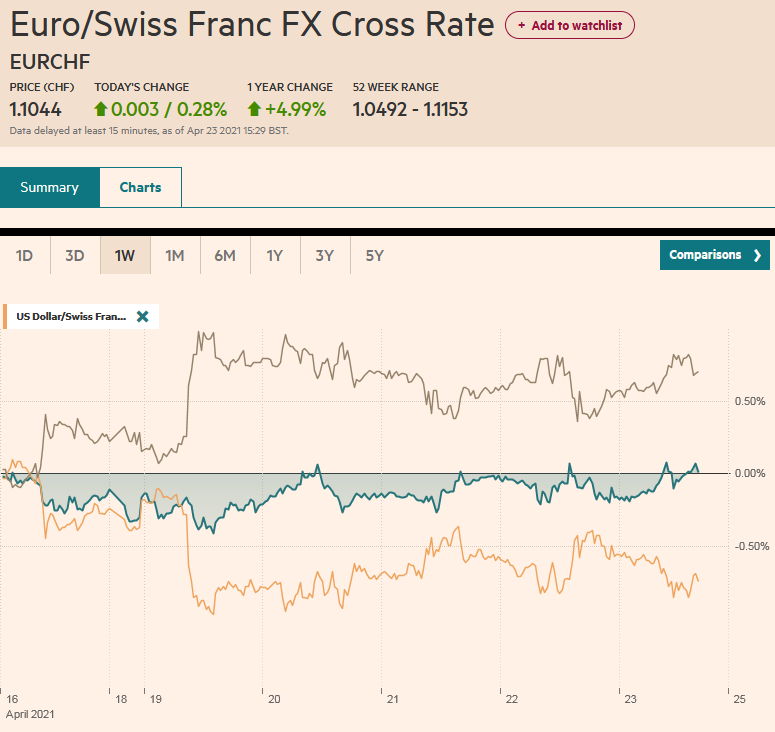

Swiss Franc The Euro has risen by 0.28% to 1.1044 EUR/CHF and USD/CHF, April 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Many narratives link the prospect of higher capital gains tax on about a third of 1% of Americans as the catalyst for losses in US equities yesterday (and Bitcoin) and weakness in some global shares today. Of the large markets in the Asia Pacific region, only Japan, which is reimposing a formal emergency in Tokyo, Osaka, and two other prefectures, fell. India, which is experiencing a dramatic surge in the contagion, fell. European shares are trading lower, and the Dow Jones Stoxx 600 is set to snap a seven-week advance. US shares are trading with a slightly firmer bias. The US

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Currency Movemeent, ECB, Featured, newsletter, PMI, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.28% to 1.1044 |

EUR/CHF and USD/CHF, April 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

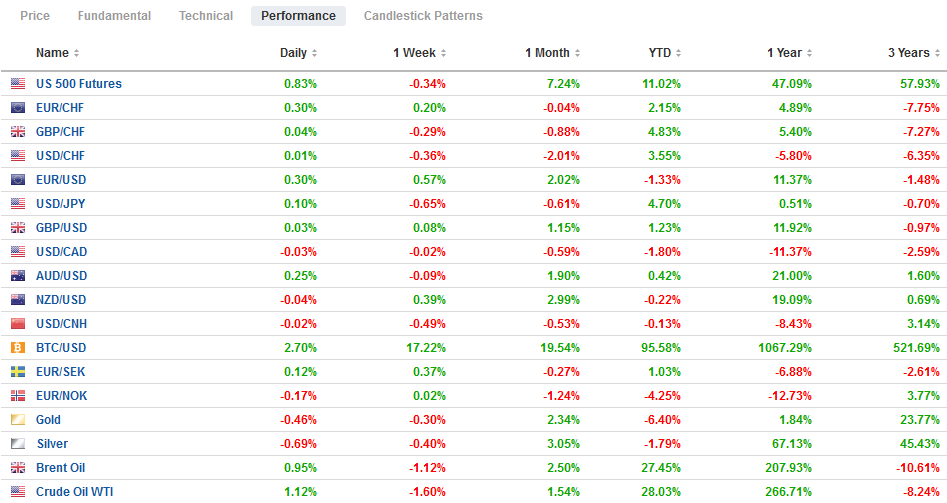

FX RatesOverview: Many narratives link the prospect of higher capital gains tax on about a third of 1% of Americans as the catalyst for losses in US equities yesterday (and Bitcoin) and weakness in some global shares today. Of the large markets in the Asia Pacific region, only Japan, which is reimposing a formal emergency in Tokyo, Osaka, and two other prefectures, fell. India, which is experiencing a dramatic surge in the contagion, fell. European shares are trading lower, and the Dow Jones Stoxx 600 is set to snap a seven-week advance. US shares are trading with a slightly firmer bias. The US 10-year yield is little changed at 1.55%, while European benchmark yields are softer. The dollar is under broad pressure to put the finishing touches on a poor week. The Australian dollar, sterling, and the euro lead today’s move. On the week, the Japanese yen and euro are the strongest (~0.8% and ~0.6%, respectively). The Aussie, in contrast, virtually flat. Among emerging market currencies, eastern and central Europe are the best today, while the Chinese yuan ends a nine-day advance. The Russian ruble was bid ahead of the central bank meeting, and a 50 bp rather than 25 bp hike was delivered. The JP Morgan Emerging Market Currency Index is edging higher for the third consecutive session and eight of the past ten. Gold is nearly flat as it tries to secure its third weekly advance. Oil is trading with a firmer bias but is still off a little more than 2% this week, paring last week’s 6.5% gain. |

FX Performance, April 23 - Click to enlarge |

Asia Pacific

Japan reported March CPI figures and the preliminary estimate to the April PMI. The inflation was in line with expectations, with the headline rising from -0.4% to -0.2%. The core rate, which excludes fresh food, stands at -0.1%, up from -0.4%, and the measure excluding fresh food and energy was 0.3% higher than a year ago. The PMI showed improved manufacturing (53.3 vs. 52.7), but the service component was flat (48.3). Nevertheless, the composite poked above the 50 boom/bust level (50.2) for the first time since January 2020. Nevertheless, with formal states of emergency starting Sunday and running through May 11 for Tokyo, Osaka, Kyoto, and Hyogo, whatever momentum the economy enjoys is at risk. Still, Prime Minister Suga reaffirmed the Olympics would proceed as scheduled, with opening ceremonies scheduled for three months from today.

Australia’s preliminary PMI shows its recovery is extending. The manufacturing component rose to 59.6 from 56.8, and the service component rose to 58.6 from 55.5. These combined to lift the composite to 58.8 from 55.5. Australia’s stronger growth will likely translate into a smaller budget deficit, and this will be evident when the FY21-22 budget is presented on May 11.

The UK parliament joined Canada and the Netherlands to declare China’s treatment of Uyghurs as genocide. It is a non-binding resolution. The motion was led by one of the five MPs that Beijing barred from entering China in retaliation for sanctions imposed by the UK (in coordination with the US, EU, and Canada). Still, it will likely force the government in a direction that it already appeared to be moving, and that is a more confrontational stance. With some conservative assumptions, China’s economy may surpass the size of the American economy within the next decade, and it is the biggest trading partner of many, including the EU, Japan, Australia, Germany, and India. Yet, it is terribly isolated on the world stage. The genocide accusation will likely fuel a movement to boycott the next winter Olympics in Beijing. A US official had suggested that the Biden administration was sympathetic, but it was later denied by the Secretary of State Blinken. Still…

The dollar has been confined to a 20-tick range below JPY108.00 so far today. The inability of the greenback to sustain modest upticks against the yen stretches into the fifth consecutive session. It has only risen in one session over the past two weeks and is the third consecutive week it has fallen. Yet, it has barely retraced (38.2%) of the year’s gain. The next retracement objective (50%) is near JPY106.80. The Australian dollar is recovering from the six-day low seen yesterday, near $0.7690, and is hovering around $0.7735 in the European morning, which is around the middle of this week’s range. It has gained more than 1.5% in the past two weeks and stalled near $0.7800 this week. The Chinese yuan is edging lower today for the first time in two weeks. The PBOC set the dollar’s reference rate in line with expectations at CNY6.4934. The dollar is off about 0.4% this week after falling about 0.5% last week and 0.2% the previous week.

Europe

The preliminary PMI shows the euro area recovery is gaining momentum. The German and French manufacturing PMIs slipped slightly (and less than expected) from March’s readings, but the aggregate estimate for the region rose to 63.3 from 62.5. Germany’s service PMI slipped (to 50.1 from 51.5) while France’s estimate rose back above 50 (to 50.4 from 48.2). The aggregate figure rose to 503 from 49.6. The EMU composite rose to 53.7 from 53.2 and is the highest since last year’s peak set in July at 54.7.

The UK’s data was most impressive. As non-essential stores re-opened, retail sales exploded. The 5.4% rise was around four times greater than the median forecast in the Bloomberg survey, and the year-over-year pace was more than double the 3.5% expected. The flash PMI for April also handily beat expectations. The manufacturing PMI rose to 60.7 from 58.9. The service PMI rose to 60.1 from 56.3, and the composite jumped to 60 from 56.4. Last year, the composite peaked in August at 59.1.

As generally anticipated, the ECB meeting was unremarkable. The status quo was maintained as the risk assessment (downside near-term, balanced medium-term) was unchanged. ECB President Lagarde cautioned against reading much into the week-to-week asset purchases but that the monthly data will reflect the increased bond purchases. She would not allow herself to be pinned down about a review of the pace of the purchases at the June meeting, which depends also on the new staff forecasts and the evolution of prices. However, we know that the ECB will look through near-term price pressures that are understood to be technical in nature and temporary. The implication is that if the forecasts for growth are revised higher (and they will almost certainly be increased as the March forecasts did not include the knock-on effect from the US stimulus and the greater resilience of several of the large members). The preliminary estimate of April CPI will be reported on April 30 at the same time as the first estimate of Q1 GDP.

Geopolitical tensions in Europe are set to deescalate following Russia’s Defense Minister Shoigu’s announcement that military forces massed in recent weeks on the Ukraine border will return to their bases by May 1. To help de-escalate the situation, US President Biden offered a summit with Russia’s Putin later this year. Shoigu’s comments are not completely new. Ten days ago, he indicated that “exercises” would be over by the end of the month. It appears Putin got three things. First, the separatist region in the east backed by Moscow is somewhat safer. Russia signaled its intention of defending Donbas. Second, Putin succeeded in sending a clear signal that he would not accept Ukraine as a NATO member. Third, despite the thuggery, interference with the US election, and offering bounties to kill Americas in Afghanistan, Putin secured a summit with Biden, even if the details have to be worked out.

The euro is trading firmly but inside yesterday’s range, where the approach to the week’s high (~$1.2080) was sold, but the dip below $1.20 was bought. The $1.2070-$1.2080 still blocks the upside. Above there, the next target is a little above $1.21, which is the (61.8%) retracement target of the decline since the early January high near $1.2350. A risk late today comes from the S&P review of Italy’s BBB credit rating. As one would expect, the fiscal situation has deteriorated its October review that removed the negative outlook. By comparison, Fitch and Moody’s rating is one notch lower. Sterling posted an outside down day yesterday, but there has been no follow-through selling today. It is consolidating in about a half-a-cent range below $1.39, where a GBP650 mln option is set to expire today. Sterling settled last week near $1.3830. This would be the second consecutive weekly gain and the third in the past four weeks.

America

The US sees the preliminary PMI today and new home sales. One way in which the US PMI stands out is that the service PMI is likely to remain above the manufacturing reading as the recovery gains momentum, and now more than half of the adults have had at least one vaccine shot. The FOMC meets next week, and the economic acceleration is consistent with the Fed’s outlook. We note that yesterday’s weekly initial jobless claims fell more than expected, and there continues to be talk that around a million workers returned to their jobs this month. Some, like ourselves, wonder this does not make tapering more likely before the end of the year. Meanwhile, new home sales are expected to bounce back from the weather-induced weakness in February. The median forecast is for an 885k seasonally adjusted annual pace. Last year’s average was 822k, and in 2019, it was 685k.

Canada’s economic diary is light today and features February retail sales and GDP next week. This week will be remembered for the Bank of Canada’s decision to reduce its bond-buying (to C$3 bln a week) and bringing forward to H2 22 when it now projects the economic slack will be absorbed, which says something about the timing of a rate hike. Mexico’s bi-weekly CPI rose above 6% through April 15, the highest in nearly three years. It prevents the central bank from resuming its easing cycle when it meets again on May 13. Today, Mexico reports February retail sales. The median forecast in Bloomberg’s survey is for a 0.8% increase after January’s 0.1%. In terms of capital inflows into Mexico, note that worker remittances are more significant than the trade surplus.

The US dollar continues to consolidate the losses suffered in response to the hawkish Bank of Canada in the middle of the week when it reached CAD1.2460. There is a large $1.2 bln option struck at CAD1.2450 that expires today. There is also an option for $1 bln to CAD1.2500 that expires today. The greenback settled near CAD1.2510 last week. Despite the Bank of Canada, the Canadian dollar is among the worst-performing major currencies this week, rising less than 0.2% against the US dollar. The greenback fell against the Mexican peso every session last week and is down for the third day this week. It settled near MXN19.93 last week, and barring a recovery today, it will be the fourth consecutive weekly decline, matching the longest drop since last August-September. Mexico offers 4%+ on its T-bills, and the carry seems to be a key attraction. Also, the peso serves as a proxy for some investors, for emerging markets as a whole. We note that the JP Morgan Emerging Market Currency Index has also risen for the four consecutive weeks.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

2021-04-19

Update April 19 2021: SNB intervening. Sight Deposits have risen by +0.2 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +0.2 bn. compared to last week.

FX Daily, January 29: Please Stay Seated, the Ride is not Over

FX Daily, January 29: Please Stay Seated, the Ride is not Over

2021-01-29

Powerful corrective forces continue to grip the market. After a large rally to start the New Year, the correction is punishing. Most Asia Pacific equities markets were off again today to bring the week’s loss to 2.5% to 5.5% throughout the region. Europe’s Dow Jones Stoxx 600 is a little more than 1% lower on the day.

FX Daily, January 22: Faltering Friday

FX Daily, January 22: Faltering Friday

2021-01-22

Fear that social restrictions may have to be broadened and extended is helping spur a wave of profit-taking and de-risking, which has also been encouraged by disappointingly high-frequency data. The equity rally seemed to falter a bit in the US, as the S&P 500 eked out a minor 0.03% gain yesterday.

FX Daily, January 21: It is the ECB’s Turn but Little New to be Said or Done

FX Daily, January 21: It is the ECB’s Turn but Little New to be Said or Done

2021-01-21

Overview: The S&P 500 and NASDAQ gapped higher yesterday to record-levels, and the reflation theme lifted Asia Pacific shares for the third session today. South Korea, Taiwan, and China led the advance.

FX Daily, January 11: Greenback Extends Recovery

FX Daily, January 11: Greenback Extends Recovery

2021-01-11

Julius Ceasar is said to have "crossed the Rubicon" on January 10, 49 BCE, taking the 13th Legion into Rome, defying orders from the Senate, and precipitating the Roman Civil Wat that marked the end of the republic and the birth of the empire.

FX Daily, December 10: Brexit and US Stimulus are Unresolved as Attention Turns to the ECB

FX Daily, December 10: Brexit and US Stimulus are Unresolved as Attention Turns to the ECB

2020-12-10

Overview: US threats to break-up Facebook and the stalled stimulus talks spurred profit-taking in US shares yesterday and is dampening enthusiasm today. The MSCI Asia Pacific Index fell for the third time this week, and Europe’s Dow Jones Stoxx 600 is little changed.

FX Daily, November 30: Equities are Heavy and the Dollar Softer to Start New Week

FX Daily, November 30: Equities are Heavy and the Dollar Softer to Start New Week

2020-11-30

Overview: Month-end profit-taking saw Asia Pacific shares tumble earlier today. Most markets are off 1-2.5% today after the MSCI Asia Pacific Index rose 2.25% last week. European shares are mixed, but little changed. US shares are also trading lower.

FX Daily, November 4: Indecision Keeps Investors on Edge, but the Dollar Rides High

FX Daily, November 4: Indecision Keeps Investors on Edge, but the Dollar Rides High

2020-11-04

Initially, the markets built on Tuesday’s price action, but as soon as a few counties in Florida indicated that it was not going to be the "blue wave," risk came off, and it was most evident in the bond and currency markets. Equities rallied in the Asia Pacific area, and all but Hong Kong, Australia, and Indonesia advanced.

Tags: #USD,Currency Movemeent,ECB,Featured,newsletter,PMI