Swiss Economicblogs.org

Swiss Economicblogs.org

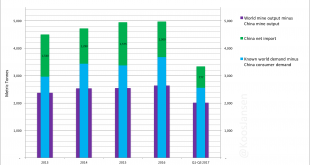

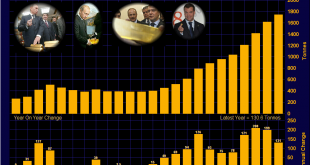

– Gold prices rise to $1,326/oz on concerns China may slow U.S. Treasury buying – Equities fell sharply on the report as did Treasurys and the U.S. dollar – Chinese officials think U.S. debt is becoming less attractive compared to other assets – Trade tensions could provide a reason to slow down or halt U.S. debt purchases – U.S. dollar vulnerable as China remains biggest buyer of U.S. sovereign debt – Currency wars to...

Read More »Gold Prices Rise To $1,326/oz as China U.S. Treasury Buying Report Creates Volatility