It is impossible to grasp the meaning of the idea of sound money if one does not realize that it was devised as an instrument for the protection of civil liberties against despotic inroads on the part of governments. Ideologically it belongs in the same class with political constitutions and bills of right. So wrote Ludwig von Mises in The Theory of Money and Credit in 1912. And further: The sound-money principle has two aspects. It is affirmative in approving the market’s choice of a commonly used medium of exchange. It is negative in obstructing the government’s propensity to meddle with the currency system. Against this backdrop, modern day monetary systems appear to have been drifting farther and farther away from the sound money principle in the last

Topics:

Thorsten Polleit considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

It is impossible to grasp the meaning of the idea of sound money if one does not realize that it was devised as an instrument for the protection of civil liberties against despotic inroads on the part of governments. Ideologically it belongs in the same class with political constitutions and bills of right.

So wrote Ludwig von Mises in The Theory of Money and Credit in 1912. And further:

The sound-money principle has two aspects. It is affirmative in approving the market’s choice of a commonly used medium of exchange. It is negative in obstructing the government’s propensity to meddle with the currency system.

Against this backdrop, modern day monetary systems appear to have been drifting farther and farther away from the sound money principle in the last decades.

In all countries of the so-called free world, money represents nowadays a government controlled irredeemable paper, or “fiat,” money standard. The widely held view is that this money system would be compatible with the ideal of a free society and conducive to sustainable output and employment growth.

To be sure, there are voices calling for caution. Taking a historical viewpoint, Milton Friedman stated:

The world is now engaged in a great experiment to see whether it can fashion a different anchor, one that depends on government restraint rather than on the costs of acquiring a physical commodity.

Irving Fisher, evaluating past experience, wrote: “Irredeemable paper money has almost invariably proved a curse to the country employing it.”

The primary cause for concern rests on a key characteristic of government controlled paper money: the system’s unrestrained ability to expand money and credit supply. In contrast, under the (freely chosen) gold standard, money (e.g., gold) supply was expected to increase as well over time, but only in proportion to how the economy expanded—i.e., an increase in money demand, brought about by an increase in economic activity, would bring additional gold supply to the market (by, for instance, increased mining which would become increasingly profitable). As such, the gold standard puts an “automatic break” on money expansion—the latter would be, at least in theory, related to the economy’s growth trend.

The government controlled fiat money system has no inherent limit to money and credit expansion. In fact, quite the opposite holds true: Central banks, the monopolistic suppliers of governments’ money, have actually been deliberately designed to be able to change money and credit supply by actually any amount at any time.

To prevent abuse of their unlimited power over the quantity of money supply, most central banks have been granted political independence over the past decades. This has been done in order to keep politicians who, in order to get reelected, from trading off the benefits of a monetary policy induced stimulus to the economy against future costs in the form of inflation. In addition, many central banks have been mandated to seek low and stable inflation—measured by consumer price indices—as their primary objective. These two institutional factors—political independency and the mandate to preserve the purchasing power of money—are now widely seen as proper guarantees for preserving sound money.

Be that as it may, Mises’s concerns appear as relevant as ever:

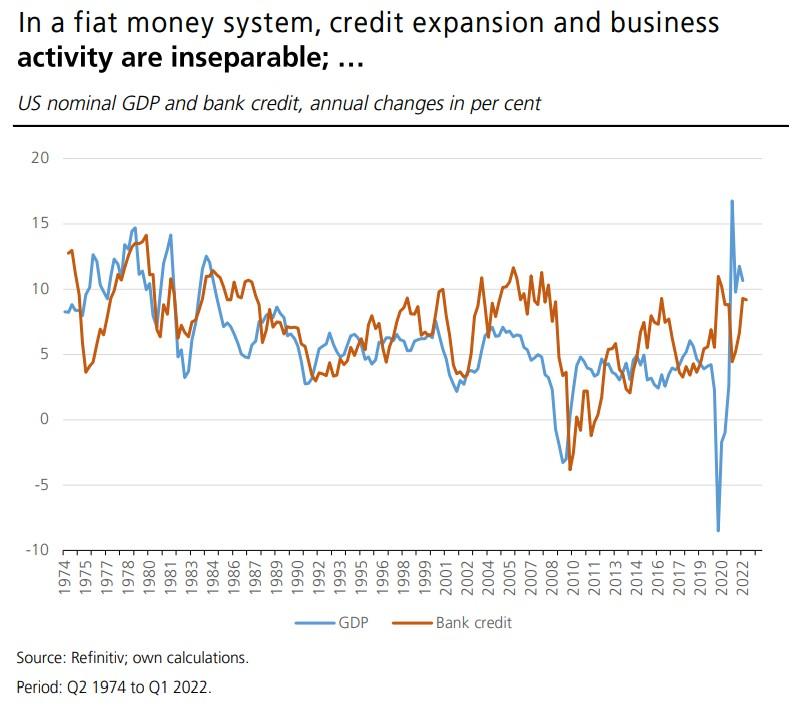

Whereas the objective to preserve the value of government controlled paper money appears to be a laudable one, the truth is that it is (virtually) impossible to deliver on such a promise. In fact, there are often overwhelming political-economic incentives for a society to increase its money and credit supply, if possible, in order to influence societal developments according to ideological preset designs rather than relying on free market principles. This very tendency is particularly evidenced by the fact that central banks are regularly called upon to take into account output growth and the economy’s job situation when setting interest rates. And these considerations are what seem to cause severe problems in a paper money system if and when there is no clear-cut limit to money and credit expansion. To bring home this point, it is instructive to take a brief look at the relationship between credit and nominal output and “wealth” growth (which is defined here, for simplicity, as gross domestic product plus stock market capitalization). The figure below shows the annual changes of US nominal gross domestic product (GDP) and bank credit in percent from 1974 to the beginning of 2022. As can be seen, both series are positively correlated in the period under review: On average, rising output had been accompanied by rising bank credit and vice versa. It is actually an instructive illustration of the Austrian business cycle theory (ABCT), which holds that the expansion of bank credit is not only closely associated with a boom-and-bust cycle, affecting both real magnitudes and goods prices, but its driving force. |

. |

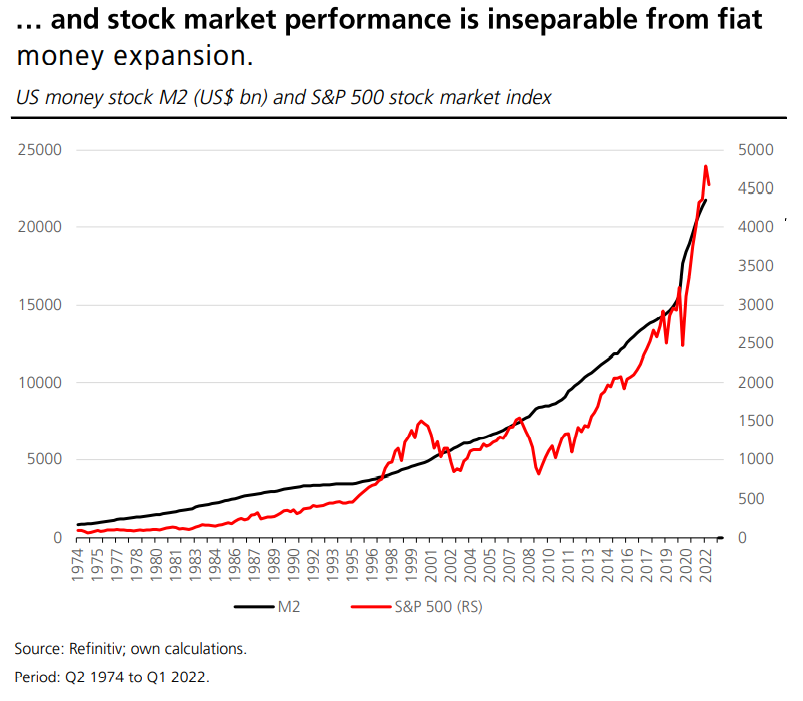

| Also from 1974 to the beginning of 2022, the following figure shows the US money stock in billions of US dollars and the S&P 500 stock market index. The rising money stock is basically the re of result of the expansion of bank credit—through which new money is created. As can be seen, the development of the money stock trends on the same wavelength as the stock market. Why? On the one hand, the increase in nominal GDP over time is reflected in rising values of corporate valuations. On the other hand, the rising money stock pushes goods prices up, including stock prices.

In other words: The stock market performance is—sometimes more so, sometimes less so—attributable to the fiat-money-caused goods price inflation. From the end of 2019 to the first quarter 2022 the US central bank increased the money stock M2 by 43 percent, while the stock market gained 63 percent in the same period. As the increase in the money stock helped inflating nominal GDP, it also translated into (substantially) higher stock prices. In other words: The monetary expansion caused “asset price inflation.” |

. |

Looking at these charts, the message seems to be: The chronic increase in credit and money supply has, on average, been “quite positive” for output and wealth. However, this would be a rather shortsighted interpretation. For a fiat money system, the expansion of credit and money makes a few benefit at the expense of many others. What is more, its “invisible effect” is that it prevents all the economic success and the resulting distributive income and wealth effects that had occurred had there not been an issuance of additional credit and fiat money.

As even classical economic theorists warn, a money- and credit-induced stimulus to the economy is (as the ABCT shows) short-lived and will eventually lead to inflation, as outlined by David Hume in 1742:

Augmentation (in the quantity of money) has no other effect than to heighten the price of labour and commodities…. in the progress towards these changes, the augmentation may have some influence, by exciting industry, but after the prices are settled … it has no manner of influence.

However, the today’s intellectual conviction of the economic mainstream, which is dominated by Keynesian economics, is that by lowering interest rates the central bank can stimulate growth and employment. So it does not take wonder that, especially so in periods in which inflation is seen to be “under control,” central banks are pressured into an “expansionary” monetary policy to fight recession. In fact, it is widely considered “appropriate” if monetary policy keeps borrowing costs at the lowest level possible.

In the work of Mises one finds a well-founded criticism of this broadly held conviction. He writes:

Public opinion is prone to see in interest nothing but a merely institutional obstacle to the expansion of production. It does not realize that the discount of future goods as against present goods is a necessary and eternal category of human action and cannot be abolished by bank manipulation. In the eyes of cranks and demagogues, interest is a product of the sinister machinations of rugged exploiters. The age-old disapprobation of interest has been fully revived by modern interventionism. It clings to the dogma that it is one of the foremost duties of good government to lower the rate of interest as far as possible or to abolish it altogether. All present-day governments are fanatically committed to an easy money policy.

Mises also outlines what the propensity to lower interest rates and increasing money and credit supply does to the economy. The Austrian school’s monetary theory of the trade cycle maintains that it is monetary expansion which is at the heart of the economies’ boom and bust cycles. Overly generous supply of money and credit induces what is usually called an “economic upswing.” It is wake, economic growth increases and employment rises.

With the liquidity flush, however, come misalignments, a distortion of relative prices, so the theoretical reasoning is. Sooner or later, the artificial money and credit-fueled expansion is unsustainable and turns into a recession. In ignorance and/or in failing to identify the very forces responsible for the economic malaise, namely excessive money and credit creation in the past, falling output and rising unemployment provoke public calls for an even easier monetary policy.

Central banks are not in a position to withstand such demands if they do not have any “anchoring”—that is a (fixed) rule which restrains the increase in money and credit supply in day-to-day operations. In the absence of such a limit, central banks, confronted with a severe economic crisis, are most likely to be forced to trade off the growth and employment objective against the preserving the value of money—thereby compromising a crucial pillar of the free society.

Seen against this backdrop, today’s monetary policy actually resembles a lawless undertaking. The zeitgeist holds that “inflation targeting” (IT)—the so-called state-of-the-art concept, from the point of view of most central banks—will do the trick to prevent monetary policy from causing unintended trouble. In practice, however, IT does not have any external anchor. Under IT, it is the central bank itself that calculates inflation forecasts which, in turn, determine how the bank set interest rates; setting a quantitative limit to money and credit expansion is usually not seen as a policy objective. IT can thus hardly inspire confidence that it will mitigate the threat to the value of paper money stemming from governments (in the form of fraud/misuse) and/or politically independent monetary policy makers (in the form of policy mistakes).

The return to “monetary policy without rule” began in the early 1990s, when various central banks abandoned monetary aggregates as a major guide post for setting interest rates. It was argued that “demand for money” had become an unstable indicator in the “short term” and that, as such, money could no longer be used as a yardstick in setting monetary policy, particularly so as policy makers were making interest rate decisions every few weeks. However, that guide post has not been replaced with anything since then.

In view of the return of discretion in monetary policy, it might be insightful to quote Hayek’s concern; namely, that inflation “is the inevitable result of a policy which regards all the other decisions as data to which the supply of money must be adapted so that the damage done by other measures will be as little noticed as possible.” In the long run, such a policy would cause central banks to become “the captives of their own decisions, when others force them to adopt measures that they know to be harmful.”

Echoing the warning that Ludwig von Mises gave back in The Theory of Money and Credit, Hayek concluded:

The inflationary bias of our day is largely the result of the prevalence of the short-term view, which in turns stems from the great difficulty of recognising the more remote consequences of current measures, and from the inevitable preoccupation of practical men, and particularly politicians, with the immediate problems and the achievements of near goals.

What can we learn from all this? The inherent risks of today’s paper money standard—the very ability of expanding the stock of money and credit at will by actually any amount at any time—are no longer paid proper attention: Putting a limit on the expansion of money and credit does not rank among the essential ingredients for “modern” monetary policy making. The discretionary handling of paper money thus increases the potential for a costly failure substantially. A first step for moving back towards the sound money principle—which is doing justice to the ideal of a free society—would be to make monetary policy limiting—e.g., stopping altogether—money supply growth.

You Might Also Like

Lighting the Gas under European Feet: How Politicians and Journalists Get Energy So Wrong

Lighting the Gas under European Feet: How Politicians and Journalists Get Energy So Wrong

2022-05-12

“We live in a time where few understand how things get made. It is fine to not know where stuff comes from, but it isn’t fine to not know where stuff comes from while dictating to the rest of us how the economy should be run.” —Doomberg

No, It’s Not the Putin Price Hike, No Matter What Joe Biden Claims

No, It’s Not the Putin Price Hike, No Matter What Joe Biden Claims

2022-05-05

Politicians love their buzzwords and talking points, and the Joe Biden White House and the Democratic Party use them as much or more than when Donald Trump and the Republicans ran Washington’s freak show. Last year, the mantra from the Biden administration was that inflation was “transitory,” meaning that the inflation would not last long.

Elon Musk’s Twitter Gambit and What It Means to the “Clique in Power”

Elon Musk’s Twitter Gambit and What It Means to the “Clique in Power”

2022-04-30

Elon Musk’s bid to take over Twitter and turn it into a private company has apparently been successful. Now the real action begins. Musk’s buyout exposes the Big Digital media complex to unwanted and unwonted competition, while threatening to loosen its near-total control of information and opinion.

Why Putin Probably Hasn’t Doomed the Dollar

Why Putin Probably Hasn’t Doomed the Dollar

2022-03-10

In this episode of Radio Rothbard, Ryan McMaken and Tho Bishop look at the economic consequences of Russia’s invasion of Ukraine. What has been the damage from America’s weaponization of the dollar? Is Russia likely to return to the gold standard? What may be the fallout in Europe?

Ukraine’s Regime Is Now Kidnapping Fathers for Military “Service”

Ukraine’s Regime Is Now Kidnapping Fathers for Military “Service”

2022-03-01

As the Ukraine regime has imposed martial law in the wake of the Russia invasion, it has also apparently imposed a new near-universal conscription order. USA Today reports: The Ukraine State Border Guard Service has announced that men ages 18 to 60 are prohibited from leaving the country, according to reports.

Andrew Moran: NBA skills trainer on Tim Hardaway Jr work ethic & Starting team Hardaway in Miami

Andrew Moran: NBA skills trainer on Tim Hardaway Jr work ethic & Starting team Hardaway in Miami

2022-01-27

In this segment, Andrew talks about Tim Hardaway Jr work ethic, reviving his career in Dallas, and building Team Hardaway in Miami which gives local kids an opportunity to travel the country and play basketball.

Stop Trying to Turn Economics into a Branch of Psychology

Stop Trying to Turn Economics into a Branch of Psychology

2022-01-22

Recently, a relatively new economics called behavioral economics (BE) has started to gain popularity. Its practitioners, such as Daniel Kahneman, Vernon Smith, and Richard Thaler, were awarded Nobel Prizes for their contribution in the field of BE.

Germany’s New Green Stimulus Plan Won’t Fix the Economy

Germany’s New Green Stimulus Plan Won’t Fix the Economy

2022-01-21

Recently, there has been a debate in Germany on the constitutionality of additional government borrowing of €60 billion. The borrowing is debated because Germany has a constitutional debt brake. The debt brake limits the possibility of the government to indebt itself and pushes it toward a balanced budget in normal times.

Tags: Featured,newsletter