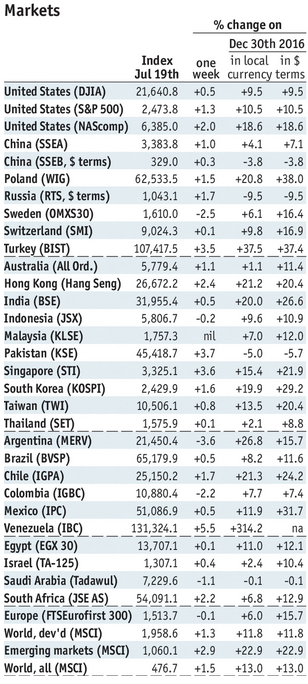

Stock Markets EM FX was mixed on Friday, but largely firmer over the entire week. Top performers were BRL, KRW, and ZAR, while the worst were ARS, MXN, and RUB. FOMC meeting this week poses some potential risks to the global liquidity story that’s supporting EM. Within EM, the low inflation/easy monetary policy narrative should continue with data and events this week. Stock Markets Emerging Markets, July 22 - Click to enlarge Singapore Singapore reports June CPI Monday, which is expected to rise 0.7% y/y vs. 1.4% in May. It then reports June IP Wednesday, which is expected to rise 6.5% y/y vs. 5.0% in May. Price pressures remain low while the real sector has been a bit sluggish. As such, the MAS may maintain its

Topics:

Win Thin considers the following as important: emerging markets, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Stock MarketsEM FX was mixed on Friday, but largely firmer over the entire week. Top performers were BRL, KRW, and ZAR, while the worst were ARS, MXN, and RUB. FOMC meeting this week poses some potential risks to the global liquidity story that’s supporting EM. Within EM, the low inflation/easy monetary policy narrative should continue with data and events this week. |

Stock Markets Emerging Markets, July 22 - Click to enlarge |

SingaporeSingapore reports June CPI Monday, which is expected to rise 0.7% y/y vs. 1.4% in May. It then reports June IP Wednesday, which is expected to rise 6.5% y/y vs. 5.0% in May. Price pressures remain low while the real sector has been a bit sluggish. As such, the MAS may maintain its forward guidance to keep the current policy neutral “for an extended period” at the semi-annual policy meeting in October. TaiwanTaiwan reports June IP Monday, which is expected to rise 1.9% y/y vs. 0.8% in May. It then reports Q2 GDP Friday, which is expected to grow 2.3% y/y vs. 2.6% in Q1. The economy remains a bit sluggish, even as price pressures remain low. This should allow the central bank to keep rates on hold at the next quarterly policy meeting in September. MexicoMexico reports mid-July CPI Monday, which is expected to rise 6.25% y/y vs. 6.30% in mid-June. If so, inflation is topping out with some help from the firmer peso. As such, we think rate hikes have ended for now. Next policy meeting is August 10, no change is expected then. Mexico then reports June trade Thursday. South AfricaSouth Africa reports Q2 unemployment Tuesday, which is expected to remain steady at 27.7%. The real sector remains weak. SARB surprised markets with a 25 bp cut to 6.75% last week, a little earlier than expected. Now that the door has been opened, further cuts are likely at the September 21 and November 23 meetings. BrazilCOPOM meets Wednesday and is expected to cut rates 100 bp to 9.25%. IPCA inflation was only 2.78% y/y in mid-July, the lowest since 1999. This is below both the 4.5% target and the 3.0-6.0% target range, and so 100 bp rate cuts are likely to continue. Brazil then reports central government budget data Thursday, followed by consolidated data Friday. KoreaKorea reports Q2 GDP Thursday, with growth expected at 2.7% y/y vs. 2.9% in Q1. It then reports June IP Friday, which is expected to rise 1.3% y/y vs. 0.1% in May. Inflation remains low while the real sector is sluggish, and so we see steady rates into 2018. Next policy meeting is August 31, no change is expected then. TurkeyCentral Bank of Turkey meets Thursday and is expected to keep rates steady. Inflation has been falling but at 10.9% y/y in June, it remains too far above the 3-7% target range to start an easing cycle. We do not think last week’s cabinet shuffle will have any policy implications, since President Erdogan calls all the shots anyway. ColombiaColombian central bank meets Thursday and is expected to cut rates 25 bp to 5.5%. A small handful looks for a 50 bp cut to 5.25%. IP and retail sales contracted in May, while CPI inflation has fallen to 4%, right at the top of the 2-4% target range. We believe easing will continue into Q4. RussiaCentral Bank of Russia meets Friday and is expected to keep rates steady at 9.0%. However, the market is split. Of the 32 analysts polled by Bloomberg, 12 see a 25 bp cut and 20 see no cut. CPI rose 4.4% y/y in June, up from the 4.1% trough in April and May and above the 4% target. The central bank has warned inflation may rise further, so it’s a close call. We lean towards no move but acknowledge risks of a 25 bp cut. |

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, July 2017 Source: economist.com - Click to enlarge |

Tags: Emerging Markets,Featured,newsletter