“The strong economic recovery will not get interrupted by inflation or a credit crunch, and the market will soon reach 4,500.” – Ed Yardeni via Advisor Perspectives After discussing BofA’s view of why the market could drop to 3800, I thought it fair to discuss a more optimistic view. BofA’s view of a market correction was a function of the more exuberant “optimism” in the market. To wit: “This analysis is interesting, particularly when analysts are rushing to upgrade both economic and earnings estimates.” “More importantly, investors are incredibly long-biased in portfolios, with equity allocations reaching some of the highest levels in history.” What Subramanian questioned is whether all the “good news” is already “priced in?” “Amid increasingly euphoric

Topics:

Lance Roberts considers the following as important: 9) Personal Investment, 9a.) Real Investment Advice, Featured, Investing, newsletter, Technically Speaking

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

After discussing BofA’s view of why the market could drop to 3800, I thought it fair to discuss a more optimistic view. BofA’s view of a market correction was a function of the more exuberant “optimism” in the market. To wit:

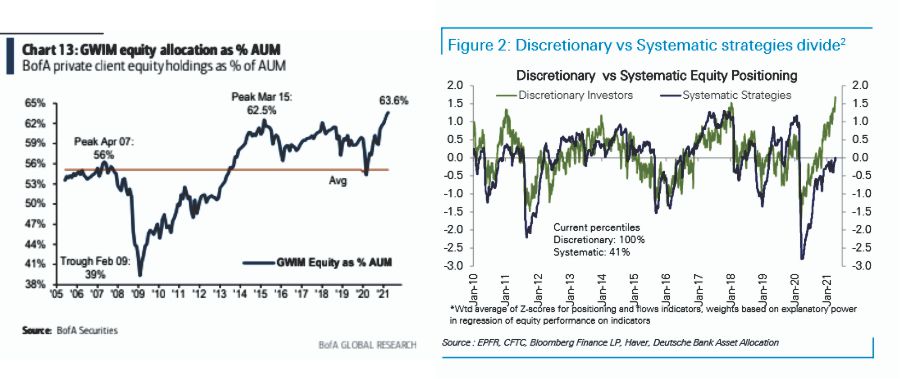

“More importantly, investors are incredibly long-biased in portfolios, with equity allocations reaching some of the highest levels in history.” What Subramanian questioned is whether all the “good news” is already “priced in?”

So, with BofA’s context in place, what is Yardeni seeing so differently? |

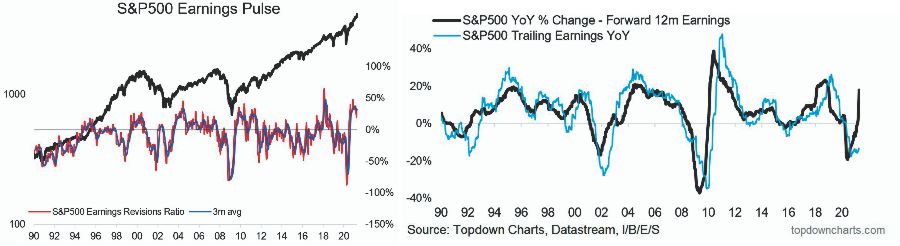

S&P 500 Earnings Revisions, 1990 - 2020 - Click to enlarge |

Yardeni’s Outlook

The basis of Yardeni’s forecast is that of a robust economic recovery that, in his words, was “much better than expected.” The other reasons supporting his optimistic view are:

|

Equity Allocations - Click to enlarge |

| Psychology Of QE

A recent commentary from Mish Shedlock on QE is key to understanding the current speculative psychology. I pulled two specific quotes from his article:

And

In other words, “Quantitative Easing” is a mental formation. The only thing that alters its effectiveness of the Fed’s monetary policy is investor psychology itself. Such was a point we made in the “Stability/Instability Paradox.”

|

|

Moral HazardThe ‘stability/instability paradox’ assumes that all players are rational, and such rationality implies avoidance of destruction. In other words, all players will act rationally, and no one will push “’the big red button.’” Importantly, what Hussman addresses when he says investors psychologically rule out the possibility of price declines is “moral hazard.” What exactly is the definition of “moral hazard.”

|

Fed Balance Sheet vs. S&P 500, 2018 - 2020 - Click to enlarge |

| The increase in the Fed’s balance sheet remains in near lockstep with the stock market’s climb.

While Fed officials tacitly deny any correlation between their monetary interventions and the stock market, the evidence is quite clear. However, as stated, the consequences of monetary policy longer-term gets set aside for the short-term benefits of inflated “psychology.” |

|

The Flies In The OintmentI would be remiss in not briefly addressing some of the concerns in Yardeni’s views. Productivity is deflationary. As I discussed in “The Roaring ’20s Aren’t Coming:”

Furthermore, a sustained spike in inflation, which drives rates higher, will negatively impact both the markets and the economy. As Michael Lebowitz noted in “What Interest Rate Will Matter,” rate increases have a history of financial events. |

Stock Bond Ratio vs. S&P Index, 1997 - 2021 - Click to enlarge |

To wit:

|

Productivity & Wages in The "New-New Normal", 2000 - 2021 - Click to enlarge |

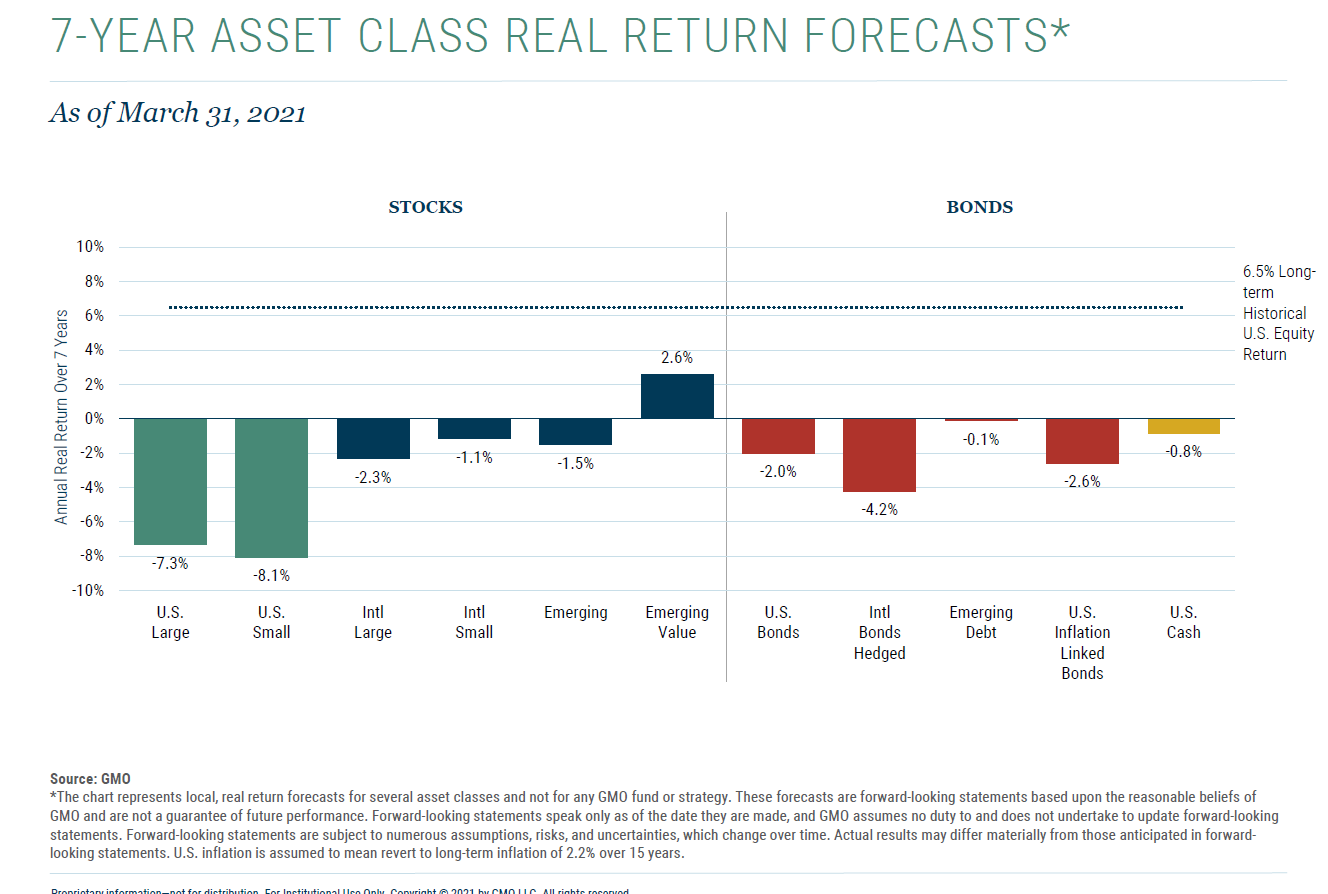

Yes. Valuations Are Expensive.While Yardeni suggests valuations are cheap, there is little evidence that such is the case. Most of the assumption is that earnings and the economy will “catch up” with prices. Such would suggest that prices remain stagnant during that process, yet Yardeni assumes prices will surge to 4500 in 2021, eclipsing the benefit of assumed growth. Therefore, valuations are not only high by historical standards but will remain high as prices rise along with economic and earnings growth. The consequence of over-paying for valuations today is substantially lower long-term returns from asset classes in the future. The eponymous GMO noted such in their most recent 7-year forecasts. Furthermore, given the extremely high correlation between stocks and bonds, a level of extreme not seen since the “Dot.com” peak, future outcomes seem poor. |

10 Year Yields and Secular GDP Growth, 1977 - 2021 - Click to enlarge |

| nue to supply liquidity, which will help the market ignore the reality of the majority of return barometers. However, as we saw in March of 2020, that does not preclude hair-raising volatility and significant declines. But, to Yardeni’s point, in the short-term Fed liquidity does support prices on the margin regardless of the environment. |

7-Year Asset Class Real Return Forecasts - Click to enlarge |

| Does that mean the market will crash tomorrow? No. However, it does strongly suggest that at some point, a mean-reverting event will occur. Such a decline will wipe out a large chunk of recent gains as markets reprice for slower future economic growth.

If you agree with Dr. Yardeni, the prescription is |

|

| ng>Does that mean the market will crash tomorrow? No. However, it does strongly suggest that at some point, a mean-reverting event will occur. Such a decline will wipe out a large chunk of recent gains as markets reprice for slower future economic growth.

If you agree with Dr. Yardeni, the prescription is simple. Buy stocks. However, as Mark Hulbert recently noted:

So, what should you do if you are close to retirement?

You have a choice. But, for now, Yardeni is correct. Just remember:

The post Technically Speaking: Yardeni – The Market Will Soon Reach 4500 appeared first on RIA. |

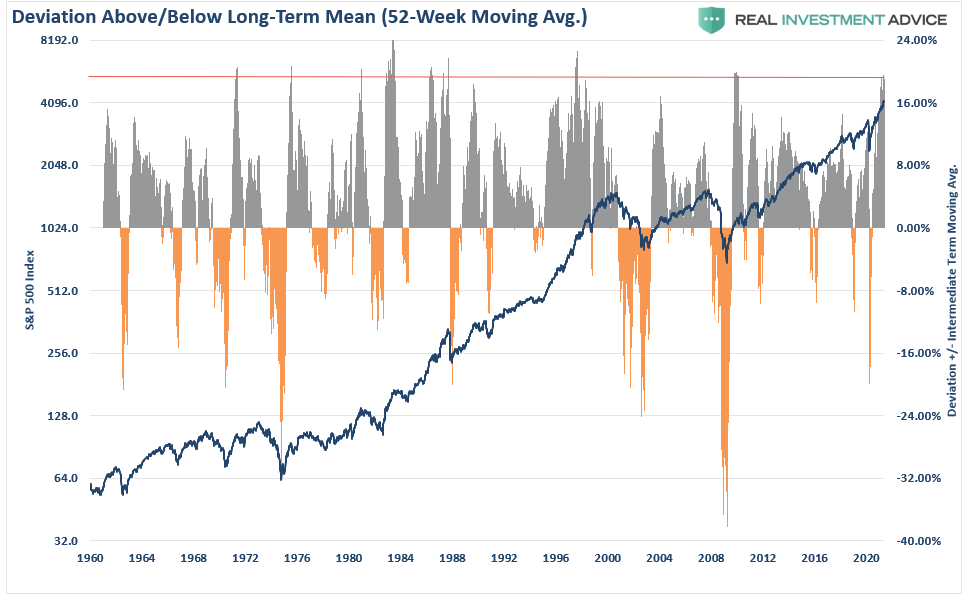

S&P500 Deviation 52 WMA, 1960 - 2020 - Click to enlarge |

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-05-17

Update May 17 2021: SNB intervening. Sight Deposits have risen by +2.7 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +2.7 bn. compared to last week.

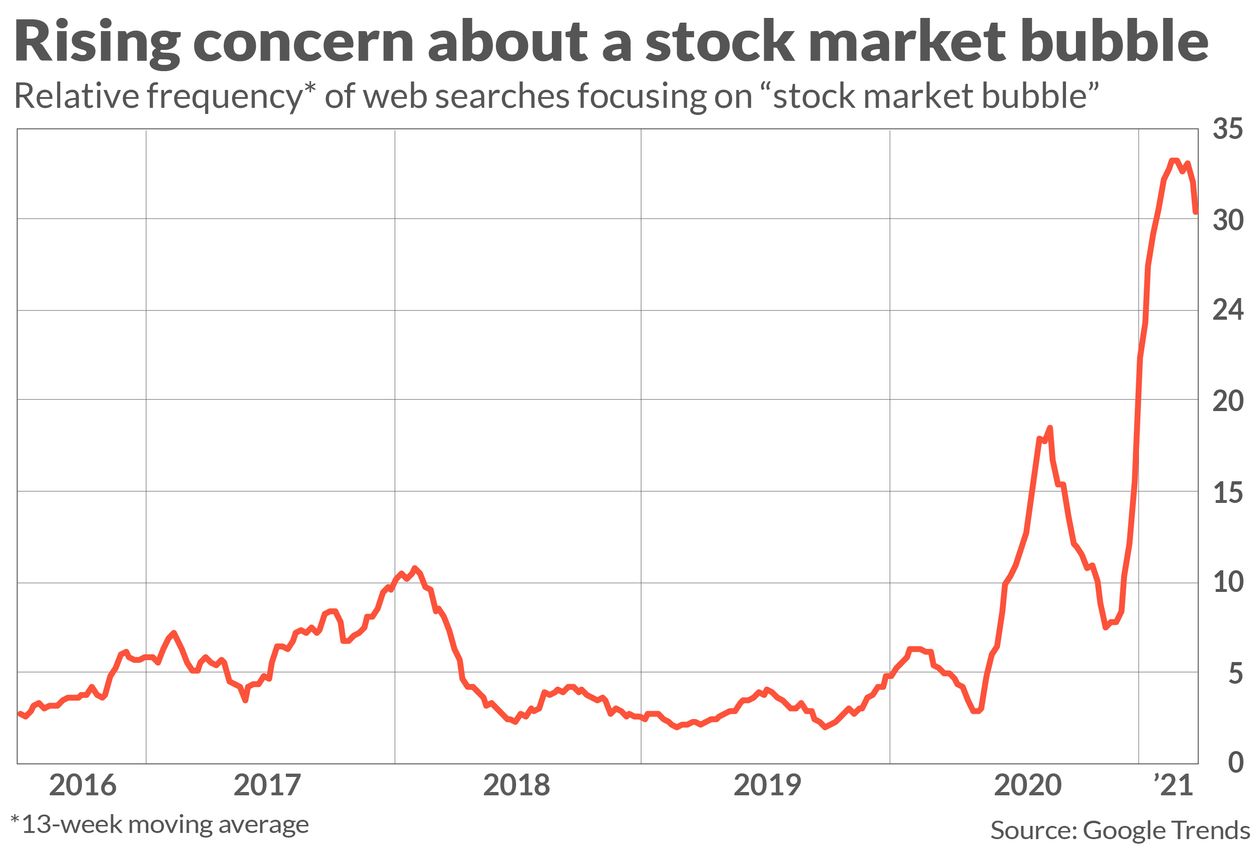

Technically Speaking: If Everyone Sees It, Is It Still A Bubble?

Technically Speaking: If Everyone Sees It, Is It Still A Bubble?

2021-05-11

“If everyone sees it, is it still a bubble?” That was a great question I got over the weekend. As a “contrarian” investor, it is usually when “everyone” is talking about an event; it doesn’t happen.

As Mark Hulbert noted recently, “everyone” is worrying about a “bubble” in the stock market.

#MacroView: Are Stocks Cheap, Or Just Another Rationalization?

#MacroView: Are Stocks Cheap, Or Just Another Rationalization?

2021-05-07

Are stocks “cheap,” or is this just another bullish “rationalization.” Such was the suggestion by the consistently bullish Brian Wesbury of First Trust in a research note entitled “Yes, Stocks Are Cheap.” To wit:

“The Fed remains highly accommodative, there are trillions of dollars of cash on the sidelines, vaccines have reached over 50% of Americans, and the economy is expanding rapidly. Some valuations have been stretched, but the market as a whole remains undervalued. As a result, we remain bullish and are lifting our targets.”

Yes, it is true the Fed remains highly accommodative, which has undoubtedly pushed asset prices higher. In fact, financial conditions recently reached a historic low, which suggests elevated asset valuations ironically.

We have busted the “myth of cash on the

All Inflation Is Transitory. The Fed Will Be Late Again.

All Inflation Is Transitory. The Fed Will Be Late Again.

2021-05-02

In this issue of “All Inflation Is Transitory, The Fed WIll Be Late Again.“

Market Review And Update

All Inflation Is Temporary

The Fed Should Be Hiking Now

Portfolio Positioning

#MacroView: No. Bonds Aren’t Overvalued.

Sector & Market Analysis

401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Catch Up On What You Missed Last Week

Market Review & Update

Last week, we said:

“The market is trading well into 3-standard deviations above the 50-dma, and is overbought by just about every measure. Such suggests a short-term ‘cooling-off’ period is likely. With the weekly ‘buy signals’ intact, the markets should hold above key support levels during the next consolidation phase.”

“As shown above, that is what is currently occurring. While

Seth Levine: Bitcoin Doesn’t Fix Defi, Defi Fixes Bitcoin

Seth Levine: Bitcoin Doesn’t Fix Defi, Defi Fixes Bitcoin

2021-05-02

Does Bitcoin Fix Defi (Definancialization)? “Bitcoin fixes this.” I cringe every time I see this popular meme. I find it worse than nails on a chalkboard. Bitcoin and other cryptocurrencies (crypto) supporters seem to wheel this tired trope out for every problem they see, particularly at economic ones. To their credit, they genuinely want to fix the financial system’s problems.

The Battle Royale: Stocks vs. Bonds (Which Is Right?)

The Battle Royale: Stocks vs. Bonds (Which Is Right?)

2021-04-28

The Battle Royale: Stocks vs. Bonds. The S&P 500 is at valuations higher than those in 1929 and rival those of 1999. Despite a recession, the index is 25% above where it was trading before the pandemic. The equity stampede is undoubtedly bullish about corporate earnings prospects and, by default, economic growth.

How to file your taxes with Swiss and foreign securities

How to file your taxes with Swiss and foreign securities

2021-03-04

One question I get often is how to file taxes with stocks and dividends. And this especially gets popular when we add foreign stocks and foreign dividends into the mix. Many people are afraid of investing because they think it will make it complicated to file your taxes. But in practice, it is not complicated to file your taxes even with a large ETF portfolio.

A Major Support For Asset Prices Has Reversed

A Major Support For Asset Prices Has Reversed

2020-12-24

In 2019, we wrote about how corporate share repurchases, or “stock buybacks,” had accounted for nearly all buying in the market. A year later, that significant support for asset prices has reversed.

Tags: Featured,Investing,newsletter,Technically Speaking