastructure spending, and deregulation) seem to diminish.

Tags: #USD,$EUR,Featured,Federal Reserve,newsletter